Global| Apr 03 2019

Global| Apr 03 2019U.S. ADP Private-Sector Payroll Increase Weakens

by:Tom Moeller

|in:Economy in Brief

Summary

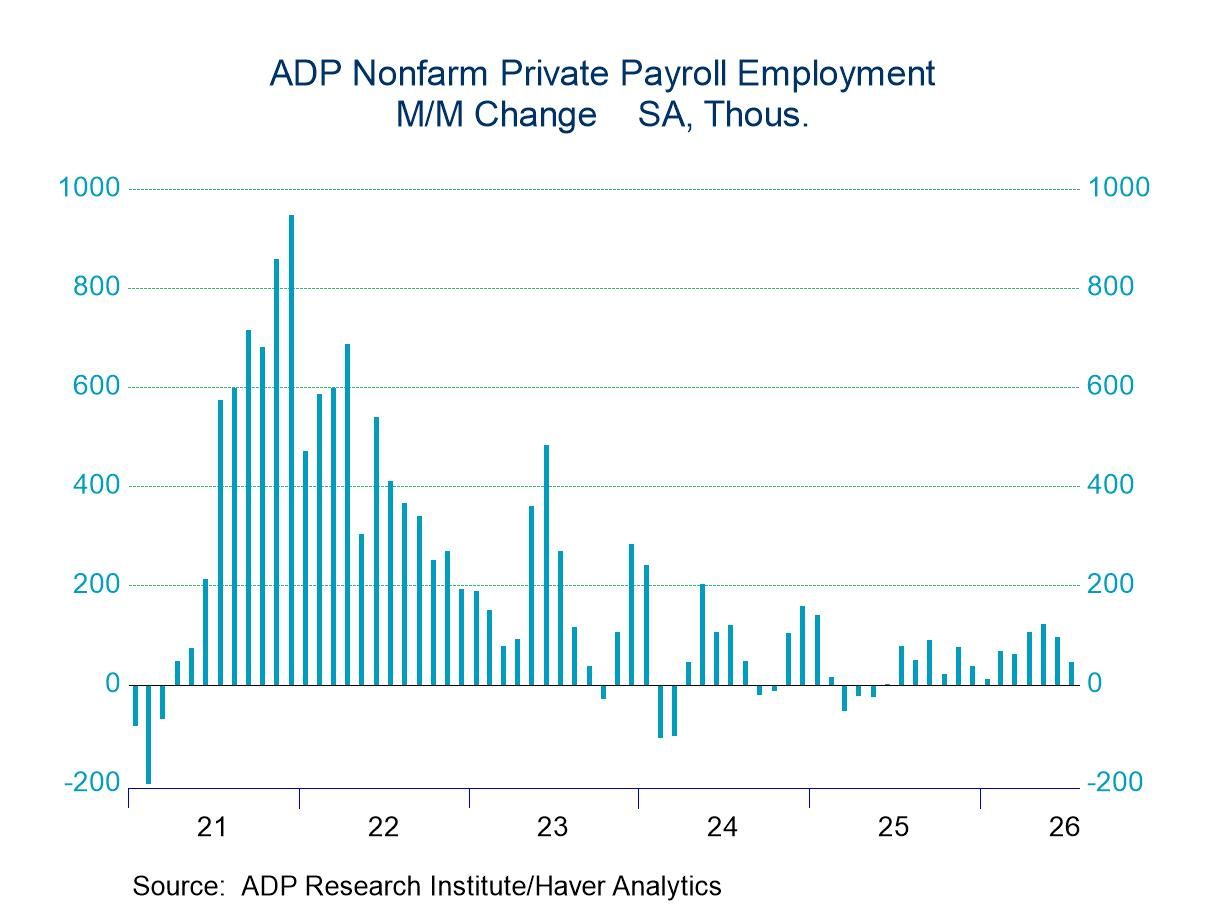

ADP indicated in its National Employment Report that private nonfarm payrolls increased 129,000 (2.0% y/y) during March after a 197,000 February gain, revised from 183,000. It was the weakest increase since September 2017. A 180,000 [...]

ADP indicated in its National Employment Report that private nonfarm payrolls increased 129,000 (2.0% y/y) during March after a 197,000 February gain, revised from 183,000. It was the weakest increase since September 2017. A 180,000 gain had been expected in the Action Economics Forecast Survey. The three-month average rise in private sector payrolls eased to 196,000, down from 236,000 as of February. During the last ten years, there has been an 84% correlation between the change in the ADP figure and the change in nonfarm private-sector payrolls as measured by the Bureau of Labor Statistics.

The ADP National Employment Report is calculated from ADP's business payroll transaction system covering 411,000 companies and nearly 24 million employees. The data is calibrated and aligned with the Bureau of Labor Statistics establishment survey data and is produced by the Automatic Data Processing Research Institute in collaboration Moody's Analytics Inc. The ADP data only cover private sector employment.

Small business hiring weakened to 6,000 (1.3% y/y) following a 19,000 rise. The latest was the weakest since a decline in September 2017. The three-month average gain of 39,000 was down from 70,000 as of January. Medium-sized payrolls rose a weaker 63,000 (2.7% y/y) and by a slightly weakened 93,000 on a three-month basis. Large payrolls rose 60,000 m/m (2.3% y/y) and by 64,000, on average, during the last three months, up from 37,000 as of January.

Goods-producing payrolls declined 6,000 (+2.5% y/y) in March after a 35,000 rise. The three-month average gain eased to 39,000, down from 73,000 as of March 2018. Construction sector payrolls also declined 6,000 m/m but remained strong at 4.1% y/y. The three-month average change eased to 24,000 from its 43,000 high roughly one year earlier. Manufacturing sector employment eased 2,000 (+1.4% y/y), the first decline since December 2016. The three-month average rise was stable at 13,000 due to strong gains during the prior two months. Natural resource and mining sector payrolls rose 2,000 following declines in three of the prior four months. Twelve-month growth fell to 5.0% from its high of 9.2% last June.

Private-service sector payrolls rose 135,000 (1.9% y/y), the weakest rise since November. Three-month average growth of 158,000 has been fairly steady since early last year. Jobs in education & health services increased an improved 56,000 (2.2% y/y). Professional and business services payrolls gained an easier 41,000 (2.7% y/y). Trade transportation & utilities employment rose a greatly lessened 9,000 (1.2% y/y), the weakest since declines early in 2017. Employment in the financial services sector slipped 1,000 (1.2% y/y) compared to an 18,000 peak rise last September. Information sector employment grew an improved 11,000 (0.5% y/y), up from stability during the prior four months. Leisure & hospitality employment rose a weakened 13,000 (2.4% y/y).

The ADP National Employment Report data can be found in Haver's USECON database; historical figures date back to April 2001 for the total and industry breakdown, and back to January 2005 for the business size breakout. The expectation figure is available in Haver's AS1REPNA database.

Why Are Recessions So Hard to Predict? Random Shocks and Business Cycles from the Federal Reserve Bank of Philadelphia is available here.

| ADP/Moody's National Employment Report | Mar | Feb | Jan | Mar Y/Y | 2018 | 2017 | 2016 |

|---|---|---|---|---|---|---|---|

| Nonfarm Private Payroll Employment (m/m chg, 000s) | 129 | 197 | 264 | 2.0% | 2.0% | 1.7% | 2.0% |

| Small Payroll (1-49) | 6 | 19 | 93 | 1.3 | 1.5 | 1.5 | 1.9 |

| Medium Payroll (50-499) | 63 | 98 | 119 | 2.7 | 2.3 | 1.8 | 1.5 |

| Large Payroll (>500) | 60 | 80 | 52 | 2.3 | 2.3 | 2.1 | 2.7 |

| Goods-Producing | -6 | 35 | 87 | 2.5 | 3.1 | 1.7 | 0.8 |

| Construction | -6 | 17 | 62 | 4.1 | 5.0 | 3.3 | 4.3 |

| Manufacturing | -2 | 19 | 22 | 1.4 | 1.8 | 0.8 | 0.1 |

| Service-Producing | 135 | 162 | 176 | 1.9 | 1.7 | 1.8 | 2.2 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief