Global| Jun 25 2020

Global| Jun 25 2020U.K. Retailing Continues to Reel Along with Global Prospects

Summary

In June, U.K. current sales metrics improved across the board. However, expectations for July largely worsened or held to extremely weak readings. These data on trend couple with new information on the virus accelerating its presence [...]

In June, U.K. current sales metrics improved across the board. However, expectations for July largely worsened or held to extremely weak readings. These data on trend couple with new information on the virus accelerating its presence in Europe and in parts of the U.S. and make the global picture a lot murkier than it had seemed to be just a few weeks ago. The U.K. has been struggling with the pandemic from the start and it appears to still be a huge factor either in fact or in fear.

In June, U.K. current sales metrics improved across the board. However, expectations for July largely worsened or held to extremely weak readings. These data on trend couple with new information on the virus accelerating its presence in Europe and in parts of the U.S. and make the global picture a lot murkier than it had seemed to be just a few weeks ago. The U.K. has been struggling with the pandemic from the start and it appears to still be a huge factor either in fact or in fear.

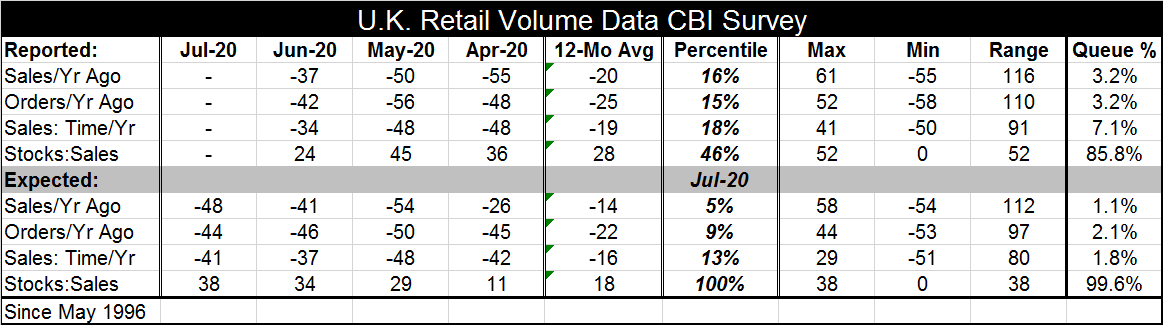

Current readings are weak

The current readings for June show improved results across the metrics. While the readings are a clear improvement from levels in the past two months, they are also still exceedingly weak.

Sales compared to one year ago are weak with a -37 net reading in June. That metric has a 3.2% queue standing; it is rarely weaker. This reading is not surprising because the previous two months were so weak. It will take several months of strength or more to offset that.

Similarly, orders compared to a year ago still have a very weak reading at -42 in June and another standing in its 3.2 percentile. Sales for the time of year log a -34 reading, significantly better than the reading of -48 in the last two months. Still, this reading has only a 7.1 percentile standing.

The stock-to-sales ratio is high at an 85.8 percentile standing, but it is also down from its May level and below its April level. High stock-to-sales ratios are not good for the outlook for production. But the movement of this ratio to a lower net standing is good news.

Outlook readings are weak…and worse

The outlook portion of the table with values for July is quite different although its percentile standings are equally poor and actually slightly weaker even than the very weak standings for the current metrics.

Expected sales compared to a year ago are weaker in July than they were in June. Sales for the time of year also are expected to be weaker. In both cases, this is a month-to-month weakening but the value rankings were even lower for May which was the nadir for most series. Sales compared to a year ago have a 1.1 percentile standing Sales for the time of year have a 1.8 percentile standing. Orders compared to a year-ago improve slightly to a -44 reading in July from -46 in June, but that metric still has a 2.1 percentile standing.

And the stock to sales ratio that we discussed above is expected to be higher and has an even higher standing than in the current survey at its 99.6 percentile-- it is the higher stock to sales ratio on record. And that means inventories are expected to be bloated at a time that sales are waning and that combination is really a bad one for growth.

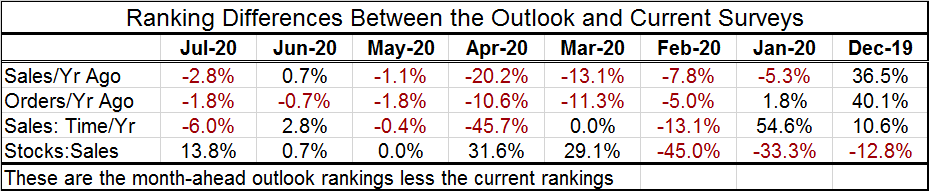

The table below looks at the gap between surveys taken at the same time. It looks at the differences in the RANK STANDINGS of the current and outlook variables. It subtracts the RANKING OF the current reading of June from the RANKING OF the outlook for July, and so on, for the last seven months. Since these series have different intrinsic net values, I have chosen to subtract their rankings rather than rely on their idiosyncratic raw values.

Since February there are eighteen values for sales vs. year-ago, orders vs. year-ago and sales: time of year. Of these 18 values, 15 (83%) show negative values indicating that the future was expected to be weaker than the current environment over the past six months. January and December readings were actually pointing more toward an expansionary outlook with relatively stronger look-ahead rankings even with the Brexit process in train. Since March the stock-to-sales ratio has been higher (or the same) indicting a tendency for inventories to begin to feel heavy to retailers. These metrics slightly preceded the recognition of the spread of the virus beyond China’s borders.

June marks the first month in this progression in which the future rankings started to exceed the current rankings, but that has reverted to weaker future rankings in July and to a move in the ‘wrong direction’ for the stock-to-sales ratio ranking as well.

The outlook has been in a deteriorating mode for some time

Real science

What the June survey (with June-July current/outlook readings) tells us about the future or at least what is expected of it is not good news. Beyond the borders of the U.K., there are other signs that are distressing as the IMF just yesterday announced a cut in its outlook and as virus infections begin to climb. However, one warning that is overdue is this: be careful what you fear. Noble Laurate Michael Levitt here argues for herd immunity and he is opposed to much of the analysis that has driven policy. His point is simply that herd immunity is the only science we have to control the spread of the disease. In other words, we need to spread the disease in a controlled way to stop it from spreading unchecked. This seemingly contradictory prescription simply draws on the fact that the way to stop/slow the spread of the disease is to build an immunity to it, a buffer within the general population. That is done by healthy people getting the disease and from that event acquiring resistance through antibodies. Then the next time the disease tries to strike them, that person will be immune and the disease will not spread through them. Put enough of these human buffers in the population and outbreaks will be naturally controlled. Instead of doing that, there is a fear of disease that is in some ways irrational. In the U.S., 40% of those who died were in nursing homes. In NYC, only 108 in a city of 8.8mln died who did not have any other preexisting illness. The large death toll in NYC of about 17,000 owes to nursing home deaths and the deaths of people who had preexisting healthcare issues and were not able to fight off the virus in their preexisting weakened state.

A second wave or a second way?

Clearly, while policymakers have made stopping the spread of the disease policy by tracking it publically and publishing these numbers, there is another way. That way would be to protect the people who are truly at risk and allow healthy people to develop immunity. Scientists- real scientists- know that waiting for a vaccine is more science fiction and hype than real science. And if a vaccine is developed in short order, it will not have been tested and could have side effects worse than the virus itself even for healthy people. The public has been kept in the dark about the real corona data and few people seem to know the real trends and trade-offs. Instead, the numbers that are bandied about by health officials ignore the fact that we have been operating with populations that are quite unhealthy and who have been kept alive by modern medicine and who remain vulnerable – to a lot of things. What is being exposed here is the unhealthiness of our populations much more than the virility of the virus. Japan has a very old population and yet even old Japanese people are healthy. It is why deaths in Japan have been so much lower.

The Las Vegas strategy

One thing to always bear in mind is that if we constantly stop our economies, lock them down, and prevent the spread of this disease we are preventing the acquisition of herd immunity and each time we unlock and open up we are at risk to a new wave of reinfection. To me this is like an old Keystone Cops silent move (see here on YouTube) or a Three Stooges comedy routine. We take a half measure and know it will not be enough, so we do it again and again. It has been said that doing the same thing over and over again and expecting a different result is a hallmark of insanity. Is our Covid-19 policy literally ‘insane?’ In fact, the current tactic to ‘control the virus’ actually prolongs it and may not in the end save any lives at all but may spread out the deaths over time. Unless we ‘draw to an inside straight’ and actually find an authentic usable and safe vaccine, having bought time actually only prolongs the period when we damage our economies and suffer the tragic feedback effects of having done that. And there is no guarantee of finding that vaccine and, no, the odds do not favor that scenario either. But that is policy. It is not science or based on science. It is the Las Vegas strategy or a policy I have also called ‘science fiction.’

The feast or famine of an arbitrary policy

IF we are willing to trash our economies and threaten the viability of our various economic systems and willing to ruin the lives and careers and businesses of many undeserving citizens to slow the spread of the virus… why are we not willing to shelter the vulnerable people, pay to protect them, and run our economies closer to full steam ahead and let healthy people acquire immunity? That is a question no one anywhere has answered in any satisfactory way. We are not even given any choice. We are told what to do. And what is worse, the real truth of the virus and who is at risk and how much they are at risk is being hidden. Instead, scare-mongering is being used to herd us all like sheep to compliance- a though those high death tolls apply to all of us. They don’t. Why don’t people know about the real facts and the real statistics of this disease? Why are only the worst of the anecdotes shown on TV? In the end, this approach to the disease is not only something that robs us of our freedom but it also something that imperils the vulnerable in our population who are not adequately warned or protected. In the meantime, many innocent hard-working people are made to suffer while others are allowed to feast on a windfall of government transfer payments.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief