Global| Dec 21 2020

Global| Dec 21 2020U.K. Retail Signals Are Mixed, Improved from November, and Still Sour

Summary

The CBI (Confederation of British Industry) survey of U.K. retailers shows clear December improvement compared to November. All current retail measures are better than in November and the inventory reading is leaner (in fact extremely [...]

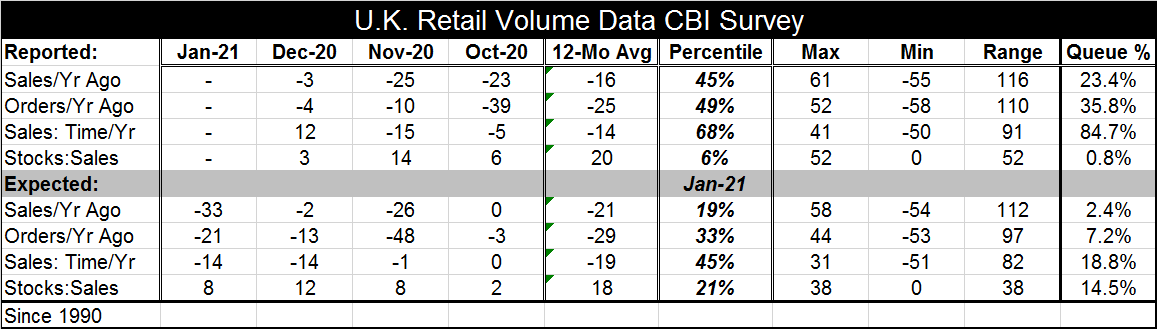

The CBI (Confederation of British Industry) survey of U.K. retailers shows clear December improvement compared to November. All current retail measures are better than in November and the inventory reading is leaner (in fact extremely lean- and that may not be a good thing in this environment). Sales for 'time of year' moved to a +12 net reading in December from -15 in November and log an 84.7 percentile standing. That standing is quite strong and is the out-of-place response in this survey. However, sales compared to a year ago have only a 23.4 percentile standing although the net metric improved month-to-month from -25 in November to -3 in December. Orders compared to one year ago also improved from -10 in November to -4 in December and they log a 35.8 percentile standing, well below their median (median for all rankings occurs at a 50% queue standing). To summarize December: it is a huge improvement from November but still largely a weak month except for one metric – that exception is the Santa Claus (sales adjusted for time of year).

The CBI (Confederation of British Industry) survey of U.K. retailers shows clear December improvement compared to November. All current retail measures are better than in November and the inventory reading is leaner (in fact extremely lean- and that may not be a good thing in this environment). Sales for 'time of year' moved to a +12 net reading in December from -15 in November and log an 84.7 percentile standing. That standing is quite strong and is the out-of-place response in this survey. However, sales compared to a year ago have only a 23.4 percentile standing although the net metric improved month-to-month from -25 in November to -3 in December. Orders compared to one year ago also improved from -10 in November to -4 in December and they log a 35.8 percentile standing, well below their median (median for all rankings occurs at a 50% queue standing). To summarize December: it is a huge improvement from November but still largely a weak month except for one metric – that exception is the Santa Claus (sales adjusted for time of year).

The outlook figures for January are different and for them there is no hint of a silver-lining or of a mixed signal. Come January what is expected is a move to worse outcomes. Only sales evaluated relative to the time of year are unchanged from their expectation reading in December. But the percentile standing of that reading is in its 18.8 percentile and that is quite weak even though it is unchanged month-to-month. Sales compared to a year ago plunge to -33 for January from -2 in December and log a 2.4 percentile standing. This is a net value so low it has been this weak or weaker only 2.4% of the time since 1990. And the Great Recession period is well enveloped by that timeline. Orders compared to a year ago get a -21 value for January, down from -13 in December and a standing in its 7.2 percentile, also extremely weak and not at all reassuring. Inventories are weaker from December to January and log a 14.5 percentile standing.

Bad news... but no real surprises

While none of this is good news none of it can be much of a surprise either. The UK-EU Brexit negotiations have not gone well, are in their 'final days' and once again appear to be on the rocks. That cannot be a good thing for any business in the United Kingdom. unless it is completely and totally cut off from any dependence on goods coming in from or going out to the EU. Even then any pure domestic service providing firm would continue to be at risk to being collateral damage from other sectors.

Setting aside Brexit issues (which are hard to set aside), there is a new wave of virus sweeping through the U.K. Some have called it so widespread that it will take the vaccine to stop it. Not that that isn't enough to worry about, but at the same time there is a mutation of the Covid-19 virus in the U.K. that may be more contagious than the main form of the virus everyone has been fighting up to this point. No one is quite sure what it is because the mutation has not been completely studied yet. Dr. Scott Gottlieb, on U.S. news show 'Face the Nation' over the weekend, said the mutation may be more contagious but that it did not appear to be more virulent. Still, there is enough concern about it that 40 countries have banned arrivals from the U.K.

It is truly surprising that the U.K. economy continues to do as well as it has been under the cloud of Brexit and after a change in government. A Brexit non-deal of some sort has been threatening for some time and the way out is still a tangled mess. Yet, growth continues and consumer spending holds up and the U.K. has - so far - about the same economic disruptions from the virus as the rest of the world.

But maybe that is all about to change.

The Brexit end game truly is at hand and Boris Johnson does not want to give the EU the fishing rights it wants. He complains that a country can't be given rights to its own fishing waters that are inferior to those of its trade partners. This does not seem to be an excessive observation on his part. It has always been clear that the negotiations would be difficult and they always have been difficult. In addition to the fishing rights demands, the other demands of the EU are still rather an intrusion on how business is conducted within the U.K. And escaping those restrictions is exactly the reason the U.K. sought to leave the EU. For its part, the EU wants to make sure that economic conditions inside the U.K. do not permit it to undercut competition in the EU. But few trade deals ever have asked for that sort of intrusion (although the U.K. does have some deals that do exactly that with other European countries with whom it trades that are not in the EU arrangement).

Summing up

The virus mutation is simply an unexpected mess hitting the fan. There is no way to handicap it since no one is quite sure of what it is. And after the way the Chinese covid-19 spread, everyone is on guard for something that might repeat or (God forbid!) be worse. But as yet, no one really knows how bad this is. But the cutting off of U.K. arrivals by 40 countries is probably just a precursor to other commerce being put in a standstill and that could be very damaging to the U.K. and to its trade partners. Markets can anticipate that. They are not reacting well to this news. The stock market sell-off is not substantial at this point, but it reflects what fears are at the moment and they can always get worse. Clearly this is an event markets are not sluffing off. Some liquids do not roll off a duck's back. This is one of them.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief