Global| Jan 18 2019

Global| Jan 18 2019U.K. Retail Sales Begin to Lose Momentum

Summary

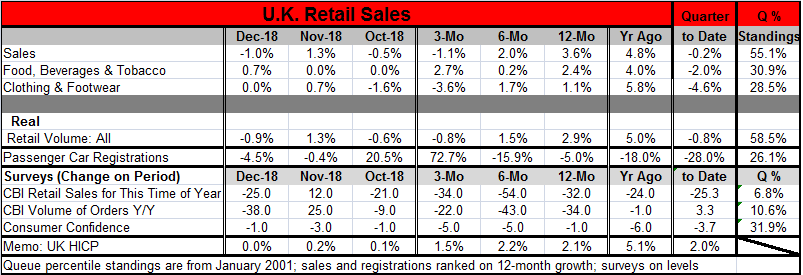

U.K. retail sales fell by a sharp 1% in December. Monthly sales last fell by 1% nine months ago and last fell by more than 1% 19 months ago. The drop in sales is truly sharp. Purchases in the month of food, beverages and tobacco rose [...]

U.K. retail sales fell by a sharp 1% in December. Monthly sales last fell by 1% nine months ago and last fell by more than 1% 19 months ago. The drop in sales is truly sharp.

U.K. retail sales fell by a sharp 1% in December. Monthly sales last fell by 1% nine months ago and last fell by more than 1% 19 months ago. The drop in sales is truly sharp.

Purchases in the month of food, beverages and tobacco rose by a solid 0.7%, but clothing and footwear purchases were flat and have declined on balance over the last three months.

Retail sales volumes in the U.K. fell by 0.9% in December. Real sales fell by more than this month-to-month 19 months ago.

Real sales volumes also are lower over three months, falling at a 0.8% annual rate. And sales volumes are steadily weakening from a solid and respectable 2.9% gain over 12 months to a 1.5% pace over six months to the 0.8% pace of decline over three months. The progression is disturbing.

Interestingly, the pattern for car registrations is the opposite, with passenger car registrations falling at a 5% pace over 12 months, contracting at a 15.9% pace over six months and exploding to the upside with a 72.7% annual rate increase over three months.

However, car sales seem to have a life and a pattern all their own. And in this case, car registrations are lower over 12 months and 12-months ago they were lower as well. So what we are seeing here with car registrations is a rebound after a prolonged period or slumping auto registrations.

The CBI survey offers some additional metrics on retailing. In December, the CBI survey found sales for the ‘time of year’ logged a -25 survey value which produces a 6.8% queue percentile ranking marking seasonal sales as being worse historically less than 7% of the time. Retail orders year-on-year logged a -38 survey reading that corresponds to a 10.6 percentile queue standing – a reading that has been weaker historically only about 10% of the time. Rounding out other metrics on retailing is a look at consumer confidence that posted a -1 reading, a level that has been worse about 32% of the time historically.

On balance, the various measures and angles we have to pin down retailing all suggest that the sector has been weakening and may now actually be so weak that it is in trouble.

And this of course comes with the U.K. perhaps on the precipice of Brexit. It is hard to know how much Brexit, Brexit preparations and Brexit fears may have distorted these data.

With December data complete, the quarter’s data are completed and the quarter-to-date metrics in the table show weakness. Retail sales volumes are off at a 0.8% annualized rate in the quarter. Passenger car registrations also show a sharp decline in the quarter. The CBI survey data all are weak in the quarter as well. In short, the fourth quarter has not been a good one for retailing in the U.K.

Of course, the big picture for the U.K. will be fleshed out by what happens to its Brexit stance. Today a host of top tier German leaders pleaded with the U.K. in a letter published in the Times to stay in EU. While the referendum vote was a clear British statement at the time, British opinion is thought to have shifted and British politicians do not seem to be able to come to terms with the Brexit conditions being imposed on them by the EU as a condition of its leaving. All of this puts Brexit up in the air as far as what it might be all way down to ‘will it even happen?’ As economic conditions change, the U.K. is still careening along a Brexit track but that still could change. In the meantime, economic sentiment and activity seem to be dissipating.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief