Global| Jun 18 2021

Global| Jun 18 2021U.K. Retail Sales Back Off in May

Summary

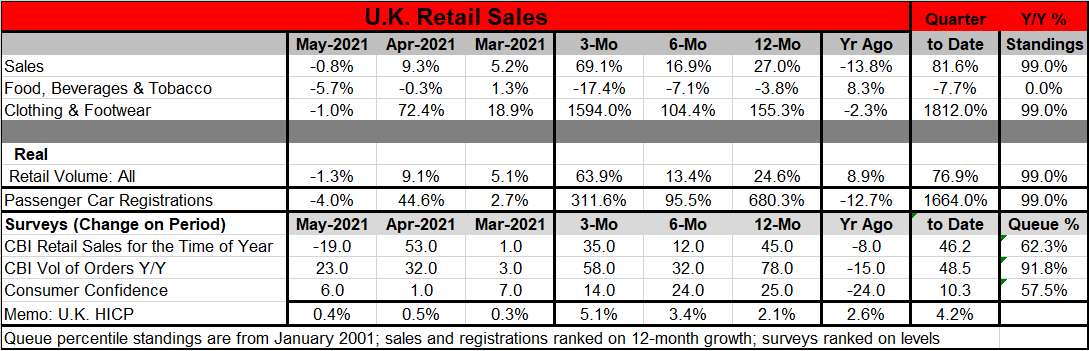

The step-back that refreshes U.K. retail sales fell by 0.8% in May but only after some really explosive gains in March and April as the U.K. economy began to lift restrictions. The chart shows the surge in retail spending. The ‘news’ [...]

The step-back that refreshes

The step-back that refreshes

U.K. retail sales fell by 0.8% in May but only after some really explosive gains in March and April as the U.K. economy began to lift restrictions. The chart shows the surge in retail spending. The ‘news’ this month is not so much that sales declined but rather how much of the previous enormous sales increases that were kept. That is evident in the three-month rate of growth at 69% annualized.

Pent-up demand meets opportunity

However, food and beverage sales fell sharply in May and fell for the second month in a row. These sales fell at a 17.4% annualized rate over three months. Clothing and footwear sales that fell by 1% in May are nonetheless up at a 1.5thousand percent annual rate (1,500%, not a typo, in fact nearly 1,600%) over three months annualized. I guess there was some pent-up demand there…

Retail volume and passenger car sales both fell in May, but both are up at extremely strong rates of change over three months.

The CBI survey weakens but is not weak

The CBI survey also logged a step back in May. Sales for the time of year fell to a -19 diffusion reading from +53 in April. The volume of orders for the time of year fell to +23 in May from +32 in April. Sales for the time of year still have a 62nd percentile standing – that is above its historic median standing. Orders for ‘time of year’ have a 92nd percentile standing. Despite the backtracking, orders still have a very strong reading.

Confidence gains footing

Consumer confidence rose to +6 in May from +1 in April, marking an above-median 57th percentile standing.

May, a month for the economy to catch its breath and to consolidate breadth

Clearly May was a step down from April. But March and April were months of very unusual strength as the U.K. economy began to open up after an extended lockdown. The strength of the three-month rates of growth make it clear that the story this month is one of strength and not one of weakness. The standings for overall sales and for footwear and clothing also are extremely high. This ranking on year-over-year growth rates is boosted by the recent rebound in sales as well as enhanced by the comparison of current sales to the period a year ago when the virus had impeded economic activity greatly.

Temperance and vigilance

Meanwhile in the U.K., inflation is starting to stir. The same is true in the U.S. and in EMU inflation has breached its inflation ceiling. Still, central banks are unanimous in treating these overshoots with forbearance given the long period of undershooting that generally preceded the overshoot and because there are a number of elements in the current inflation scene that appear to be temporary factors. Still, no one is quite sure what is temporary and what is going to have staying power so central bankers are showing temperance combined with vigilance.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief