Global| Jul 28 2020

Global| Jul 28 2020U.K. Retail Mounts a Comeback But It Has Its Limitations

Summary

The CBI U.K. retail sales survey moved sharply higher to the still weak reading of +4 in July, rising from the -37 reading logged in June after an abysmal -50 reading in May. At least the CBI survey has climbed back to positive [...]

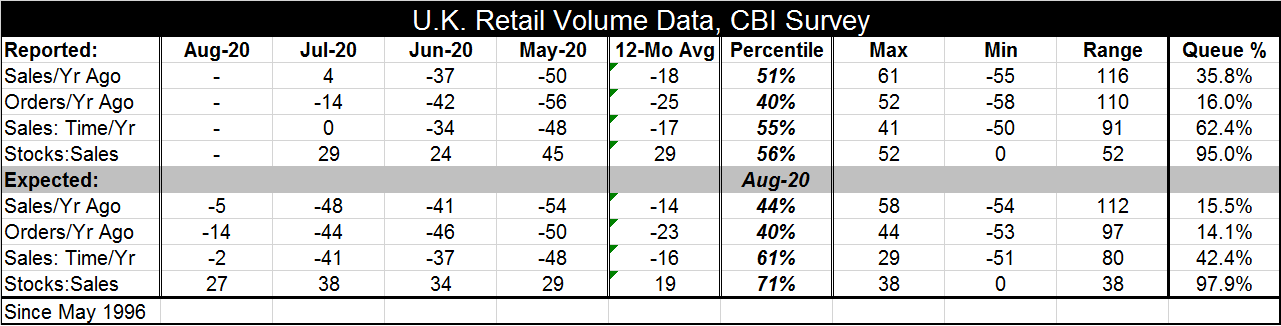

The CBI U.K. retail sales survey moved sharply higher to the still weak reading of +4 in July, rising from the -37 reading logged in June after an abysmal -50 reading in May. At least the CBI survey has climbed back to positive readings in July, but the queue standing of that reading is only in its 35.8 percentile. There is a clear snapback in the wake of the U.K.'s virus lockdown response. But it has not yet brought what could be called a return to normalcy and certainly not a snapback to make up for the lost sales in prior months.

The CBI U.K. retail sales survey moved sharply higher to the still weak reading of +4 in July, rising from the -37 reading logged in June after an abysmal -50 reading in May. At least the CBI survey has climbed back to positive readings in July, but the queue standing of that reading is only in its 35.8 percentile. There is a clear snapback in the wake of the U.K.'s virus lockdown response. But it has not yet brought what could be called a return to normalcy and certainly not a snapback to make up for the lost sales in prior months.

Orders compared to a year ago improved sharply from -56 in May to -42 in June to -14 in July but still have an extremely weak reading that standing in its historic 16th percentile when ranking year-on-year performances.

The year-on-year gain in sales for 'time of year' also has progressed from -48 in May to -34 in June to zero in July. This is a solid progression but still leaves sales for the time of year at a moderate 62.4 percentile standing. That, at least, is above its median (median occurs at a ranking of 50%).

The stock-sales ratio is moving lower steadily and yet it still has a 95th percentile standing. Stocks are heavy relative to sales and we know that sales are light generally and moderate for this time of year.

And the 'bad' news is...

The really bad news in this report is not that the progress is slow or disappointing. It is that expectations have still not kicked into gear.

The rankings for expectations readings are item by item lower than their respective counterparts for current activity – except for the stock sales ratio. And that is not a good exception since it takes a current stock-sales ratio that is exceptionally high and expects it to not improve and in fact to worsen.

Sales and orders metrics on the expected variables show a similar progression of improvement over the last few months, except that the progress for expectations has been slow, ponderous and less complete only making a strong move higher in August.

In August, expectations improve sharply making the largest month-to-month improvement over this period of time. However, it is the August set of readings that are ranked and that have still-weaker queue standings in August than the current variables have in July.

Based on these results we see that retail sales are indeed improving and have been improving relatively fast. Yet, even with stepped up progress in July, the forward assessment has been lagging.

At this point, there is nothing but speculation about how this will progress. The good news is that while expectations are being restored to normalcy at a lesser speed that current conditions they are nonetheless improving and made a huge move in August albeit one that still leaves expectations on a slower track back to normalcy than current conditions. We have no way of determining how this will progress. Despite the fact that expectations are improving more slowly than current conditions, both are continuing to improve.

Are policymakers paying a price for scaring everyone on the risk of this virus? The virus kills, that's for sure. But it kills sick people and very few healthy ones. The numbers of dead are growing large, but as a percentage of the population the numbers remain small and contained. The strategy of using lockdowns continues to cut every start of recovery short and put the economy back on ice for a time before reopening and rerunning the go-stop protocol again and… perhaps again and again. And that may be why expectations are improving so slowly. The future under this policy does not look very promising unless there is a vaccine and safe one that is discovered and that can be manufactured and distributed very quickly. The odds of all that happening fast are very speculative and seem rather remote.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief