Global| Feb 12 2021

Global| Feb 12 2021U.K. IP Fights Off Effects of Brexit and Corona

Summary

U.K. IP is fighting off two devastating blows. One is the transition to Brexit that is proving to be less seamless than Boris Johnson led many to believe. The other is the virus that exploded across the U.K. in December. Yet, [...]

U.K. IP is fighting off two devastating blows. One is the transition to Brexit that is proving to be less seamless than Boris Johnson led many to believe. The other is the virus that exploded across the U.K. in December. Yet, manufacturing output still managed a gain in December.

U.K. IP is fighting off two devastating blows. One is the transition to Brexit that is proving to be less seamless than Boris Johnson led many to believe. The other is the virus that exploded across the U.K. in December. Yet, manufacturing output still managed a gain in December.

As December began, the virus in the U.K. had moderated from its November peak and was infecting 13,430 per day. That was down from a spike peak of 33K per day on November 12. However, the view of coming containment and control of the virus was an illusion. As December progressed, the virus- a new more lethal and communicable strain- spread like wildfire driving the daily infection rate to a peak of 68,053 by January 8. From there, it has come back down to 13,494 per day on February 11. It is back to its early-December values. But that was not without a widespread and severe national lockdown to contain the virus spread. Despite those restrictions, manufacturing output continued to rise. During this time, the death rate tracked the infection rate with a lag as it usually does. By February 11, the death rate was clearly dissipating again but was still at an elevated mark above its early-December level. January should be another tough month for U.K. activity

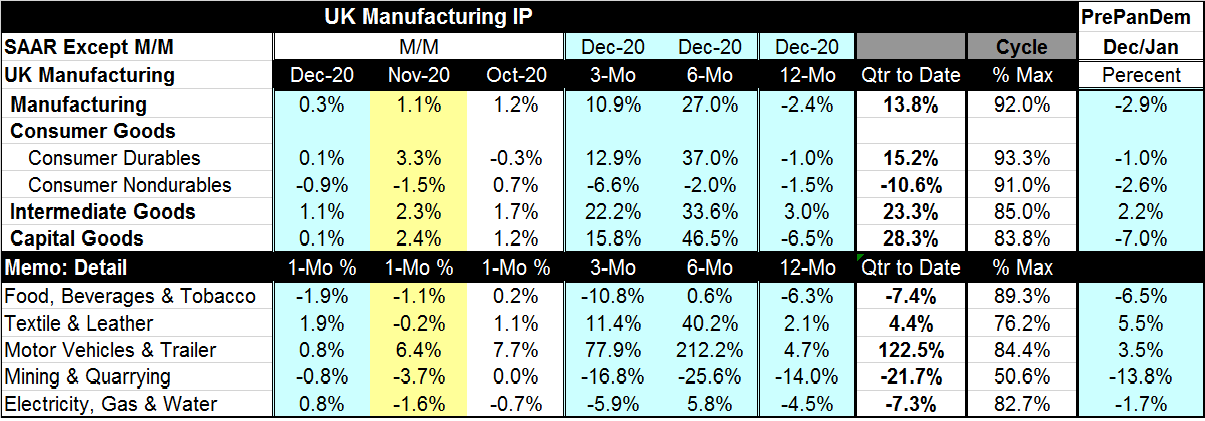

Industrial output in the U.K. managed to rise by 0.3% in December despite all the issues with Brexit, the virus and the lockdown. Consumer durables output rose by 0.1% while nondurables fell by 0.9%. Intermediate goods output rose by 1.1% while capital goods output eked out a 0.1% gain. Industrial output was more mixed with declines in mining & quarrying as well in food, beverages & tobacco. Gains were lodged in textile & leather, motor vehicles, and utilities.

The typical pattern for output in these virus-affected times is for 12-month growth to be weak, six-month growth to be extremely strong, with a pronounced slowing over three months. The U.K. follows this prescribed route as well. This pattern of output changes is thrust upon IP because of the way the growth periods interact with the virus on a calendar basis as the virus struck early in 2020, killed activity, then spawned a strong recovery and subsequently generated another wave of growth-damping infection and deaths.

Still, U.K. data are resilient with manufacturing output even posting strong 10.9% rate of growth over the most recent three months. Over three months consumer durables output, intermediate goods output and capital goods output all log growth rates in double digits. A decline in consumer nondurables output holds back manufacturing gains overall.

In the quarter-to-date, which now reflects Q4 over Q3 growth, output is up at a 13.8% annual rate. There are double-digit gains in consumer durables, intermediate goods and capital goods output. As is the case of three-month growth, quarterly average growth also shows a drop in nondurable goods output.

Looking at output since just before the pandemic set in (January to December), we find IP in December is still short of its January level by 2.9%. Consumer durables are short of their mark by 1% and consumer nondurables lag their level of January by 2.8%. Capital goods are below their January pace by a sizeable 7%. But intermediate goods output is up by 2.2% compared to its level of January 2020.

The U.K. seems have corralled if not controlled the virus now, but we know to be cautious with such assessments. The U.K. is dealing with the more lethal and communicable strain of the virus. It also is engaged in a rapid vaccine rollout to keep the virus at bay. Meanwhile, on the Brexit front, U.K. merchants seem to find new impediments in trade with the EU almost daily. The BOE has warned that the EU may be taking actions that will shift financial market activity to the EU from the U.K. Already the Amsterdam stock exchange has overtaken London in trading volume (more here). The benefits from Brexit have yet to show themselves.

Commentaries are the opinions of the author and do not reflect the views of Haver Analytics.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief