Global| May 11 2017

Global| May 11 2017U.K. IP Drops for the Third Month Running; BOE Meets and Holds Rates Steady on Split Decision

Summary

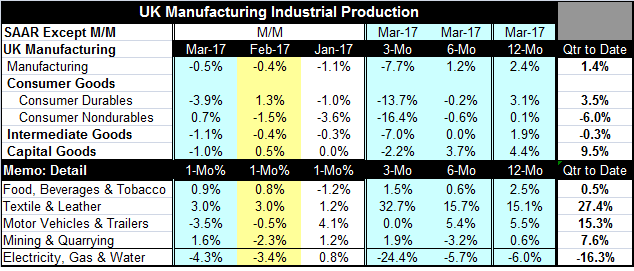

Pattern of vicious cycles hits U.K. IP; is it down for good? Industrial output in the U.K. has fallen for the consecutive third month. Oddly that leaves IP up in the quarter gaining at a 1.4% annual rate. That bit of oddness stems [...]

Pattern of vicious cycles hits U.K. IP; is it down for good?

Pattern of vicious cycles hits U.K. IP; is it down for good?

Industrial output in the U.K. has fallen for the consecutive third month. Oddly that leaves IP up in the quarter gaining at a 1.4% annual rate. That bit of oddness stems from IP having jumped in December, the last month of Q4 both raising output at the end of Q4 and giving output ahead of Q3 a higher platform for which to evolve. As a result, the output index in March after falling for three-months at a level 104.4 is still higher than October 2016 (102.8) and November 2016 (104.2). So growth in Q1 is an artifact of a data quirk, but the pattern is lower for the course of output during the quarter even if the quarterly average rises in Q1 relative to Q4.

Trend more broadly considered

Still, sequential growth rates show growth has been deteriorating more broadly from 12-month to six-month to three-month as growth fell from 2.4% over 12 months to a -7.7% pace over three months (here you see the sledge hammer effect of three straight monthly IP declines from an elevated base).

By sector

By sector the trend patterns are also hopeless as all show decelerating profiles from 12-month to six-month to three-month. That holds for consumer goods overall, for consumer durables separately, for consumer nondurables separately, as well as for capital goods and intermediate goods. The trends here are about as unequivocal as they get. And yet the Bank of England met amid this sort of news and one member thought that conditions were right for a rate hike. Really?

Knock on effects from Brexit knock before they arrive

Although the U.K. is being torn in different directions by the oncoming Brexit talks, there is still little clarity on Brexit and a major U.K. election looms in the meantime. The EU is taking a very hard line on the U.K. withdrawal and PM May has been resisting as best she can. She has called for an election to strengthen her hand ahead of negotiations with the EU, negotiations that promise to be brutal. The EMU not only wants to take a hard line to make the point that membership has its privileges but also as a deterrent to the rise in nationalism that has seen the popularity of the EU swoon on the continent. The EU wants to send a strong message to own membership that 'this could happen to you.' It is not exactly like waking up with a bloody horse head in the bed next to you (the Godfather), but it may be the next best thing. Banks are not waiting and are planning to move as many as 9,000 jobs -and probably quite well-paying jobs, too, out of the U.K.

The cushioning by sterling: is it enough?

The cushioning by sterling: is it enough?

However, the chart reminds us that through all of this the wisdom of the Bank of England under Mark Carney's leadership shows through. He cut rates sharply in the wake of the Brexit vote and did not lose time and wait to see the impact on the economy of Brexit. Although the economy did not immediately weaken, we are now seeing what he was worried about. That instant easing dropped the pound sterling sharply and provided a cushion of improved competitiveness for U.K. industry, a cushion that still is in place. However, there are concerns about who the U.K. exporters' customers will be in the future and on what terms. That helps to blunt the stimulative impact of this highly competitive exchange rate. The chart plots the 'real effective exchange rate' for the pound sterling which means it is a trade weighted (or multilateral) presentation of sterling's value and that the exchange rate pairs are compared in a framework that is adjusted for inflation differences. Certainly the low level of the pound on this gauge should be help to support U.K. industry. But as we can see from the data, the performance of U.K. industrial output is far from ideal. One interpretation of the chart is that the push from the weaker pound is already losing its impact.

Swing vote

Given the broad swings in industrial output, it is hard to cast a ballot for trend. The chart pictures something that is unusual for a real variable which is an explosive oscillating pattern- a pattern of cycles in which the 'highs' are sequentially higher and the 'lows' are sequentially lower. Obviously at some point, this sort of explosive oscillation will have to stop. But will it stop with a bang or a whimper?

Signage for growth and in a post-Brexalyptic world

The signs for the U.K. economy are not so good right now. Retail sales have been sputtering and are growing at pace of less than 2%. Money growth has flattened out and despite this competitive exchange rate, the U.K. visible account (goods trade) is showing a widening deficit. Just today The U.K. visible trade deficit was reported to have widened in March increasing to GBP 13.44 billion from GBP 11.44 billion in February. At today's meeting, the BOE kept policy unchanged, but one member did want to hike rates. It seems to me that the U.K. already has a lot of negative forces vying for attention and that it is not the right time to be thinking of slowing down growth. With Brexit in play, a lot of jobs, income and spending power will be leaving the U.K. economy. In the post Brexalyptic world (a new word I have coined, that I fear may become very useful, combines 'Brexit' with 'apocalyptic'), the U.K. may also find higher trade barriers, less import penetration and less free access to some foreign markets for its exporters. But it is still too early to know and maybe the EU will come to its senses (and maybe it won't). But there is a lot in play and many important things remain undecided. Still, don't make the mistake of waiting and assuming that in the course things being decided conditions will get better - they may not.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief