Global| Aug 15 2017

Global| Aug 15 2017U.K. Inflation in the Quandary Zone

Summary

The Brexit vote has thrown the U.K. economy into a tizzy as everyone is well aware. And while the government will have to conduct the actual exit negotiations, nowhere has dealing with Brexit and its new and yet unknown realities [...]

The Brexit vote has thrown the U.K. economy into a tizzy as everyone is well aware. And while the government will have to conduct the actual exit negotiations, nowhere has dealing with Brexit and its new and yet unknown realities posed a greater challenge than at the Bank of England. The BOE response to the Brexit vote was to prepare for shock of weakness by easing policy sharply. This act plunged the pound sterling in foreign exchange markets and that has helped to stoke-up inflation in the United Kingdom.

The Brexit vote has thrown the U.K. economy into a tizzy as everyone is well aware. And while the government will have to conduct the actual exit negotiations, nowhere has dealing with Brexit and its new and yet unknown realities posed a greater challenge than at the Bank of England. The BOE response to the Brexit vote was to prepare for shock of weakness by easing policy sharply. This act plunged the pound sterling in foreign exchange markets and that has helped to stoke-up inflation in the United Kingdom.

Challenges to the BOE policy

The challenge now faced by the BOE is whether to raise rates to counteract its own act of monetary stimulus or to wait out the inflation blister caused by a weak pound. Brexit weakness is slowly encroaching. But inflation has been fast-rising since the drop in the pound quickly led to gains in import prices. Whether policy 'stays the course on stimulus' or reverse probably has to do with how much or fast inflation - its policy side effect- is seen to be spreading.

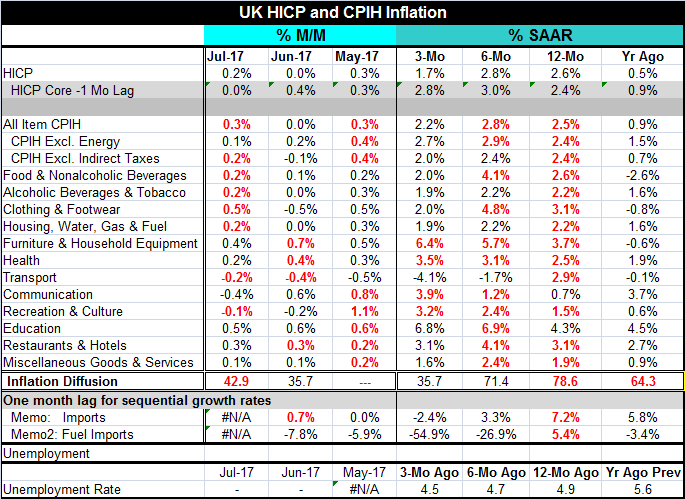

We have assembled the necessary prices in the table to assess these various forces on the U.K. economy. First of all, inflation is at 2.6% over 12 months, 2.8% over six months and 1.7% over three months. The headline path is reassuring.

Headline adjustment and headline vs. core

The first observation is that inflation is over the top of its target but not accelerating and in fact it may already have been cooling on its own. The core rate lags in terms of data availability. That lag alone may make its adjustment seem more sluggish. Presented on a lagged basis its year-on-year inflation rate is 2.4% over 12 months which rises to a 3% pace over six months and only dips to a 2.8% pace over three months. Core inflation is a month behind headline in terms of data availability and it does not show quite the same degree of reassurance as does the headline that inflation has fallen off and is on a downslope. Is that mainly a real effect or a data lag effect?

Inflation diffusion

One year ago in July 2016, U.K. inflation was rising by 0.5%. So it is not surprising that with year-on-year inflation running at 2.6% in July 2017, inflation diffusion - the breadth of inflation across categories - is up at 78.6 in July (78.6% of the categories are demonstrating increases in the pace of their year-on-year percentage gain). With headline inflation up to 2.8% over six months, inflation diffusion edges down to 71.4. But with inflation dropping off to 1.7% over three months, inflation diffusion has downshifted compared to six-month inflation to 35.7, a very low reading that reassures us that inflation is not accelerating and instead decelerating on a broad front across all categories.

Import prices

Import prices also suggest that the worst is behind the BOE as import prices gain 7.2% over 12 months, dropping to a pace of 3.3% over six months and dropping further to a pace of -2.4% over three months.

Energy import prices

This 'adjustment process' is being helped along by the weakness in energy prices as fuel prices rise by 5.4% over 12 months, drop at a rate of 26.9% over six months and drop at a faster pace of 54.9% over three months.

Cross currents

Clearly, the Bank of England is dealing with a variety of inflation-affecting macroeconomic forces. There are monetary induced effects reflecting the reverberation from its own policies. There are international oil effects that reflect the global oil market as well as broader supply-demand effects. There are in addition the macroeconomic effects from the state of its own economy and there is the impact as well of the not yet fully known impact of Brexit. But firms are leaving the U.K. and high-paid financial sector jobs are leaving London and the BOE really seems to have been on the right path with its policy that tries to cushion the economy against the impact of such losses.

The BOE balancing act

Did it overdo it and does it now need to pull back? The BOE's MPC will make that decision. But the evidence to pull back stimulus is not clear to me. There still seems to be economic weakness and more negative shocks in the pipeline. Meanwhile, the inflation pulse, which is there and has put inflation over the top of its target, is dissipating either rather quickly (headline inflation) or more slowly (core/ex food and energy inflation). Globally, weak energy prices are helping to suppress inflation forces. In this environment, I'd expect the BOE to continue to stand pat. It's not exactly in the cat bird's seat. But it has set something in motion which has done what it intended by providing some stimulus and has done so at the cost of inflation. But that cost or side effect, which once seemed to loom and grow, now appears to be contained. Brexit, like winter in the Game of Thrones, is still coming. It is probably not a good time to twist policy to fight inflation and to undermine growth ahead of a slowdown that is already being put in place by oncoming Brexit. Winter is coming...

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief