Global| Jan 03 2018

Global| Jan 03 2018U.K. Industry Continues to Post Solid Results

Summary

The Confederation of British Industry orders index flat-lined in December at its all-time high reading over the period since the European Monetary Union was formed. Export orders have moved up strongly as well but they are short of [...]

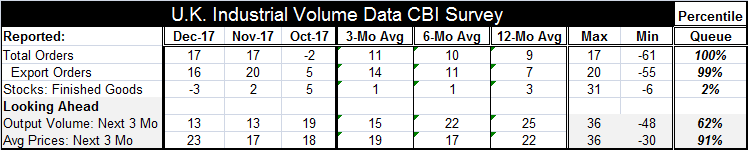

The Confederation of British Industry orders index flat-lined in December at its all-time high reading over the period since the European Monetary Union was formed. Export orders have moved up strongly as well but they are short of their high values on this timeline as they fell back off their own high reached in November as of December. Stocks registered a negative reading and that is a mark that has been lower only 2% if the time since 1990.

The Confederation of British Industry orders index flat-lined in December at its all-time high reading over the period since the European Monetary Union was formed. Export orders have moved up strongly as well but they are short of their high values on this timeline as they fell back off their own high reached in November as of December. Stocks registered a negative reading and that is a mark that has been lower only 2% if the time since 1990.

Looking ahead, the outlook for output volume remains flat in December at its November level. That reading has a much more midstream 62nd percentile standing- it is firm but also well short of the ebullient standing logged by orders. And the outlook shows ongoing slippage from 12-month to six-month to three-month. The outlook for prices, however, saw a jump in December although the trend for prices has generally been fading from a peak level reached back in February. The December price expectation reading, nonetheless, has a 91st percentile standing and has been stronger only about 9% of the time.

The recent PMI readings from IHS Markit confirm relatively strong manufacturing conditions in the U.K. but also chronicle month-to-month slippage. Still, ranked over the last six years, the Markit manufacturing PMI for the U.K. has an 80th percentile queue standing which is quite good. U.K. output and orders both are on rising tends but output, new orders and employment all slowed in December in line with the message from the CBO survey that sees some flattening out below the levels of recent peaks for the most part.

Of course, industry has generally done well in the wake of the U.K. Brexit vote with the stimulus action by the Bank of England that undercut the value of the pound sterling. The BOE is now in the process of gradually reeling back in some of that stimulus. Still, expectations ahead out to four months remain quite solid. But beyond that, U.K. firms will have to deal with the consequences of Brexit which remain a black box as negotiations drag on. For the time being, U.K. industry is on solid footing and has a constructive outlook for the near future. But the situation regarding Brexit will have to be ironed out for the better if these survey values are to persist when the U.K. makes its break with the EU.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief