Global| May 26 2015

Global| May 26 2015U.K. Distributive Trades Survey Shows Growth

Summary

On the whole the U.K. retail and wholesaling sectors are doing alright in Q2, but something is missing. The business situation for the U.K. retail sector rose to 20 in Q2 2015 from 11 in Q1. For wholesaling, the business situation [...]

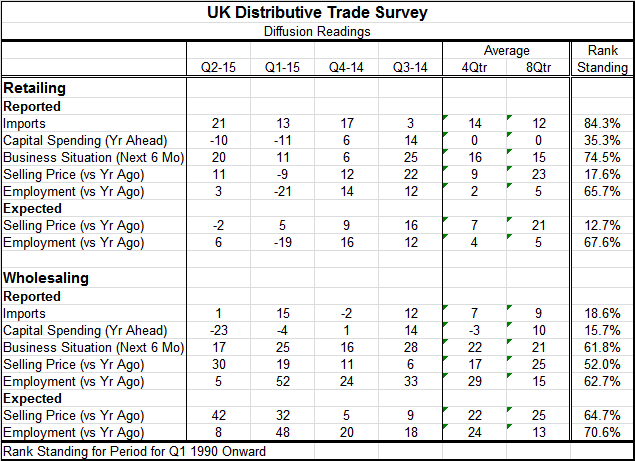

On the whole the U.K. retail and wholesaling sectors are doing alright in Q2, but something is missing. The business situation for the U.K. retail sector rose to 20 in Q2 2015 from 11 in Q1. For wholesaling, the business situation backed off to a 17 reading in Q2 from 25 in Q1. The retail sales sector reading sits in the 74th percentile of its historic queue of readings since 1990 while the wholesale reading sits in its 61st percentile. These are both expansionary readings with the retail reading the significantly stronger one. But both sectors show flagging investment plans.

On the whole the U.K. retail and wholesaling sectors are doing alright in Q2, but something is missing. The business situation for the U.K. retail sector rose to 20 in Q2 2015 from 11 in Q1. For wholesaling, the business situation backed off to a 17 reading in Q2 from 25 in Q1. The retail sales sector reading sits in the 74th percentile of its historic queue of readings since 1990 while the wholesale reading sits in its 61st percentile. These are both expansionary readings with the retail reading the significantly stronger one. But both sectors show flagging investment plans.

In retailing, all the current readings improved in Q2. The selling price compared to a year ago moved up to a 11 reading in Q2 from a -9 in Q1, a sharp improvement. Employment also moved sharply higher to 3 from -21. Imports jumped to 21 in Q2 from 13 in Q1 while capital spending expectations slipped slightly to -10 from -11.

In terms of the current reported percentile standings, imports have the strongest standing, in their 84th percentile, followed by overall business conditions in their 74th percentile. After that, employment is in its 65th percentile with capital spending falling below the 50% mark (its median reading) to a 35th percentile standing and with the selling prices in its 17th percentile. While business conditions are deemed relatively firm, there is a good deal of unevenness here.

The expected selling price also is weak in percentile standing terms, falling into its 12th percentile -indicating that the weakness in the current selling price is expected to continue. However, employment expectations show a pick up to 6 in Q2 from -19 in Q1 and a 67th percentile standing.

The wholesaling sector, by comparison, has a weaker business environment but stronger expectations on prices and employment.

Wholesaling found a drop in imports, contrary to the pattern in retailing in Q2. Capital spending in wholesaling continued its negative disposition and fell sharply too. However, wholesalers see a robust pricing situation for the selling prices in Q2 and with a much higher percentile standing than for retailing. Employment in wholesaling has nearly the same percentile standing as in retailing.

The wholesaling sector sees stronger selling prices and employment in its outlook than does retailing.

On balance, both the wholesale and retail sectors show firm results. What weakness there is seem mostly confined to pricing trends (and there, mostly in retailing) and in capital spending (both sectors). That weakness is enough reason to give some to pause to any view of strength for the sector. Not seeing capital spending step up and seeing it weak to boot is a red flag on true sector performance.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief