Global| Nov 19 2019

Global| Nov 19 2019U.K. CBI Survey Shows Some Improvement- Still Very Weak

Summary

The Confederation of British Industry (CBI) industrial trends survey showed some improvement in the U.K industrial sector in November, but it is better to focus on where the readings stand than on how much they may have changed month- [...]

The Confederation of British Industry (CBI) industrial trends survey showed some improvement in the U.K industrial sector in November, but it is better to focus on where the readings stand than on how much they may have changed month-to-month.

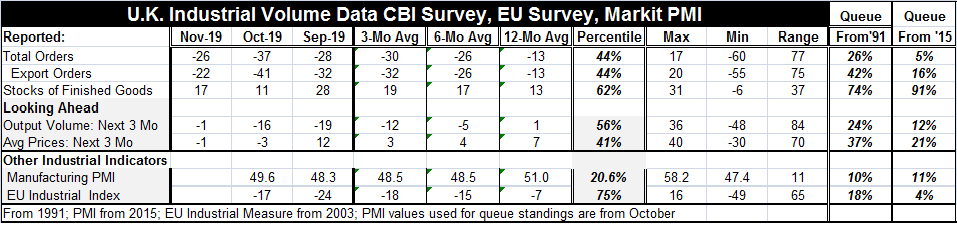

The Confederation of British Industry (CBI) industrial trends survey showed some improvement in the U.K industrial sector in November, but it is better to focus on where the readings stand than on how much they may have changed month-to-month.

This point-of-view directs your attention immediately to the graph and to the far right-hand columns of the table that produce rankings of the current (left column) observations in their historic queues of data on two timelines, one from 2015 and the other from 1991. Compared to the more recent period, current U.K. data are extraordinarily weak with metrics ranking in their bottom 20th percentile or even much lower for the most part. The exception is inventories which rank at a strong 91st percentile standing - and that is even worse. Having high-ranking inventories vs. low-ranking orders and sales is a problem either in the making or in hand.

Ranked data over the longer period from 1991 are not nearly as disastrous but are still clearly weak. Here again rankings are weak and all are below their historic medians on this timeline (a rank of 50% marks the median) with only inventories as an exception. Again that is not a good result. Orders have a 26th percentile standing. Foreign orders have a 42nd percentile standing; but with Brexit about to happen and the uncertainty of how U.K. goods shipments to the EU would be treated, it is best to take any strength in exports with a grain or two of salt. Looking ahead, output volume over the next three months has a 24th percentile standing despite its month-to-month improvement. Expected prices have a 37th percentile standing. Other industrial indicators that are up to date only through October have even weaker standings on data back to 1991 as well as more recently.

Having made that point, there is some improvement in train month-to-month and that is across the board. All the November readings are above their respective three-month averages, marking the rebound as real and not just as a volatile month. Current metrics are close to their six-month average values for the most part and are weaker than their 12-month averages. That progression shows that whatever rebound is in force does not result any sense of restoring recent normalcy. The graph also makes that clear.

The U.K. is undergoing nationwide elections with the hope that once the government is re-set there will be a clearer path to Brexit that will reflect a voter consensus. Still, there is plenty of room for this process to run afoul of events and Brexit has been a surprising, sticky and divisive issue in the U.K.

The global environment continues to reflect a slowing world economy, but one that has showed some recent resilience as global markets have raised interest rates. There is hope for a U.S.-China trade deal to reinvigorate the global trade picture. However, the two biggest special factors dogging the U.K. manufacturing sector, Brexit uncertainty and slowing world trade remain in force. But there is some optimism on the prospect for change on both fronts.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief