Global| Apr 22 2021

Global| Apr 22 2021U.K. CBI Optimism Speaks Volumes

Summary

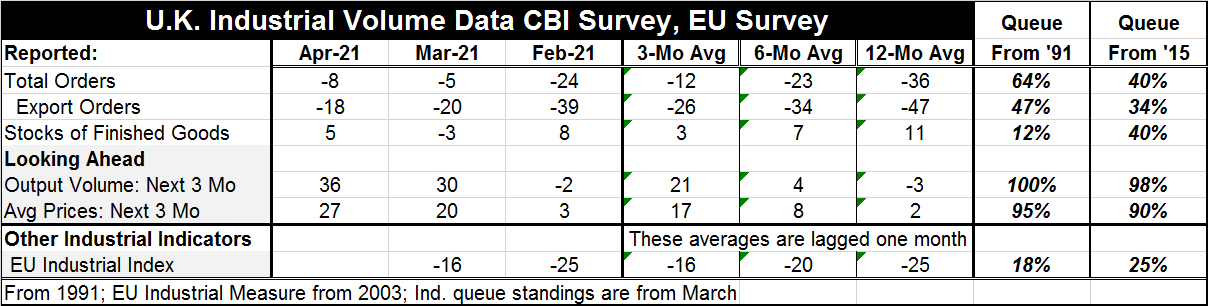

The U.K. Confederation of British Industry (CBI) survey saw its order component backtrack in April falling to -8 from -5 in March even as optimism on future output expectations gained purchase. Total orders have a queue standing in [...]

The U.K. Confederation of British Industry (CBI) survey saw its order component backtrack in April falling to -8 from -5 in March even as optimism on future output expectations gained purchase. Total orders have a queue standing in their 64th percentile on data back to 1991 but are below their median at a 40% standing on a shorter series ranking back to 2015.

The U.K. Confederation of British Industry (CBI) survey saw its order component backtrack in April falling to -8 from -5 in March even as optimism on future output expectations gained purchase. Total orders have a queue standing in their 64th percentile on data back to 1991 but are below their median at a 40% standing on a shorter series ranking back to 2015.

Export orders, a component part of total orders, have picked up slightly month-to-month to a reading of -18 in April from -20 in March. This is curious since the U.K. has begun to open up its economy and reduce virus-related restrictions on activity while Europe, where a lot of U.K. trade still goes, continues to struggle with the virus and low rates of vaccination. Logic would suggest the overall orders reported by the CBI which include domestic orders should strengthen first; yet, that is not what is happening. That divergence may be a reflection of just how much the manufacturing sector (tradeable goods sector) has come to insulate itself from local virus conditions. It could contrarily reflect a shift of business to the U.K. from the domestic market in Europe where conditions have weakened. So we will have to continue to monitor this situation to see what is driving the U.K. orders series and just how strong Europe gets and how soon it gets there. In any event, there is also this finding: export orders ranked on the two horizons are, in fact, weaker than total orders on both ranking horizons.

Looking ahead, U.K. industries hiked their expectations for output volume tremendously in March and have continued to lift expectations in April. Output volume in the next three months leapt to +30 in March from -2 in February and now in April volume expectations are up to +36, another solid if much less spectacular monthly rise that extends the gains made in March through the month of April. The March month-to-month jump in expected output is, in fact, the second strongest monthly gain in the series back to the year 2000, a period of over 20 years. Coming as the U.K. is still fighting off virus issues and adjusting to post Brexit trade relations, this reading has to be scored as a very unexpected and pleasant result. The fact that April was able to build on such a strong monthly gain is another encouraging sign.

As a result of this shift up in expected output, the level of the reading for the expected output metric (for three months ahead) this month is the highest on record back to 1991 and of course gets the highest ranking possible over the 2015 span as well. Despite a rather blasé attitude toward inflation by global central bankers, the CBI survey respondents put the assessment of average prices over the next three months as much higher mirroring the movement posted in expected output. Maybe the world is Keynesian after all or maybe producers just think that it is. In any event, expected prices jumped from +3 in February to +20 in March and have risen again in April to +27 and to a 95th percentile standing on data back to 1991 (meaning that the April reading is this high or higher 95% of the time).

Putting a different spin on these data is the one-month lagging industrial index from the EU Commission. This ‘up minus down’ diffusion index at the table bottom also rose significantly in March rising to -16 from -25 in February, but that gain only boosted it to an 18th percentile standing since 1991 and a 25th percentile standing since 2015. The one-month change in the EU index was only at about the 50% mark of all ranked changes, stigmatizing March as an ‘average gain’ not a spectacular gain as in the CBI survey. Notice also that whereas CBI rankings are higher over the longer period for the EU Commission index ranking is higher over the shorter period. The weaker standing of the lagging EU index suggests that breadth may not be as solid as the CBI gauge asserts. And while the overall assessment of the EU Commission index falls well-short of what the CBI index says (comparing ranking evaluations), both surveys point to a substantial-to-solid improvement in U.K. manufacturing beginning in March. That agreement between the two surveys is good news.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief