Global| May 02 2017

Global| May 02 2017The EMU Unemployment Rate Steadies at Recent Low

Summary

The EMU unemployment rate remains low. The EMU rate in March stabilized at February's cycle low. In February, four of 11 of these early EMU members saw their unemployment rates fall. Only Austria saw its rate rise in February. In [...]

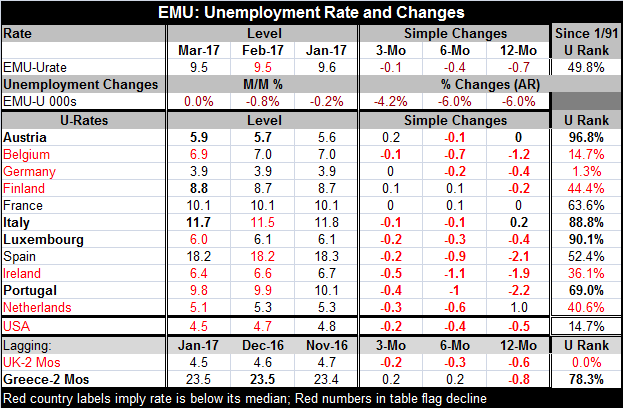

The EMU unemployment rate remains low. The EMU rate in March stabilized at February's cycle low. In February, four of 11 of these early EMU members saw their unemployment rates fall. Only Austria saw its rate rise in February. In March, five of these members saw rates fall as three others saw their rates rise. It is too early to take that as a sign of prevarication in progress. Of the 11 earliest EMU members, seven have their unemployment rates lower on balance over three months. Nine had their rates fall over six months. Seven have unemployment rates lower on balance over 12 months.

The EMU unemployment rate remains low. The EMU rate in March stabilized at February's cycle low. In February, four of 11 of these early EMU members saw their unemployment rates fall. Only Austria saw its rate rise in February. In March, five of these members saw rates fall as three others saw their rates rise. It is too early to take that as a sign of prevarication in progress. Of the 11 earliest EMU members, seven have their unemployment rates lower on balance over three months. Nine had their rates fall over six months. Seven have unemployment rates lower on balance over 12 months.

Austria and Finland have unemployment rates higher on balance over three months. Finland and France have rates higher over six months. Italy and the Netherlands have their respective rates higher on balance over 12 months. Also over 12 months, France and Austria have rates that are unchanged.

Meanwhile, the EMU inflation rate has popped up to the 2% mark, but just as suddenly it has lost all of its momentum as flagging global oil prices have actually backtracked and OPEC is looking for Plan B to control the price slide.

On the whole, the ongoing improvement in Europe's economy seems to be still on track. However, a few countries seem to be 'inoculated' against progress such as Austria, Italy and Luxembourg. But five of 11 countries now have unemployment rates below their respective medians (Germany, Belgium, Ireland, the Netherlands, and Finland). While headline inflation has returned to the 2% mark, core inflation is well below it and ECB's position is that headline inflation is not broad and has mostly been driven by weak oil prices. It plans to keep stimulus in gear.

According to this unfolding view, Europe's progress still has a way to go. The EMU unemployment rate has been lower only about half the time with a queue standing at its 49.8 percentile mark very near its median. The midway mark for unemployment should not be construed as a low point or as the place where Keynesian-like bottleneck inflation pressures set in. Only Germany and Belgium have extremely low unemployment rates. For most of the rest of Europe, countries will be looking to let stimulative polices run to further reduce their respective unemployment rates. However, the ECB's policy directive is written only in terms of inflation. For the moment, Mario Draghi has a strategy. Draghi's view on inflation being not broad-based fits into the view of keeping stimulus in play to allow for further unemployment progress across the euro area- at least for now.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief