Global| Jul 07 2016

Global| Jul 07 2016Surprise Drop in German IP

Summary

Weakness on the doorstep and Brexit looms German IP dropped 1.3% in May, marking its third drop in four months as well as its fifth drop in seven months. The IP drops in May and March are large, each in excess of 1%, while the April [...]

Weakness on the doorstep and Brexit looms

Weakness on the doorstep and Brexit looms

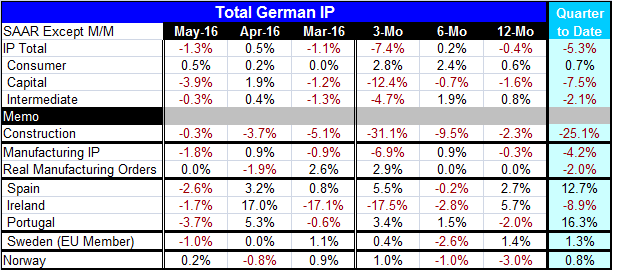

German IP dropped 1.3% in May, marking its third drop in four months as well as its fifth drop in seven months. The IP drops in May and March are large, each in excess of 1%, while the April IP gain is smaller at only 0.5%. Thus, the trends in play are not encouraging and these are, of course, pre-Brexit statistics. Germany has a good deal of trade with the U.K. and with Brexit it acknowledges that trade relations will need to be recast. In the meantime, it is unclear how much ongoing commerce might be affected by unclear expectations.

Estimated Brexit impact

However, in a new survey, the Association of German Chambers of Industry and Commerce (DIHK) projects a drop in German exports to the U.K. of 1% this year and of 5% next year on forecasts that have tried to capture the expected Brexit impact.

German IP trends by sector

German IP is falling over three-months (rapidly) and over 12-months, with a very slight gain (0.2%, annualized) over six-months. Consumer goods output is relatively firm with growth rates building from 0.6% over 12-months to 2.4% over six-months and 2.8% over three-months. However, capital goods output has been losing momentum. Output is down sharply in two of the last three months and is falling at a 12.4% annual rate over three-months and declining on all three horizons from 12-months from six-months and from three-months. Intermediate goods output is falling by 4.7% over three-months and has suffered declines in two of the most recent three months as well. But intermediate goods output is growing over 12-months and six-months with a solid 1.9% pace over six-months.

German construction sector

Germany's construction sector is weakening. The German construction sector index for June was at a 10-month low on the Markit diffusion index, albeit with a value barely above 50. But in May the German construction sector IP was lower by 0.3% and its down for three consecutive months. Construction sector output is falling at a 31.1% annualized pave over three-months with declines on six-months and 12-months as well and with downward momentum steadily gathering pace.

Manufacturing struggles

The German manufacturing sector logged a drop of 1.8% in May and is lower in two of the three recent months; real manufacturing orders are falling in May and lower by 1.9% in April. While manufacturing IP is falling at nearly a 7% annualized pace over three-months, real orders are up at a 2.9% pace. But manufacturing IP is hardly strong with a six-month annualized pace at 0.9% and a 12-month drop on the books. Over six-months and 12-months, real manufacturing orders are dead flat. The manufacturing sector signals are not encouraging.

Quarter-to-date (two months into Q2)

Moreover, in the quarter-to-date, overall IP is lower with only consumer sector output higher. Construction sector orders off at a 25.1% annualized rate; overall manufacturing orders are lower and real orders are lower.

Early-reporting Europe

The rest of early-reporting Europe shows output declines in May as well with Spain, Ireland, Portugal, and Sweden all showing substantial output declines in May. However, only Ireland has output declining over three-months and only Ireland has a decline in the quarter-to-date. But the rest of Europe is not exactly solid except for May as four of these five European reporters (Norway included) show output drops over six months as well as weakness in May.

German competitiveness erodes

In a recent study by Swiss business school IMD, Germany is shown to have dropped two places in the global competiveness rankings and is now down to 12th place globally after being as high as 6th in 2014. Germany still has a highly skilled work force, but firms assessing German competitiveness have cut its score because of Germany's complicated tax structure.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief