Global| Jan 11 2021

Global| Jan 11 2021Spain's IP Still Struggles to Attain Year-Ago Levels As the Virus Circulates and Mother Nature Offers New Challenges

Summary

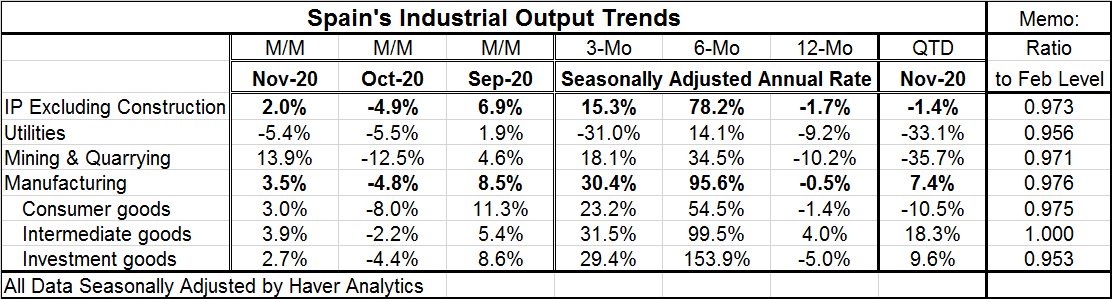

Spain continues to reel under the effects of the coronavirus. Of the various total and sector data in the table, only intermediate goods output is back at its level of February 2020, just before the virus slammed into Europe. Among [...]

Spain continues to reel under the effects of the coronavirus. Of the various total and sector data in the table, only intermediate goods output is back at its level of February 2020, just before the virus slammed into Europe. Among the various industrial totals and sectors, only the sector 'intermediate goods' has a year-on-year gain in November- all other metrics in the table show 12-month declines. However, all metrics except utilities show strong gains in output over three months. Although in all cases, those gains are a slowdown compared to the skyrocketing results over six months.

Spain continues to reel under the effects of the coronavirus. Of the various total and sector data in the table, only intermediate goods output is back at its level of February 2020, just before the virus slammed into Europe. Among the various industrial totals and sectors, only the sector 'intermediate goods' has a year-on-year gain in November- all other metrics in the table show 12-month declines. However, all metrics except utilities show strong gains in output over three months. Although in all cases, those gains are a slowdown compared to the skyrocketing results over six months.

The chart shows an uneven path for Spanish output and that leaves an unclear future. The manufacturing sector is still declining over 12 months on balance, but the manufacturing PMI gauge is continuing to improve. But the level of Spain's manufacturing PMI in November slipped to 49.8 from 52.5 in October. The gauge is once again above '50' indicating output expansion in December. But the whole economy matters and manufacturing must make its contribution in the context of how the economy is doing. Spain's services PMI, as of December, logs its fifth straight month below '50' indicating ongoing contraction in the services sector. This adverse trend is a headwind that manufacturing is trying to make progress against. The readings for Spain's PMIs in December, a month ahead of the IP data, find the manufacturing PMI with a 33rd percentile standing and services PMI with an 11.9 percentile standing; both are well below their respective historic medians on data back to January 2016. Despite the manufacturing PMI edging above '50' in December, Spain is continuing to struggle to post growth.

The Spanish virus

The virus is very active and its spread is accelerating in Spain. Spain's Friday data for new infections at 25,456 is the highest daily total on record surpassing all the peak reading in late-October. However, the good news for Spain is that this third wave has not been as lethal as the death total remains well below the peaks of April 2020 and also well below the peaking of November 2020. The January 8 death total at 199 compares to a peak of 537 on November 24 of last year and a peak at 996 on April second of last year. The deaths bear no resemblance to the year ago peaks even though the number of new infections has risen sharply (source). There are two factors operating here. One is that medicine has learned better how to deal with the virus. The other is that the virus kills more easily those who have compromised immune systems. As the virus kills the weakest in a community, it no longer has them to prey upon.

More challenges for Spain

Still, the spread of the virus is worrisome and Spain is also in the process of distributing vaccine. However, Mother Nature is intervening and a massive snow storm has crippled transportation. Spanish authorities are working overtime to try to remove the snow before temperatures drop and make road clearing even more difficult. Current efforts are trying to keep roads clear so that the vaccine distribution program can continue. CNN reports that the Spanish government is sending out the Covid-19 vaccine and food supplies in convoys (source). The heaviest snowfall in Spain in decades fell on January 10 in Madrid.

Across Europe

Spain's statistics are unique. What we see as we gaze across other large European economies is that other countries are experiencing their own and different patterns as well. The distribution of vaccine is charging after and trying to subdue a new wave of infections across Europe. For the most part, there is concern about the virus spreading even though in many places the death tolls are lower that in past peaks.

• The United Kingdom is an exception. In the U.K., there is a new variant that appears to be more communicable and is faster spreading. There, the virus spread has accelerated to new highs and the death total is above its April and November totals as well (source).

• In Germany, there is a hint that the recent accelerated spread is flattening out its pace but the death toll has hit a new high in Germany; however, it currently seems to be backing off from its highest death toll reading posted on December 29 (source).

• France is a wholly different situation with daily cases having made their all-time peak in early-November and with new cases currently showing signs of dissipating and at level far below their previous peak. Deaths in France are still elevated but gradually being reduced (source).

• Italy is another large EU member where the spread is well off its peak that was reached around mid-November. But in Italy, infections show signs of picking up again. Deaths in Italy reached a peak in early-December at a new high just above their March peaks. Since then, the death toll by day has been reduced, but it also shows some sign of possibly rising again (source).

There is no single overarching description of the position that Europe is in other than 'still fighting off the spread.' This makes policymaking much more difficult since the EMU area runs with a single monetary policy, but individual countries do have their own fiscal policies and responses to the virus. Right now the U.K., no longer an EU member and never a single currency participant, seems to be having the hardest time corralling the spread and reducing the death toll.

In sympathy these European trends U.S. infections have been rising to a new peak of 307,911 reached on January 8 with subsequent days' infections lower. But the death curve in the U.S. has continued to rise and is ahead of its peak of April 2020. It is unclear if the death curve is still rising in the U.S. or not.

Outlook and the virus

These samplings of the virus cycle make it clear that the virus remains a major problem for policy. And while the emergence of approved vaccines were the good news stories of last year, vaccines take time to manufacture, to rollout, to distribute and to actually finish the act of inoculation. In some ways, policy has fallen behind and the virus which seems to have jumped ahead despite the vaccine distribution piggy-backing on lax social distancing measures during the holiday season in December. Scientists are working to try to find solutions to getting more inoculations and to getting them sooner. This phase of fighting a rising tide of infections is probably going to last a little longer- probably to the end of the month. Science can only do so much with the supply of vaccine that is available and the limitations of vaccine production.

The virus trends and the existence of ongoing and new lockdowns that have begun to sink oil prices raise further questions about where global growth and industrial output will go in the short to medium term. There is still optimism riding on the back of the various vaccines, but public policy and social distancing requirements will remain in effect for some time if the vaccine is to make gains on the spread especially in the U.K. where the new variant has raised the hurdle for policy challenge.

Commentaries are the opinions of the author and do not reflect the views of Haver Analytics.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief