Global| Dec 30 2014

Global| Dec 30 2014Spain's Inflation Makes Sharp Deceleration

Summary

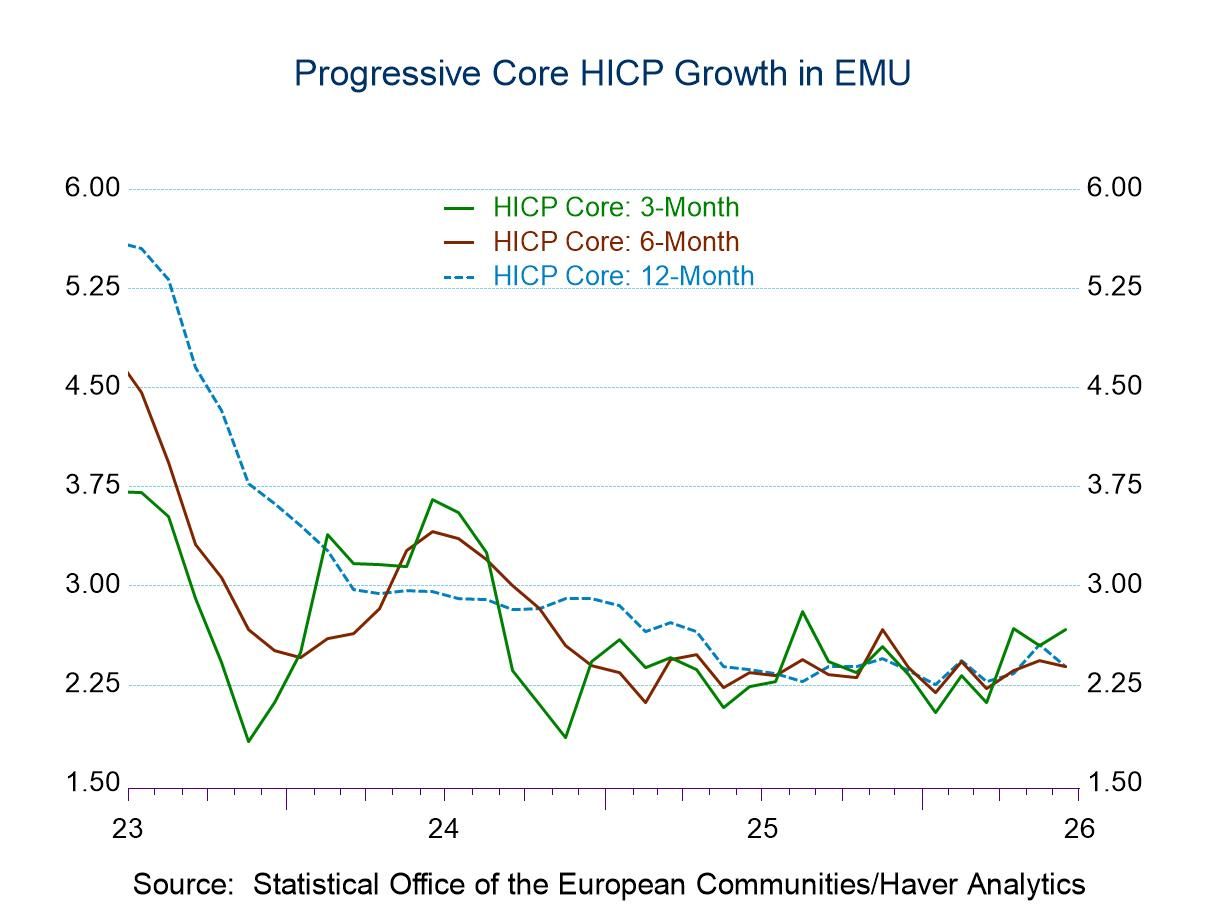

With the European Monetary Union grappling with inflation and unsure what to do next, in some countries, the decision seems clearer than in others. Unfortunately, EMU monetary policy is one for all and all for one. In the chart, we [...]

With the European Monetary Union grappling with inflation and unsure what to do next, in some countries, the decision seems clearer than in others. Unfortunately, EMU monetary policy is one for all and all for one. In the chart, we plot Germany's HICP vs. Spain's HICP. Since mid-2013, Spain consistently has been doing something unusual: it has been running a lower rate of inflation than Germany. This has helped Spain to catch up on some of the competiveness it lost to Germany since joining the EMU. Germany previously had run the lowest inflation rate in the EMU- no more. In the last few months, Spain's inflation rate has turned more sharply lower.

With the European Monetary Union grappling with inflation and unsure what to do next, in some countries, the decision seems clearer than in others. Unfortunately, EMU monetary policy is one for all and all for one. In the chart, we plot Germany's HICP vs. Spain's HICP. Since mid-2013, Spain consistently has been doing something unusual: it has been running a lower rate of inflation than Germany. This has helped Spain to catch up on some of the competiveness it lost to Germany since joining the EMU. Germany previously had run the lowest inflation rate in the EMU- no more. In the last few months, Spain's inflation rate has turned more sharply lower.

Both Germany and Spain are net energy importers. But the weak energy price is creating an environment or coming in environment in which prices in Spain are falling relatively faster than in Germany. It is too soon to know what the cause is for this. Since 2013, the cause has been a weaker Spanish economy and that may still be the operative reason.

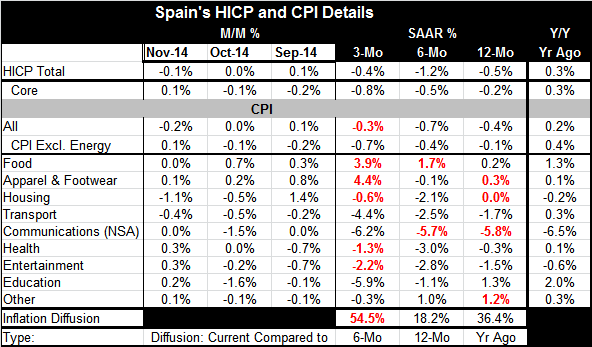

Looking at the performance of Spain's inflation, we see that, of the nine major categories, seven showed declines over three months, eight show declines over six months and four show declines over 12 months with one category's inflation rate unchanged over 12 months. Inflation diffusion measures the breadth of inflation's rise over a given time horizon. For example, over three months, we see diffusion is up slightly compared to six months (diffusion at 54.5% is above the neutral 50% reading). But over six months and 12 months inflation's breadth clearly is decelerating with very low diffusion readings of 18% and 36%, respectively.

Spain clearly is seeing a lot of prices weakness. Its inflation rate has been weaker historically on only two occasions, one of them just a few months ago, the other in the depths of the financial crisis. The details on inflation by category come for Spain's national price index, not from the HICP. But both measures show about the same -0.5% in headline inflation over 12 months and a core drop of about 0.2% over 12 months.

Spain's inflation trends are poor. It would be good that inflation were declining if it were higher. But it is not. A condition of falling prices is not what you want to see, especially with inflation still trending even lower. But EMU members sees that trend in different degrees and we find members with differing views and resolve about how to deal with adversity, each with a different degree of adversity. These differences make policy-making difficult.

While the chart above may seem to show much the same general `trend' for German inflation as for Spanish inflation, there are two critical differences. One is that in Spain prices are falling. The second is that in Spain the trend lower has become even sharper. What may look like similar circumstances at first glance is not.

With lower oil prices, the Bundesbank in Germany has been talking of hiking its growth outlook. Since Europe is a net oil importer, lower oil and energy prices will help European growth. But since energy is so highly taxed in Europe relative to the U.S., there will be less of a bump than in the U.S. Europe still has many challenges and we should not expect that a bout of lower oil prices of unknown duration will be Europe's savior. Its structural issues run too deep to be solved so easily.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief