Global| Jul 11 2006

Global| Jul 11 2006Small Business Optimism Continued Lower

by:Tom Moeller

|in:Economy in Brief

Summary

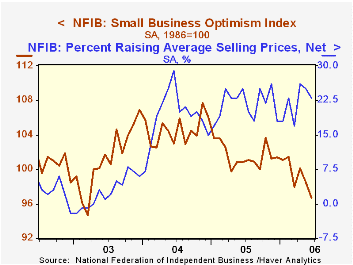

Small business optimism in June fell another 1.8%, according to the National Federation of Independent Business (NFIB). It was the fourth m/m decline this year. During the last ten years there has been a 70% correlation between the [...]

Small business optimism in June fell another 1.8%, according to the National Federation of Independent Business (NFIB). It was the fourth m/m decline this year.

During the last ten years there has been a 70% correlation between the level of the NFIB index and the two quarter change in real GDP.

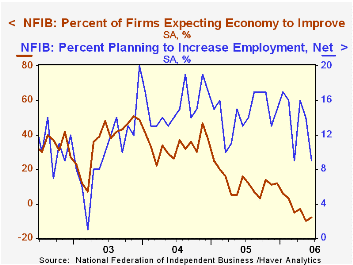

Respondents expecting the economy to improve rose slightly m/m but remained near the lowest level since early 2001.

The percentage of firms planning to increase employment slipped back to the lowest level since 2003. The number of firms currently with one or more job openings remained stable but off from the April high. During the last ten years there has been a 72% correlation between the NFIB percentage and the y/y change in nonfarm payrolls.

The percent planning to raise capital expenditures fell moderately to a new low (27%) since 2003..The percentage of firms planning to raise average selling prices slipped to 29%. The percentage of firms actually raising prices also fell m/m to 23% but remained up versus a 22% average last year. During the last ten years there has been a 60% correlation between the change in the producer price index and the level of the NFIB price index.

About 24 million businesses exist in the United States. Small business creates 80% of all new jobs in America.

| Nat'l Federation of Independent Business | June | May | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Small Business Optimism Index (1986=100) | 96.7 | 98.5 | -4.1% | 101.6 | 104.6 | 101.3 |

by Tom Moeller July 11, 2006

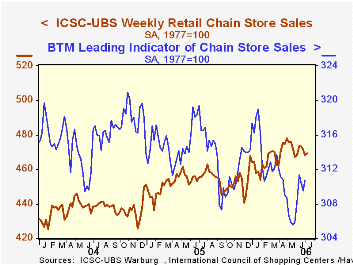

The International Council of Shopping Centers (ICSC)-UBS indicated that chain store sales ticked 0.2% higher during the opening week of July following two consecutive weeks of decline.

As a result, sales began the month 0.4% below the June average which fell 0.4% from May. During the last ten years there has been a 47% correlation between the y/y change in chain store sales and the change in nonauto retail sales less gasoline.The ICSC-UBS retail chain-store sales index is constructed using the same-store sales (stores open for one year) reported by 78 stores of seven retailers: Dayton Hudson, Federated, Kmart, May, J.C. Penney, Sears and Wal-Mart.

The leading indicator of chain store sales from ICSC-UBS rose 0.4% (-2.1% y/y) following two consecutive weeks of 0.3% decline.

| ICSC-UBS (SA, 1977=100) | 07/08/06 | 07/01/06 | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Total Weekly Chain Store Sales | 469.2 | 468.3 | 3.0% | 3.6% | 4.7% | 2.9% |

by Tom Moeller July 11, 2006

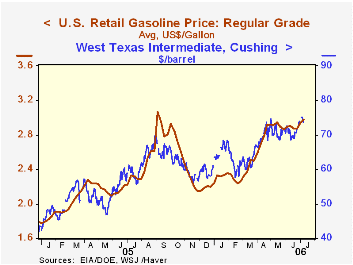

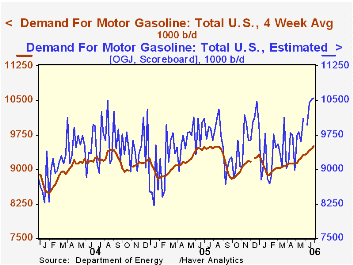

Retail gasoline prices rose another four cents last week to an average $2.97 per gallon (27.7% y/y).

Demand for motor gasoline was quite strong during June. According to the Oil and Gas Journal's estimates, demand rose 5.6% from the May average and rose 6.5% from June of 2005. The US Dept. of Energy's figures peg demand up as well but to a lesser degree

Yesterday, in spot market trading the price for a gallon of regular unleaded gasoline fell seven cents to $2.13. In 2005 petroleum companies began eliminating MTBE from reformulated gasoline (RFG) and have replaced it with ethanol. The last remaining markets for MTBE RFG are in the final stages of switching to RBOB (Reformulated Blendstock for Oxygenate Blending). As a consequence, prices for RFG in the Haver databases are being discontinued and new regular and premium RBOB prices are being added.

The New York Mercantile Exchange introduced a RBOB futures contract in January and traders are gradually migrating to the new RBOB contracts. RFG contracts will end with the January 2007 contract. While these changes are important, two-thirds of all gasoline consumed in the US is still conventional and not impacted by these changes.

The domestic spot price for a barrel of West Texas Intermediate fell for the third straight day on Monday. Nevertheless, at $73.63 per bbl. the price was nearly 4% higher than last month's average.

What the Fifth District's only major oil refinery explains about high gas prices in the wake of Hurricanes Katrina and Rita from the Federal Reserve Bank of Richmond is available here.

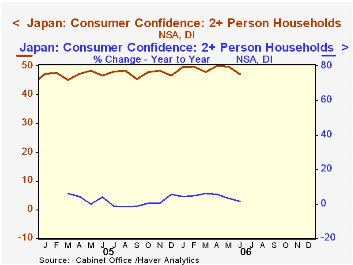

Japanese Consumer Sentiment Wavers: Price Expectations Suggest that Concern over Inflation Is Replacing that over Deflationby Louise Curley July 11, 2006

Consumer sentiment among Japanese households with two or more persons declined to 47.2 from 49.8 in May according to the Cabinet Office's diffusion index. The decline was greater than expected and resulted in the lowest value of the index so far this year. To illustrate the weakening of consumer confidence, we have plotted the index of consumer confidence and its year over year increase in the first chart. (Since the monthly data are available only from Jan 2004, there are only two and a half years of data.) The year over year percentage change in the diffusion index is an indicator of the trend in the diffusion index. In recent months the year over year percentage change has declined from a peak of almost 6% in March to 1.3% in June. The erosion of consumer confidence contrasts with strengthening of confidence in the business community. (See the commentary by Carol Stone on July 3rd, reporting on the June Tankan Survey.)

In spite of the recent trend, sentiment among Japanese consumers has improved over the period of the survey. The biggest improvement is seen in consumers' attitude toward employment prospects. The index for this component has risen to 51.7 in June, 2000 from 45.6 in June, 2004. The other components--Overall Livelihood and Income Growth have shown more moderate gains but the Willingness to Buy component, while slightly above June 2004, is at 48.8, almost a full point below the 49.7 of June 2005.

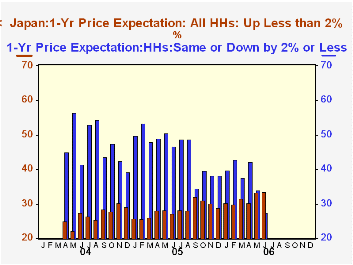

Price expectations of consumers in all Households in June show substantial increases in the numbers expecting prices to rise. 23.5% expect prices to rise between 2 and 5% in the next year, almost double the percent that expected such increases in June, 2004. Current price expectations are shown in the following table compared with those for June 2005 and 2004. As an indication of the shift in consumers' concern from one of deflation to one of inflation, we show, in the second chard, the decline in the percent of consumers expecting prices to stay the same or decline by two percent with the rise of those consumers expecting price to rise by less than two percent.

| Japan: Consumer Confidence: Two Person Households |

Jun 06 | Jun 05 | Jun 04 |

|---|---|---|---|

| Confidence Index | 47.2 | 46.6 | 44.9 |

| Overall Livelihood | 44.8 | 45.0 | 43.6 |

| Income Growth | 43.3 | 43.2 | 41.9 |

| Employment | 51.7 | 48.3 | 45.6 |

| Willingness to Buy Durable Goods | 48.8 | 49.7 | 48.3 |

| Price Expectations: All Households | |||

| No Change | 24.1 | 40.3 | 35.7 |

| Up by Less than 2% | 33.5 | 27.3 | 27.4 |

| Up between 2 and 5% | 23.7 | 12.2 | 17.8 |

| Down between 2 and 5% | 1.0 | 1.3 | 1.5 |

| Down by less than 2% | 3.4 | 6.5 | 5.7 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief