Global| Nov 07 2017

Global| Nov 07 2017Setback for German IP But Trends Are Sill Solid

Summary

Despite growing optimism about European growth and the prospects for the ECB to continue its easing scale back, output growth in Germany fell in September and has dropped in three of the last four months. This period of weakness was [...]

Despite growing optimism about European growth and the prospects for the ECB to continue its easing scale back, output growth in Germany fell in September and has dropped in three of the last four months. This period of weakness was preceded by a string of five straight gains which itself was preceded by a long patch of more or less alternating drops and gains monthly. The message here is to transcend the monthly ups and downs and focus on the trends.

Despite growing optimism about European growth and the prospects for the ECB to continue its easing scale back, output growth in Germany fell in September and has dropped in three of the last four months. This period of weakness was preceded by a string of five straight gains which itself was preceded by a long patch of more or less alternating drops and gains monthly. The message here is to transcend the monthly ups and downs and focus on the trends.

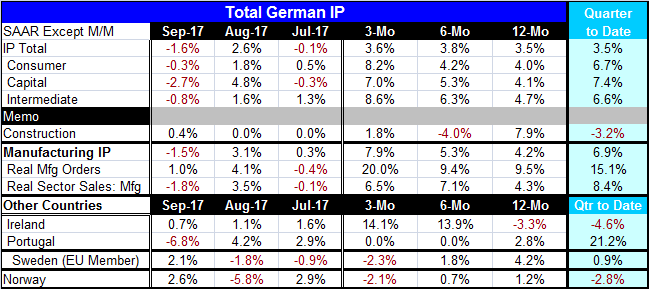

The chart makes it clear that the monthly ups and downs are mostly noise. And since late-2016, all three principle sectors have been expanding regularly. The table makes the added observation that the shorter sequential growth rates from 12-month to six-month to three-month also tell a tale of consistent growth. Over these horizons, total output growth in Germany is hovering in a band between 3.5% and 4%, a narrow and solidly strong habitat for a (real) IP growth rate. Manufacturing output has been mildly and more persistently accelerating in each sector over those horizons. Manufacturing output overall has ramped up from 4.2% to 5.3% to 7.9% from 12-month to six-month to three-month. Construction output has held back the gain in overall output as it falls over six months and gains at less than a 2% pace over three months. But construction output has a strong year-on-year rise.

On this same set of timelines from 12-month progressing through three-month, manufacturing orders have accelerated and manufacturing sales have been quite steady. On balance, the German manufacturing sector appears to be on solid footing; the monthly patterns of decline are best set aside and looked at instead as a part of the broader developing trends.

In the German orders report released yesterday, we saw that German real orders rose by 1% in September boosted by exceptional orders from other EMU member countries. We see entries for the IP results of Ireland and Portugal as well as from Sweden and Norway in the table below. There are monthly output increases for three of these early IP reporters with Portugal the notable exception, but Portugal's large drop in September is on the heels of even more substantial gains over the previous two months. Sequentially, however, these reporters are not on the same page as Germany. Only Ireland has strong and accelerating output trends from 12-month to six-month to three-month. Portugal has output up over 12 months then it is simply flat. Both Sweden and Norway show output on a decelerating path. But these are only the early reporters and much of Europe is still unreported for industrial output. The PMI data that have been released, however, suggest that in those countries that report PMI indexes, manufacturing is still doing quite well despite some sporadic slowing in services.

The German IP report is a solid reassuring assessment of German industry trends. Consumer goods, intermediate goods and capital goods output all are on progressively stronger output paths. On top of that, the growth rates for each sector are solid-to-strong and the quarter-to-date performance is also impressive. The gains in IP are solidly supported by order growth which also looks to better times ahead. The other early reporters of IP data do not so much echo the German theme, but these are smaller economies and they will not loom large in the final tallying of EU or EMU output growth. For now they remind us that not every country is on an upswing.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief