Global| Feb 01 2006

Global| Feb 01 2006Russian Growth Moderates in 2005; Inflation Still Up in Double-Digits

Summary

The State Committee of the Russian Federation reported GDP data today for the year 2005. Total GDP expanded 6.4% for the year as a whole. Assuming there are no meaningful revisions to the first three quarters of the year, the year-to- [...]

The State Committee of the Russian Federation reported GDP data today for the year 2005. Total GDP expanded 6.4% for the year as a whole. Assuming there are no meaningful revisions to the first three quarters of the year, the year-to-year growth for Q4 would be 7.0%, the same as for Q3, not seasonally adjusted. [The implied Q4 information is calculated by us, using DLX capabilities in Excel.]

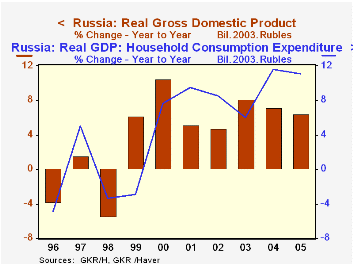

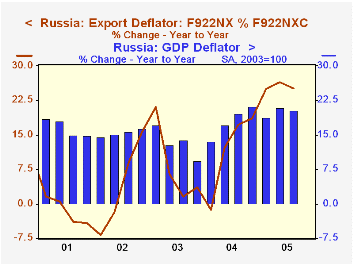

For the year as a whole, growth slowed from 2004 in all major expenditure categories. For most, this downshift was quite modest. Indeed, private consumption remained on a firm growth path after picking up in 2004. In contrast, both exports and imports saw a sizable adjustment. Imports of goods and services had expanded 22.5% in 2004 and moderated to 16.2% in 2005. Exports had been up 11.9% in '04 and then grew only 5.6% last year. A cursory examination of the price deflator for exports suggests that accelerating prices, perhaps for oil, lifted nominal export growth, while export volume gains were much smaller, their weakest since 2001.

Prices in general seem still to be an issue in Russia. Inflation, again perhaps energy related, accelerated sharply in 2004, to nearly 20% from 13.2% in 2003. Last year saw a bit of moderation at a still-high rate. The acceleration is reflected in a price deflator for Russian exports, seen in the second graph. Deflators for consumption and capital formation don't show this significant increase, although they still run at 10-12% rates. Compared with its neighbors, this range of inflation is fairly high. The Ukraine and Kazakhstan experience occasional bouts of double-digit price increases, but most other surrounding industrial countries have much lower rates: Poland, Hungary, the Czech Republic, and so on. Russia continues then to grapple with structural difficulties that, despite its apparently healthy real growth, keep its overall economic performance in a rather precarious state.

| Russia (Bil.2003 Rubles) |

2005 Annual Level | % of Total | Q4 Y/Y Implied Growth | 2005 | 2004 | 2003 | 2005 |

|---|---|---|---|---|---|---|---|

| Total GDP | 15,101 | 100.0 | 7.0 | 6.4 | 7.2 | 8.2 | 4.7 |

| Private Consumption | 8,109 | 53.7 | -- | 11.1 | 11.6 | 6.0 | 8.5 |

| Gov't Consumption | 2,423 | 16.0 | -- | 1.8 | 2.1 | 0.6 | 2.6 |

| Capital Formation | 2,991 | 19.8 | -- | 10.5 | 11.3 | 11.5 | 2.8 |

| Imports | 4,488 | 29.7 | -- | 16.2 | 22.5 | 18.6 | 14.6 |

| Exports | 5,501 | 36.4 | -- | 5.6 | 11.9 | 12.4 | 10.3 |

| Deflator (2003=100) | 143.47 | -- | 25.7 | 19.7 | 19.9 | 13.2 | 15.5 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief