Global| May 04 2017

Global| May 04 2017Retail Sales Continue to Advance in EMU

Summary

Euro area retail sales were soft again in March. Nonfood sales are up by 0.2% and up at a 2% annualized pace over three months, at a 0.4% pace over six months and at a 1.7% pace over 12 months. For an economic area sporting its best [...]

Euro area retail sales were soft again in March. Nonfood sales are up by 0.2% and up at a 2% annualized pace over three months, at a 0.4% pace over six months and at a 1.7% pace over 12 months. For an economic area sporting its best private sector PMI gauge in six years, this is pretty disappointing results.

Euro area retail sales were soft again in March. Nonfood sales are up by 0.2% and up at a 2% annualized pace over three months, at a 0.4% pace over six months and at a 1.7% pace over 12 months. For an economic area sporting its best private sector PMI gauge in six years, this is pretty disappointing results.

In Q1 2017

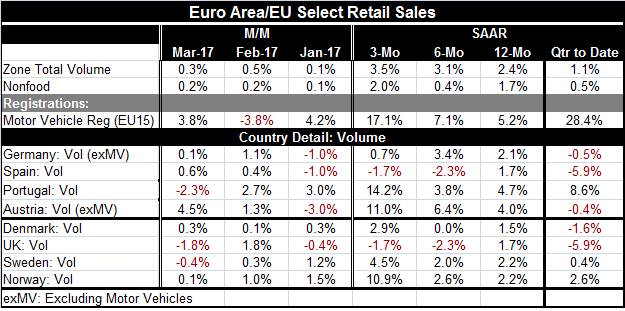

In the just-completed quarter (Q1), EMU area sales rose at a 1.1% pace or at a 0.5% pace excluding food. Motor vehicle sales spurted at an eye-popping 28.4% annualized pace.

Vehicle sales trends

Motor vehicle sales for the overall EU area are much stronger than retail sales, running at a 17.1% annual rate over three months and rising by 5.2% over 12 months as well as showing steady acceleration.

In March and monthly

Looking at European results for a set of eight early sales-reporting countries, only Portugal, the U.K. and Sweden showed sales declines in March. None of these countries showed declines in February and four showed declines in January, three of them sharp declines. However, Germany and Norway logged barebones sales gains in March of just 0.1% month-to-month. And German sales ran cold then hot in January and February.

Sales trends in Europe

The three-month annualized growth figures show double digit sales gains in Portugal and Austria as well as in Norway as of March. There are sales declines in the U.K. and Spain. Germany, the largest EMU economy, gained at an annualized rate of only 0.7%. Over six months, the annualized gains are muted with the strongest gain being Austria at a 6.4% annualized rise. Spain and the U.K. show six-month declines while Denmark is flat over six months. Year-over-year percentage gains show sales advancing across the board, ranging from the strongest gain of 4.7% in Portugal to the weakest rise of 1.5% in Denmark. German sales rise a boring 2.1% over 12 months.

Consistencies

What these calculations reveal is how much Europe is on the same path. The only 'wild differences' are over three months when compounding blows short-term disturbance up larger than life. Over six months and 12 months, the retail sales volume gains are very consistent.

About the region in the quarter

The country level data, which include some EU-only members, some EMU members and one unrelated country, show a solid underpinning to sales gains. Most countries show sales growth over most horizons. Over 12 months no country in this table shows a sales decline. But of course, there is another short-term calculation and that is for the quarter-to-date where the Q1 numbers have just finalized. There we find quarter-to-quarter sales declines in five of the eight countries in the table although the EMU area itself posts a gain in the quarter. On a quarter-to-date basis, the largest declines in sales are drops of nearly 6% (annualized) in Spain and the UK. Denmark (EU) logs a drop at a 1.6% pace. Austria and Germany have declines roughly at a 0.5% pace. Portugal has a strong 8.6% annualized rise as Sweden gains at a 0.4% pace in the quarter and Norway shows a sales gain at a 2.6% annualized rate.

Summing up

On balance, the quarterly and other short-term data show the most unevenness. The pattern of sales, however, is relatively stable over longer periods. As we head into the new quarter, Q2 2017, sales are rising at a 1% to 2% pace. There is no inherited weakness leading into Q2 to hold trends back. However, there is no evidence of the sort of strength that the Markit PMI gauges are pointing to, either. Part of that is that having the best PMI gauge in the last six years is not a very high hurdle. For the PMI gauges to make their mark, they are going to have to climb even higher. Relative strength can be an absolute disappointment.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief