Global| Apr 12 2016

Global| Apr 12 2016Progress on Reducing Price Level Divergence within EMU

Summary

While there is a great deal of focus on what stimulus the ECB can provide or how much a weak euro will stimulate EMU area growth, one factor that should be helping to spur growth in the EMU is the reduction of price level divergence [...]

While there is a great deal of focus on what stimulus the ECB can provide or how much a weak euro will stimulate EMU area growth, one factor that should be helping to spur growth in the EMU is the reduction of price level divergence within the EMU.

While there is a great deal of focus on what stimulus the ECB can provide or how much a weak euro will stimulate EMU area growth, one factor that should be helping to spur growth in the EMU is the reduction of price level divergence within the EMU.

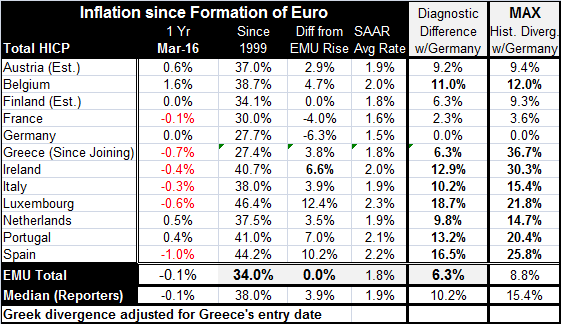

When the EMU was formed, there was some attempt to get the exchange rate levels right for the various domestic prices indicators. Since that day, there has been complete neglect of the country-level price performance since it had no formal standing in policymaking. But that was a mistake. Individual country indices mattered only to the extent that every index fed with a weigh into the EMU index which was the target for the ECB. An overall inflation rate of just under 2% has been the objective for monetary policy since the union was formed. There are no country level inflation objectives. Here we look at the results for the original member states plus Greece. We have estimated monthly results for Belgium and Austria in March to include them.

To provide some baseline, be aware that Germany has the largest weight in the EMU as its largest economy. Since EMU formation, Germany has averaged a 1.5% annual rise in its HICP, a smaller gain than any other member. This `undershooting' of the EMU objective allowed other countries to `overshoot' and for the overall ECB objective still to be met. However, some countries ran persistently higher inflation than Germany. Since all were locked in a single currency zone, they gradually lost competitiveness. This loss caused other economic problems. The far right hand columns track these statistics. At the very far right, we show the maximum bilateral price level difference since the EMU's inception for each country vis-a-vis Germany. In the column just to its left, we show where that divergence stands today.

In all cases, the current divergence with Germany is less than its historic maximum. For some countries like Austria and Belgium, the differences are small. But for other countries, the divergence has been substantially reduced, particularly countries with austerity programs. Greece's divergence has been reduced from 36.7% to 6.3%, a huge amount of progress. For Spain, the maximum divergence of 25.8% has been reduced to 16.5%. For Portugal, a divergence of 20.4% has shrunk to 13.2%. Ireland has improved from a divergence of 30.3% to just 12.9%. These figures refer to how much more each of these nations' HICPs have risen compared to that of Germany since the EMU was formed and exchange rates fixed within the EMU.

For the EMU as a whole, divergence has been reduced from 8.8% to 6.3%. However, that is misleading and understates the degree of progress, since Germany has a very high weight and its divergence with itself will always be zero.

The current German HICP is flat year-over-year in March. At this pace, there are six EMU members that are currently gaining back competitiveness ground once lost to Germany: Spain, Greece, Luxembourg, Ireland, Italy, and France. Finland is holding its place in March. Other countries are back to losing ground again.

The chart at the tops plots German year-over-year inflation vs. that for Spain as an example. The chart shows how through 2008 Spain's inflation ran well above that in Germany. Then the financial crisis hit and German and Spanish inflation both fell and began to track very closely. For the next couple of years, roughly 2010-2012, Spanish inflation grew somewhat faster than German inflation again; then Spanish inflation began to grow more slowing as Spain began to claw back some of its lost competiveness under its austerity program. Even with this progress, Spain's HICP has risen by some 16% more than Germany's since the EMU was formed.

The table shows us that progress is being made and that progress has been made. But also we can see some backsliding. As countries reduce their competiveness disadvantage with Germany, economic growth in those areas should respond more favorably not just because that country can trade on better terms with Germany but that it can do so everywhere in the world. The euro exchanger rate is depressed and countries that have repaired their competiveness situations should also find that they are better able to compete on world markets.

All of this is the good news. The bad news is that these gains have been hard won and are ephemeral. The various economies that have undergone competiveness transformations have also undergone political, social and economic upheaval. And many still bear the scars of that process; despite progress, a great deal of resentment is still harbored against austerity programs. In many places, political parties have gained momentum that want to dismantle austerity.

The key for these countries will be to stay the course. If countries rebel and go back to their budget-busting ways, domestic prices will soar again. And all the pain `invested' in this progress would be for naught. But this is also a lesson about how economics works. And particularly it is a lesson to the countries of Southern Europe that hoped to gain something from this union with strong currency Germany. They hoped to gain lower financing costs and they did. But they did not use the proceeds wisely. They can see that what they have gained-unexpectedly- is the need for discipline far more than they had even when preparing to enter the EMU. Countries came into the EMU with very different momentum for their rates of inflation setting the stage for what happened.

As long as Germany stays on the straight and narrow path (and we know it will always do that), all EMU members will be forced to line up behind it or to suffer the consequences of eroded competiveness. Has the lesson been learned? It is too soon to tell. Some EMU members have experienced pain they will not wish to experience again. But do they understand why? Others continue to run higher inflation rates than Germany. Still, the progress is substantial. But there is a need to do more as well as keep what has been gained. Germany by running fiscal surpluses now is making it even harder for fellow EMU members to keep up. Europe still does not have consensus on how things should be run, but it does have rules that will define what is possible and what the costs and benefits will be of trying to go your own way.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief