Global| Apr 13 2020

Global| Apr 13 2020Portuguese Prices Fall in March; Annually Prices Barely Rise

Summary

Globally the theme is corona, corona, corona. The virus and its progression dominates everything. Economists defer their forecasting to the whims of policymakers led by epidemiologists. But in the end, there remains a steady drumbeat [...]

Globally the theme is corona, corona, corona. The virus and its progression dominates everything. Economists defer their forecasting to the whims of policymakers led by epidemiologists. But in the end, there remains a steady drumbeat of eco-data to be digested, analyzed and put in perspective. Portugal's March CPI and HICP results show tame inflation. Tame inflation trends. And little to worry about on the inflation front... At least that's for now.

Globally the theme is corona, corona, corona. The virus and its progression dominates everything. Economists defer their forecasting to the whims of policymakers led by epidemiologists. But in the end, there remains a steady drumbeat of eco-data to be digested, analyzed and put in perspective. Portugal's March CPI and HICP results show tame inflation. Tame inflation trends. And little to worry about on the inflation front... At least that's for now.

Portuguese inflation trends

Portugal's chart shows inflation ripping up to 4% back in 2011 in the wake of the Great Recession for a period subsequent to one that showed prices falling. Indeed Portugal's prices fell again in 2014 very briefly and since then they have been in a range. But for a few very brief spikes, inflation has kept below the ECBs overarching 2% ceiling. Since end-2010 despite 2011 being an inflation balloon year, inflation in Portugal has run at a compounded annual rate of 1.2% - quite mild.

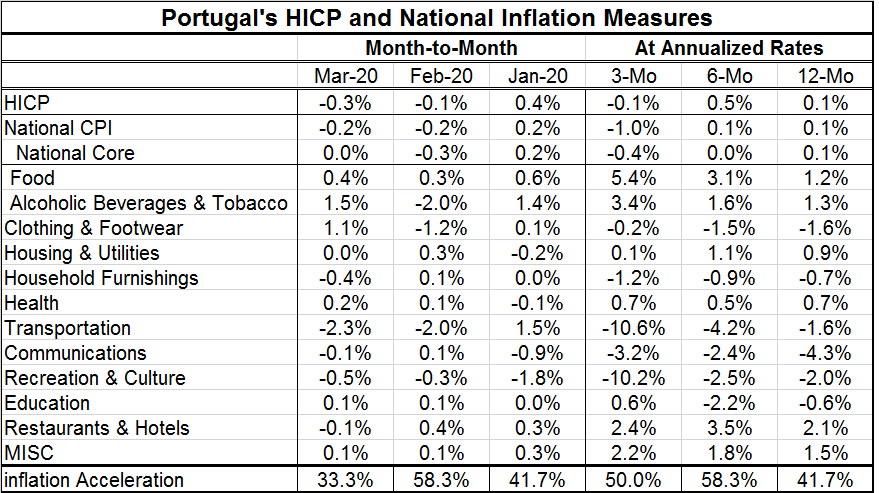

Currently, inflation is 0.1% over 12 months for both the HICP and domestic gauge with the core pace as 0.1% over 12 months as well.

Portugal's success

Portugal is a country once beset with inflation problems that has tamed its inflation beast. The inflation situation globally has settled back as most international reserve currency areas have controlled inflation. Portugal's own trends show inflation as low, steady without acceleration and with widespread trends of moderation. Inflation diffusion gauges are mostly low showing diffusion in the last three months in a range of 33% to 58% or on sequential trends in a range of 41% to 58%. The recent diffusion metrics are low and the one of 12-month inflation diffusion is at 41.7%. The diffusion gauge tells that inflation is decelerating in more categories than it is accelerating. Values below 50% show more deceleration; values above 50 show relatively more acceleration; generally diffusion is above 60% when inflation is on the move.

Eco weakness implies weak prices

Globally central banks and government programs are trying to stave off the effects of economic weakness that are the result of actions taken to stem the spread of the coronavirus. And in the wake of this weakness, prices have been tame in part because oil prices have collapsed. The oil story is one of a two-way problem: weak and falling demand coupled with the deadly sin of excess supply. Over the weekend, OPEC, the Saudis and Russia struck an agreement for sharp reductions in output. But markets are not reacting to it much because demand remains so weak. Even deep output cuts are having a hard time reassuring markets that oil prices can and will firm. That, of course, keeps inflation and inflation expectations low.

Two-pronged inflation risk

Inflation is caught in all of this on a strange two-way street. The Fed and the ECB face similar challenges. Over the weekend, we heard Fed Vice Chair Richard Clarida emphasize that the Fed has all the firepower it needed to avoid deflation. Meanwhile, in a release last week, U.S. inflation expectations, that are still quite low, had started to rise. So inflation is in this odd place where there are both fears of near-term deflation and concerns that all this stimulus will bring inflation later.

Of course, no country's current inflation report is going to shed much light on this multidimensional issue. But that does not make it less real or less of a concern. If countries do not find a way to support their economies while fighting off the contagion of the coronavirus, they are going to find that concerns about deflation are real. Regardless of reassuring words from central banks or policymakers if economies implode prices fall.

The virus and growth

Beyond that everything we think, or think we know, about the economy is speculative. This is because we do not know about the spread of the virus and there is a risk of a second wave if countries opt out of their restrictive modes too soon and if they do not continue to take other steps to contain contagion as they normalize their economies. There was more news overnight from South Korea that has reported another group of people, who had the virus and had recovered, have it again. This is cause for concern because it raises the question of immunity. If you have the virus once, can it reignite spontaneously? Or, if having had it once doesn't cause the creation of antibodies sufficient to protect a person from a second exposure that would be news, too. (and not good news). Because of this new finding in South Korea and because we are still amassing data on who is most at risk, steps to normalize remain risky. But the costs of keeping lockdowns engaged are substantial too. So far, there has been no attempt to bridge the gap between the two and find an equilibrium position between how long to shut down and when to start up. Epidemiologists Rule! And so far, the death rate among the infected is still contained around 1% to 1.3% with the old and persons with certain preexisting conditions most at risk – and other at a very, very, low risk of death. It is possible to flip the switch on growth and still protect at-risk groups. It just does not seem that anyone anywhere has done it. Public policy so far is a blunt instrument of restricting nearly everybody (except essential workers) or nobody. It seems to me that that will have to change.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief