Global| Apr 18 2016

Global| Apr 18 2016Portuguese PPI Prices Show Some Sharp Weakness

Summary

Inflation reports continue to be weak globally. Markets don't really focus on the PPI reports as much especially because they tend to be so dominated by commodities prices which have been so weak. But monetary authorities are looking [...]

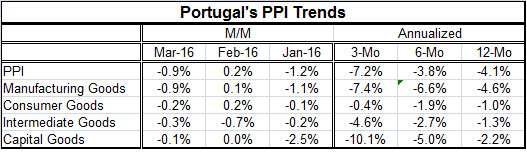

Inflation reports continue to be weak globally. Markets don't really focus on the PPI reports as much especially because they tend to be so dominated by commodities prices which have been so weak. But monetary authorities are looking at everything these days. Portugal may not be a bellwether inflation barometer for the EMU, but maybe its performance is more interesting when its inflation is extra-low instead of extra-high. And that is the case in March. The headline PPI fell by 0.9% in March with manufactured goods prices down by 0.9% on declines in intermediate, consumer and capital goods prices. The three-month rate of change drop stepped up to -7.2% annualized. And the Portuguese PPI is deep into deflation on all horizons for all sectors. That much seems to be a pretty clear signal.

Inflation reports continue to be weak globally. Markets don't really focus on the PPI reports as much especially because they tend to be so dominated by commodities prices which have been so weak. But monetary authorities are looking at everything these days. Portugal may not be a bellwether inflation barometer for the EMU, but maybe its performance is more interesting when its inflation is extra-low instead of extra-high. And that is the case in March. The headline PPI fell by 0.9% in March with manufactured goods prices down by 0.9% on declines in intermediate, consumer and capital goods prices. The three-month rate of change drop stepped up to -7.2% annualized. And the Portuguese PPI is deep into deflation on all horizons for all sectors. That much seems to be a pretty clear signal.

Weakness in unexpected places

As oil prices have stabilized, this is not the expected result and that is what makes the case of Portugal's PPI interesting. In fact, Portugal's inflation is decelerating (deflation is accelerating) on all horizons from 12-month to six-month and from six-month to three-month for all categories of goods except consumer goods. Leading the way lower is a collapse in capital goods prices which are now falling at a 10.1% annual rate. Capital good prices should not be leading the way lower. That is an eye-opener.

Another reduced outlook

Also on Monday, the Bundesbank announced that it expected a slowing in German growth. The Bundesbank is concerned about weaker new orders and overall business expectations for the period ahead. The German economy has been driven by solid consumer attitudes and relied uncharacteristically on consumer spending. Now even with the euro so weak, German exports are slowing and the Bundesbank is cutting its outlook.

Brouhaha over Doha

Over the weekend, the Doha greater-OPEC meeting frayed at the edges and unraveled. Markets have been poised to bump oil prices up on a deal, but there was no deal. And the facts that we knew before the meeting that stood in opposition to a deal eventually scuppered it. Iran was never going to be a part of an output restriction deal and the Saudis prevaricated but were not ready to impose their own freeze and leave Iran out. In any event, there were no members who mattered ready to put any meaningful freeze on the table. With that in mind, we could be poised to see another leg down in oil prices and further negative impact on energy prices and on through to the consumer prices that central bankers target.

The energy price conundrum

Low energy prices are having an impact on the higher cost producers in the U.S. There have been company-level shut downs with knock-on effects for banks. But their estimated costs of production seem to hover around $40/barrel, implying that the oil prices does not really have much upside before supply would expand again. Bankruptcy of oil producers would probably lead to others acquiring their assets and lowering further the breakeven production cost for the acquirer. On the demand side, there is still no revival. As of last week, a number of institutions including the IMF were still cutting their outlooks; today we have the Bundesbank so engaged. Demand can hardly be said to be stabilizing.

The outlook prevarication

On balance, the outlook for inflation has to remain guarded and weak. The ECB, the Bank of Japan and the Federal Reserve all are trying to boost inflation and they appear to still face headwinds. While oil has bounced from its lowest levels then hit a flat spot, it is no longer clear that the flat spot will not become soft again. In the U.S., the Fed has even initiated a tightening sequence that has quickly had to put on hold. The policy environment and outlook is as confusing as it has been for some time. The recent extreme price weakness in Portugal is only one symptom. But when capital goods prices are unraveling and leading the way lower, there is good reason to wonder what is really going on with the inflation process overall. Stability is not the first thing that comes to mind.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief