Global| Nov 11 2020

Global| Nov 11 2020Portugal's Inflation Remains Controlled and Low Which Is More Than You Can Say for Its Encounter with the Virus

Summary

Portugal's inflation rates in October show continued temperance. The year-on-year HICP is lower by 0.6% compared to a 0.1% decline for both the national CPI and the national CPI core measure. Inflation momentum shows the HICP measure [...]

Portugal's inflation rates in October show continued temperance. The year-on-year HICP is lower by 0.6% compared to a 0.1% decline for both the national CPI and the national CPI core measure.

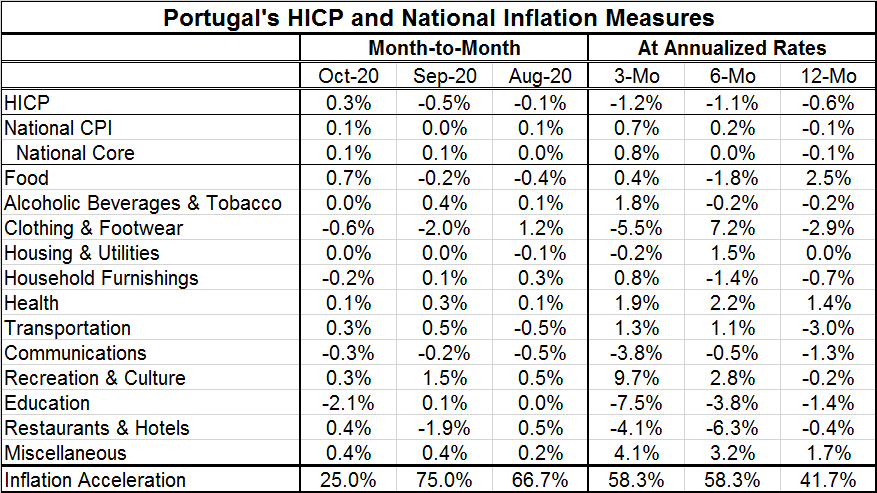

Portugal's inflation rates in October show continued temperance. The year-on-year HICP is lower by 0.6% compared to a 0.1% decline for both the national CPI and the national CPI core measure.

Inflation momentum shows the HICP measure getting progressively weaker for 12-months to six-months to three-months. In contrast, both the national CPI and the national core CPI show an upward progression on that same timeline. However, all inflation gradients are relatively flat.

The last several months also show some differences in inflation according to the HICP vs. the national CPI. In October, the HICP is up by 0.3%, but it was also down even more sharply in September and it fell in August. In contrast, the national headline and core indexes have been waffling around being unchanged month-to-month or rising by 0.1% month-to-month. The HICP has been much more volatile than the domestic measures.

The proportion of national index categories in which inflation rose month-to-month fell to 25% in October from 75% in September and 66.7% in August. However, the proportion of categories with inflation accelerating from 12-months to six-months to three-months shows some tendency to acceleration as the year-on-year proportion is 41.7%, below the 58.3% mark over both six-months and three-months. At 58% more than half of the categories are showing acceleration and that is what we see happening in the aggregate national index price trends over those periods.

However, all of that is hairsplitting for a situation in which inflation clearly is under control. Growth in Europe has been weaker as the virus spreads and that is a factor too. Slow growth and a spreading infection weigh on oil prices which more naturally drive inflation lower.

Impact of the virus

Portugal's virus infection is rising sharply (Source here). There were 187,237 cases as of November 10. However, new cases fell to 3,817 on November 10, down sharply from its spike to 7,497 cases reached on November 4. The total number of active cases and total deaths also are rising. The turn lower for infections is still a very new development and it is hard to say if it marks a trend and a true turning point yet. Deaths are 62 on November 10 were only one death per day off their peak reached on the previous day, November 9. Portugal has imposed a curfew to deal with the spreading virus. About 70% of its population (about 7 million people) has been urged to stay at home on weeknights from 11 PM to 5 AM. The curfew will limit them even more on weekends. These curfews are projected to be in effect for two weeks- but the government has said they will last longer if needed.

Portugal is another European case in which officials will be watching the developments and waiting. The high frequency daily data hint at a turn lower in results, but it is too soon to tell. These measures to ‘stop the spread' will weaken growth to some extent. Portugal is facing a situation that finds a lot of company across the rest of Europe where the spread also has accelerated is advanced and has, in many cases, surpassed the first wave faced earlier in the year. There seems to be a small and negative impact on inflation so far. The impact on growth is yet to play out and to be determined.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief