Global| Oct 21 2005

Global| Oct 21 2005Petroleum Prices Down, And Going Lower?

by:Tom Moeller

|in:Economy in Brief

Summary

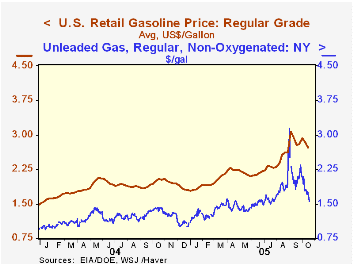

As of last week the US average retail gasoline price fell to $2.73 per gallon, down 11.2% from the weekly high of $3.07 seen in early September. Moreover, yesterday's NY harbor spot price for regular unleaded gasoline was down twenty [...]

As of last week the US average retail gasoline price fell to $2.73 per gallon, down 11.2% from the weekly high of $3.07 seen in early September. Moreover, yesterday's NY harbor spot price for regular unleaded gasoline was down twenty cents to $1.55 from the week previous, the lowest since July, and the seven day average price was off 21.6% from its high.

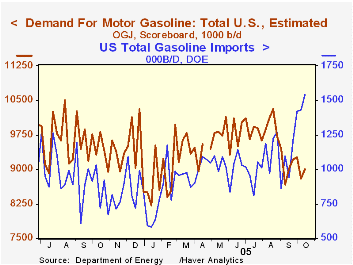

Father Guido Sarducci's axiom that in economics, all that matters is supply and demand is behind the recent price declines. US gasoline supplies have soared due to the surge in gasoline imports which have more than doubled versus last year. That has supplanted a shortfall in production which was limited by a sharp recovery last week to roughly -2% y/y. Demand, on the other hand, has responded to the higher prices and is down sharply, by roughly 8% versus the year ago level.

Lower prices for crude oil have allowed for the gasoline price decline as WTI crude fell yesterday to $61.04 per barrel. That was off 13% from the late August high of $69.82.

The decline in wholesale natural gas prices has been limited versus the petroleum price declines. At $13.09/mmbtu yesterday and $13.42 last week, gas prices were off 13% from the daily high $15.00 one month ago, but trend prices remained elevated ahead of the Winter heating season.

Are Inflation Expectations Rising from the Ashes? from the Federal Reserve Bank of St. Louis can be found here.

For the latest Short Term Energy Outlook from the US Department of Energy click here.

| Energy Prices | 10/17/05 | 12/31/04 | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| US Retail Gasoline, Regular ($/Gal.) | $2.73 | $1.79 | 33.9% | $1.85 | $1.56 | $1.35 |

| Natural Gas, Henry Hub, LA ($/mmbtu) | $13.42 | $6.35 | 139.6% | $5.89 | $5.47 | $3.35 |

| Domestic Spot Market Price: West Texas Intermediate ($/Barrel) | $63.21 | $41.78 | 18.6% | $41.78 | $32.78 | $31.23 |

by Carol Stone October 21, 2005

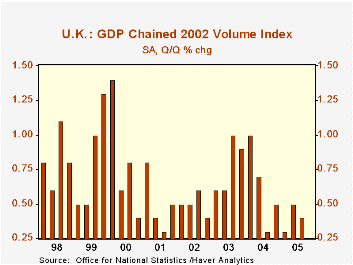

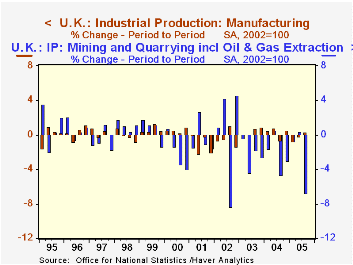

UK GDP grew 0.4% in Q3, according to Office of National Statistics "Preliminary Estimate", following 0.5% in Q2. This early estimate is compiled from industrial production and other industry data. It shows that manufacturing gained 0.3% on the quarter, after Q2's 0.2% decrease. Services maintained their 0.6% quarterly pace for a third straight time. Mining, including oil and gas extraction, and utility output, both of which had been supports in Q2, fell by significant amounts in Q3, 6.7% and 1.8%, respectively.

The upturn in manufacturing was generated by a number of largely unrelated sectors. Wood products, petroleum output and electrical and optical equipment, for examples, all turned up after Q2 declines. Nonmetallic minerals stabilized after a steep decline and rubber and plastics have been virtually flat for about six months. Food and textiles fell in Q3 after rising in Q2. Thus, it's hard to characterize the performance of manufacturing as a whole and therefore to look for any sustaining force -- one direction or the other.

Another sign of precariousness in these UK data comes from a look at the revisions for Q2 compared with its "preliminary" estimate. Three months ago, when we wrote about the Q2 preliminary report, we noted the support from the mining sector, but also that recent irregular downtrends there suggested that the 1.4% gain reported then might be transitory. Indeed. The growth there has now been revised to just 0.4% and the sector resumed a long-term contraction in this latest quarter. This change shouldn't be much of a surprise in this industry. But the broad manufacturing sector also seems to be subject to transitory forces. Already seen above to have a scattered performance reported so far for Q3, the sector experienced a notable revision of Q2 data. As seen in the table below, the "preliminary" Q2 report showed a 0.7% decline, which now has been recalculated at just 0.2%. This is a favorable revision, of course, but at the same time, it points out the skittishness in these data. The analysts at the UK Office of National Statistics include a warning in their press release about the preliminary GDP data, expressing their concern that users put too much store in the preliminary figures. Our examination here describes a couple of good reasons we might agree with that sentiment and suggests that caution is needed as business planners and investors apply them to decision-making and actions.

| United Kingdom: | Q3 2005 "Prel" | Q2 2005Year/Year | 2004 | 2003 | 2002 | ||

|---|---|---|---|---|---|---|---|

| Latest | "Prel" | ||||||

| GDP | 0.4 | 0.5 | 0.4 | 1.6 | 3.2 | 2.5 | 2.0 |

| Manufacturing | 0.3 | -0.2 | -0.7 | -0.1 | 1.9 | 0.1 | -3.1 |

| Mining inc Oil Extraction | -6.8 | 0.4 | 1.4 | -9.9 | -8.0 | -5.2 | -0.3 |

| Electricity, Gas & Water Supply | -1.8 | 1.0 | 1.1 | -2.8 | 2.2 | 1.1 | -0.4 |

| Services | 0.6 | 0.6 | 0.6 | 2.2 | 3.7 | 2.7 | 2.7 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief