Global| Nov 01 2013

Global| Nov 01 2013Peripheral Countries Are Still Lagging: Will That Continue?

Summary

Global growth has been and remained weak. The US has had consistent growth, but it has also fallen short of historic markers. Political developments make the future less certain. The US recently has attacked the `German model' of [...]

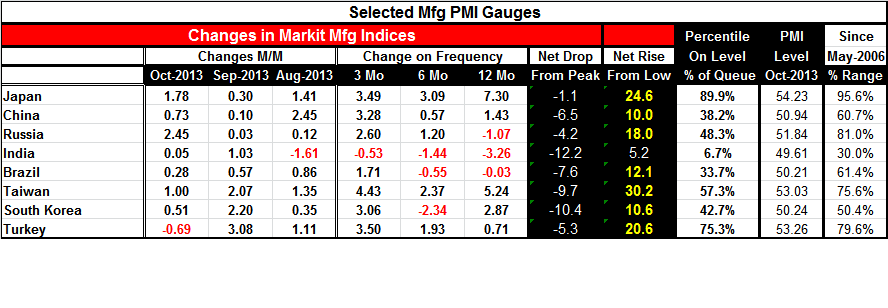

Global growth has been and remained weak. The US has had consistent growth, but it has also fallen short of historic markers. Political developments make the future less certain. The US recently has attacked the `German model' of growth, which is to rely on export-led growth and to maintain a current account surplus. Most of the countries in the table above have relied on export-led growth and may be in for the same sorts of pressures from the US in the future. But if the US doesn't do it, someone else should. There is a great deal of reform needed to the underpinnings of our global trading system

Global growth has been and remained weak. The US has had consistent growth, but it has also fallen short of historic markers. Political developments make the future less certain. The US recently has attacked the `German model' of growth, which is to rely on export-led growth and to maintain a current account surplus. Most of the countries in the table above have relied on export-led growth and may be in for the same sorts of pressures from the US in the future. But if the US doesn't do it, someone else should. There is a great deal of reform needed to the underpinnings of our global trading system

The most highly developed countries in the world, roughly the G-10 countries, have relied too much on debt to drive their growth. Now it all has started to unravel. The modern export-led growth model that was developed in Japan to tap this growth, pursued by the Asian `dragons' and then taken to an extreme by China, has run to its logical conclusion.

That program of export-led growth was never part of a sustained global growth model. Japan moved to the fore using export growth and a low savings rate to build a series of huge trade surpluses while building its foreign exchange reserves as its private financial firms also amassed dollar assets. After some point Japan's penetration of the US market became so great that `orderly marketing agreements' were used to slow the flow of Japanese automobile exports to the US. Japan began to erect factories in the US. A severely rising yen, the impact of the Tsunami and Japan's grappling with a transition away from nuclear power have greatly transformed the Japanese economy from its former export juggernaut days.

Except for China, the rest of the Asian exporters were smaller and did not raise the political backlash that Japan did. But the heavy debt load in the Western countries is beginning to slow demand and their growth rate of imports (exports to them). This, of course, has negative repercussions for nations that use the export-led growth strategy.

China was the game changer, the Baby Huey, who wanted the same thing as `the other kids' but whose size made that impossible. When China launched its own export-led growth drive, it sucked up all the air in the room. Output that had come from other developing economies often migrated to China where costs were even cheaper. China `learned' from Japan's experience and refused to let its currency rise. This allowed China to keep its low-cost advantage longer than it should have. China's international capital flows from its own surplus excesses helped to create the environment for the eventual financial collapse that occurred.

On balance we find the countries that have pursued export-led growth strategies as floundering. Some, like Brazil, blame the US. It blamed the US for the bad effects of QE and for planning to taper and the market effects that the expected taper spawned. This episode is a good example of why world growth needs to be balanced and whey trade needs to occur in a sustainable program. Countries need to take responsibility for their own growth.

Economics does not draw out clear rules on trade and current account balances. Conservatives may hold that a balance international position and domestic fiscal position is best. That is a safe policy but it may not be the best one.

There is time when some nations should run surpluses and others should run deficits .For obvious reasons Saudi Arabia runs and will continue to run surpluses. Its situation is unusual. China cannot claim Saudi Arabia as a precedent. When countries at a high stage of development without any `clear need' to tap foreign savings are doing so and doing it year after year (as the US has done), there should be some questioning of that. Trade must eventually balance. It need not ever balance bilaterally. And in those two statements you can see room for a world of disagreement. When China was in its heyday it was growing fast and running large trade surpluses. Why was a county, in such need of development, running such large surpluses on its current account, accumulating financial assets instead of spending those resources on development? Why did China's consumption as percentage of GDP fall by so much? What kind of development was that?

It was exploitive. And this is the kind of development that is not only unsustainable but, instead, sure to help to contribute to the next meltdown because it is part of a disequilibrium process.

When we look at the progress of the formerly high growth developing economies, we see angst directed at others, as in the case of Brazil. We see China is trying to shift its focus to develop its own internal demand. China was not prepared for this. It stubbornly refused entreaties to let its currency rise and to go the route of normal development. China's path came to a sudden dead end instead of to a managed change in course because of its intransigence and inability to see how unsustainable its policies were. But economics were telling us that every day.

As this growth cycle plays out there are many unanswered questions that all nations need to have answered.

First and foremost is this: Can we have free trade organizations -dedicated to free trade- if the rules of free trade are not ever met? Economists extoll the virtues of free trade, of comparative advantage and yet in the real world these concepts remain elusive. The benefits of comparative advantage are fleshed out in the framework of barter. But in the real world trade uses money (monies). To bridge that gap we need financial reforms. Free trade and comparative advantage principles do NOT play out in a world where currencies are misaligned especially not one where they are consistently misaligned. Following free-trade principles in a non-free trade environment leads to trouble

While trade flows are not a perfect judgment of whether trade is truly `free,' looking a trade flows and at reserve accumulation and at accumulated trade balances we can get a good idea of whose currency is breaking the rules.

We have many issues to deal with in the wake of the financial crisis. Developing nations that have long exploited demand by using a weak currency as a tool may feel deprived of an `old friend.' But if there is no exchange rate reform, we will simply be revisiting financial meltdowns again and again.

So as we watch this period of development play out, let's also watch what happens to trade and current account imbalances. If they are not becalmed, then we are simply on another road to our next BIG THING. And it won't be something good.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief