Global| Sep 24 2008

Global| Sep 24 2008OFHEO House Price Index Continued Moving Lower

by:Tom Moeller

|in:Economy in Brief

Summary

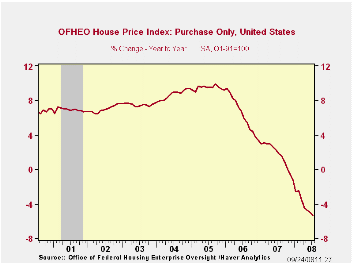

The index of U.S. house prices from the Office of Federal Housing Enterprise Oversight (OFHEO) continued moving lower in July. The 0.6% m/m decline from June followed a revised 0.3% dip during that month which was revised from the [...]

The index of U.S. house prices from the Office of Federal Housing Enterprise Oversight (OFHEO) continued moving lower in July. The 0.6% m/m decline from June followed a revised 0.3% dip during that month which was revised from the initial report of no change in prices.

The 5.3% year-to-year decline is by far the sharpest for this cycle and on record. Negative y/y comparisons began last November.

The OFHEO price index reflects repeat sales of the same

property. It does not, however, make an adjustment for changes in the

form of additions to or deterioration of that property.

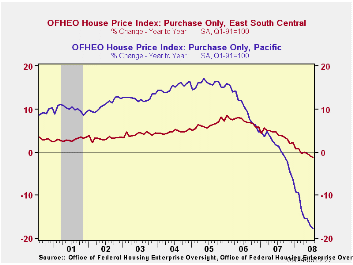

Regional declines in home prices during the latest twelve months were greatest in the Pacific region where prices fell 17.7% y/y. That followed a 0.6% rise last year and several years of double digit gain. Prices also fell a sharp 5.2% in the South Atlantic states, by 4.7% in the Mountain states and by 4.6% in New England.

Elsewhere in the country home prices fell 3.5% in the Middle Atlantic region, by 1.9% in the West North Central region and by 1.2% in the East South central states.

Only in the West South Central of the country did prices rise year-to-year. The 0.6% gain was, however, down from nearly ten years of 3%-to-7% growth.

The latest report from OFHEO can be found here.

OFHEO figures are available in Haver's USECON database.

Another Conundrum? from the Federal Reserve Bank of St. Louis can be found here.

| OFHEO House Price Index (Q1 1991=100,SA) | July | June | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| Purchase Only | 212.0 | 213.4 | -5.3% | 1.6% | 6.3% | 9.5% |

by Tom Moeller September 24, 2008

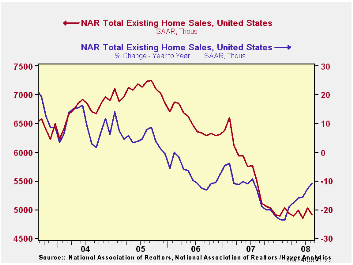

The level of existing homes during August fell 2.2% m/m to 4.910 million. The figure, reported by the National Association of Realtors, followed a 3.5% increase during July which was revised up modestly. The figure about matched Consensus expectations for a selling rate of 4.94M homes. Total sales include sales of condos and co-ops.

Sales of existing single-family homes fell a lesser 1.4% and have moved sideways since last Fall. These sales have a longer history than the total and they were still near their lowest level since early-1998.

By region, home sales in the Northeast reversed all of their July improvement with a 6.6% (-15.0% y/y) decline. Sales out West also fell 5.3% (+4.9% y/y) and reversed the July increase. Working the other way, sales in the Midwest rose 0.9% (-12.3% y/y) and in the South sales also reversed the July downtick and inched up 0.5% (-15.1% y/y).

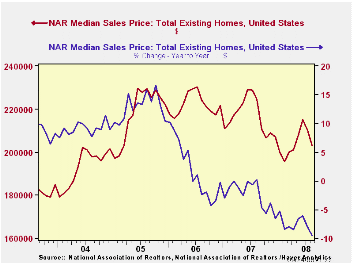

Median home prices fell 3.4% last month

after a downwardly revised 2.2% drop during July.

The number of unsold homes (condos & single-family) on the market fell 7.0% from July (-2.9% y/y). At the current sales rate the inventory fell slightly to a 10.4 months supply which is near the record high for this series. For single-family homes, however, the inventory fell a bit more to a 10.0 months supply at the current sales rate. That was down from an 11.0 months supply in June.

Why Do Chinese Households Save So Much? from the Federal Reserve Bank of St. Louis is available here.

| Existing Home Sales (Thous) | August | y/y % | July | August '07 | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|---|

| Total | 4,910 | -10.7 | 5,020 | 5,500 | 5,672 | 6,508 | 7,076 |

| Northeast | 850 | -15.0 | 910 | 1,000 | 1,008 | 1,090 | 1,168 |

| Midwest | 1,140 | -12.3 | 1,130 | 1,300 | 1,331 | 1,491 | 1,589 |

| South | 1,860 | -15.1 | 1,850 | 2,190 | 2,240 | 2,576 | 2,704 |

| West | 1,070 | 4.9 | 1,130 | 1,020 | 1,093 | 1,353 | 1,617 |

| Single-Family | 4,350 | -9.6 | 4,410 | 4,810 | 4,958 | 5,703 | 6,181 |

| Median Price, Total, $ | 203,100 | -9.5 | 210,300 | 224,400 | 216,617 | 222,000 | 218,217 |

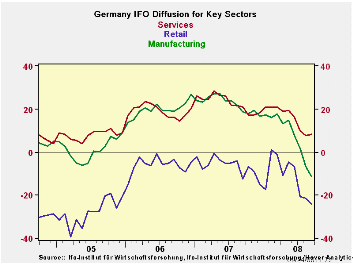

by Robert Brusca September 24, 2008

The IFO sector readings are plunging and the overall indices are weak as well. In September the business expectations index remains in the lower 13 percentile of its range. The current situation is mid range at the 51st percentile. But sector readings are deteriorating with manufacturing, wholesaling and retailing falling especially sharply in just the past few months.

Moreover, all of euro is beginning to show this same sort of malaise. Yesterday the Bank of Belgium index fell from 5.9 in August to14.4 in September. Italian business confidence released today registered its lowest reading in seven years. French business confidence, another morning release, fell to its lowest mark in over five years.

The German IFO reading is only the lowest in three years. But this year’s low in expectations sub index is the lowest since 1993. With the recent surge in oil prices and mini jump in the euro Europe has a lot on its plate to worry about. If Europe escapes recession it will be nothing short of a miracle.

| Summary of IFO Sector Diffusion readings: CLIMATE | ||||||||

|---|---|---|---|---|---|---|---|---|

| CLIMATE Sum | Current | Last Mo | Since Jan 1991* | |||||

| Sep-08 | Aug-08 | Average | Median | Max | Min | Range | % range | |

| All Sectors | -14.8 | -11.1 | -6.6 | -9.8 | 16.8 | -26.3 | 43.1 | 26.7% |

| MFG | -11.6 | -6.8 | 3.5 | 3.8 | 27.2 | -22.6 | 49.8 | 22.1% |

| Construction | -25.2 | -26.4 | -32.8 | -38.8 | -7.9 | -50.5 | 42.6 | 59.4% |

| Wholesale | -10.3 | -5.5 | -9.9 | -14.5 | 23.5 | -39.4 | 62.9 | 46.3% |

| Retail | -24.0 | -21.5 | -20.3 | -20.5 | 1.2 | -39.6 | 40.8 | 38.2% |

| Services | 8.3 | 7.7 | 10.7 | 9.5 | 28.5 | -15.7 | 44.2 | 54.3% |

| * May 2001 for Services | ||||||||

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief