Global| Dec 08 2016

Global| Dec 08 2016OECD LEIs Tick Ever So Slightly Higher as the OECD Trumpets Gaining Momentum

Summary

The OECD itself reports the following analytical assessment of its release this month: * Signs of growth gaining momentum have emerged in the CLIs for the United States, Canada, Germany, and France. In the United Kingdom, there are [...]

The OECD itself reports the following analytical assessment of its release this month:

The OECD itself reports the following analytical assessment of its release this month:

* Signs of growth gaining momentum have emerged in the CLIs for the United States, Canada, Germany, and France. In the United Kingdom, there are also signs of improvement in the short term, although uncertainty persists about the nature of the agreement the U.K. will eventually conclude with the EU.

* Growth is expected to gain momentum in China and India, in particular, and also in Brazil and Russia, albeit from low levels.

* In the OECD area as a whole, Japan, and the euro area as a whole, the CLIs point to stable growth momentum.

* In Italy, the CLI show signs of easing growth.

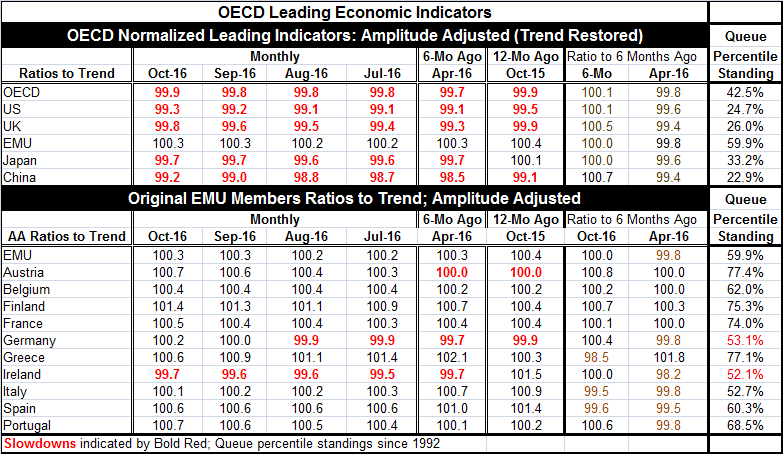

The OECD seems to be sipping some thin gruel to find improvement in these data. In the past, it has referred to looking at the change in its indices over six months to see the best (most reliable) signal. For that purpose, the table we present looks at the ratio in the CLIs to their value of six months ago, and in turn, at the six month ago reading to six months previous to that to create a linked 12-month look at momentum.

Here is what I find...

* The OECD LEIs are below 100 for all countries/groups in the top panel of the table except for the EMU. That result alone points to below average performance for growth.

* The ratios of the current index to six months ago show improvement for China, the U.K., the U.S., and for the OECD area as a whole. The ratios for the EMU and Japan are unchanged.

* Six months previous to that all countries/areas were showing worsening ratios to their six month before indices. So the lack of deterioration is another measure of 'progress' but not one that is very robust.

* Looking at CLI values back to 1992, only the EMU has a reading that is above its historic median on that timeline. The U.S. the U.K. and China have readings clustering at or near the bottom 25th percentile of their values on that period -hardly cause for celebration. Japan's standing is in the bottom one-third of its queue of CLI values while the EMU is in its 60th percentile, ten percentile points above its median. It is the relative strongest reading of the lot- hardly impressive. For all of the OECD, the CLI standing is in the 42nd percentile of its historic queue of CLI values, below its median reading since 1992.

* Within the EMU, Austria, Finland, Portugal, Belgium, and France show momentum higher now than six months ago (higher ratio). But Greece, Italy and Spain are weakening and for the latter two the weakening follows a weakening over the previous six months as well. The problems playing out in Italian politics are reflected in ongoing economic deterioration and in worse prospects; even the OECD is forced to admit it. Ireland presents raw CLI readings consistently below 100 but also shows an unchanged ratio to six months ago- implying weaker than average performance that will persist but is not worsening.

On balance, the OECD CLI indicators can be construed to be showing some improvement or gain in momentum as the OECD has chosen to do, but when placed of a scale of truth the real story is how meager and nascent this improvement is and that weak the growth continues to be in train. In the case of the U.S., the CLI has ticked up by a net of 0.2 points in the course of two months after being stuck at a reading of 99.1. The ratio of the current U.S. CLI to its value of six months ago is higher by just 0.1 and that is a very sour note on which to hang a song of improvement.

The OECD is a membership organization. I very much get the impression that members are trying to put the best spin possible on the interpretation of these readings. I do not find the OECD report encouraging in the least and find the 'improvements' posted this month as in the range of normal variation and unconvincing as yet as to the ongoing nature of improvement.

The ECB policy shift (hint: it's a taper)

What is perhaps the most disturbing aspect about the OECD's own interpretation is that it can serve as a guide for policy and potentially as an independent third party's view. And today we have the ECB cutting back on its former level of monthly stimulus although it is extending the period for such bond purchasing stimulus farther into the future than had been expected. I believe most people in markets find the monthly total as more of the measure of support than the period for which purchases are planned (and can be changed, as we see today). To the markets, this looks like a tapering and markets are responding in that fashion today with bond yields higher, stocks lower and the euro's foreign currency value higher. These are classic less-stimulus responses by markets.

Downshifting while stalling?

I certainly hope that the ECB has not taken any of the recent data including the fresh OECD LEIs to heart as evidence of improved or more solid economic performance. The OECD gauges for the EMU as whole find, on the OECD's interpretation, a showing of 'stable momentum.' That is not technically wrong, but it is still a weak trend and without an improvement in momentum and that is with a good deal of monetary stimulus that has been both in train and in effect. What happens when that monetary stimulus is cut back? This is the problem when one hand is on the stimulus switch and the other operating the forecast mechanism. The right hand has to know and account for what the left hand is doing. Is it? This is a hypothetical question, but if momentum is only stable and you remove or reduce a source of stimulus, shouldn't conditions get weaker? Isn't that how you see it?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief