Global| Feb 08 2016

Global| Feb 08 2016OECD LEI Slips But Is Called 'Stable' in December

Summary

The OECD has refused to panic over some ongoing erosion in its LEI series (called composite leading indicators or CLIs). Its LEI series for the OECD as a whole is construed as stable even as the series languishes below 100 and has [...]

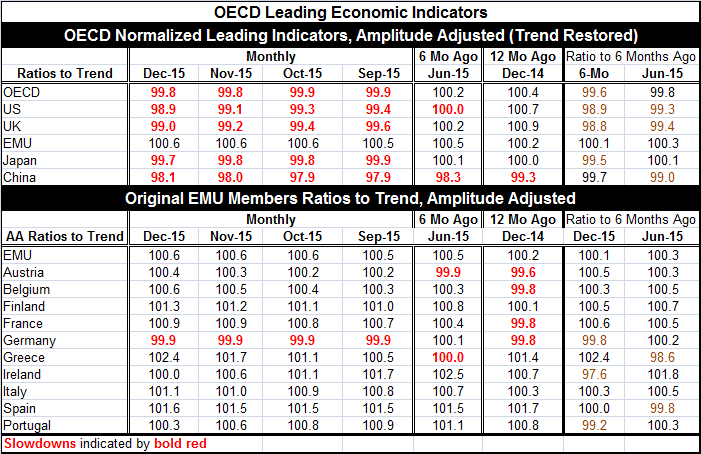

The OECD has refused to panic over some ongoing erosion in its LEI series (called composite leading indicators or CLIs). Its LEI series for the OECD as a whole is construed as stable even as the series languishes below 100 and has fallen in two of the last three months before halting its slide in December. The U.S. series is looking more uneven with drops in each of the last 15 months and a current level standing at 98.9. Looking at the levels of the LEI, the U.S. level has been lower only 18% of the time since January 1993. The U.S. has the weakest level standing on this horizon among all developed countries save the U.K. which has a 10th percentile standing. The OECD assesses the U.K. and U.S. as having growth in an easing mode with similar weak trends emerging in Canada and Japan. Japan has just adopted a program of negative interest rates which was approved on a decidedly split (six to five) vote at the Bank of Japan.

The OECD has refused to panic over some ongoing erosion in its LEI series (called composite leading indicators or CLIs). Its LEI series for the OECD as a whole is construed as stable even as the series languishes below 100 and has fallen in two of the last three months before halting its slide in December. The U.S. series is looking more uneven with drops in each of the last 15 months and a current level standing at 98.9. Looking at the levels of the LEI, the U.S. level has been lower only 18% of the time since January 1993. The U.S. has the weakest level standing on this horizon among all developed countries save the U.K. which has a 10th percentile standing. The OECD assesses the U.K. and U.S. as having growth in an easing mode with similar weak trends emerging in Canada and Japan. Japan has just adopted a program of negative interest rates which was approved on a decidedly split (six to five) vote at the Bank of Japan.

So while there is some view that the U.S. economy is being battered by forces from abroad but that it will be able to pull through, the fact is that the U.S. economy is being battered even harder by forces from within. And while some characterize the situation as being an international slowdown, clearly it is global since the U.S. slowdown already is in train; moreover, its slowing is among the fastest. Stanley Fischer's point that the U.S. has weathered past international events is a nonstarter as an observation since this one is global and already is taking a toll on the U.S. economy which has its own domestic problems at any rate. The Fed ought not to try to sluff off the challenges of the U.S. economy as coming only or even mainly from abroad.

The OECD indices show that four of the five main countries/areas in the table, four stand below their respective levels of 100. That is an indicator of slippage. The OECD overall index also is below 100 at 99.8 in December. The EMU is the exception with a December value above its six-month-ago level and is the only country/region to be able to say that. These observations leave us with the impression that there is still a great deal of weakness afoot. And while EMU is so far escaping the emission of weak signals on the OECD data tableau, it continues to have other indicators that have logged less than stellar performance.

When we look inside the EMU at its earliest members plus Greece, we find only Germany with readings below 100 and these have been stuck at 99.9 for a series of months. Only three countries Germany, Ireland and Portugal are net weaker over six months. According to the LEI approach, the EMU is stabilizing and not withering. The EMU reading, at a level of 100.6, stands in the 70th percentile of its historic queue of data. All EMU members in the table are above their 50% percentile except Germany. Portugal stands only in its 52nd percentile followed by Ireland in its 59th percentile with all the rest showing observations in their 60th percentile region or higher.

The OECD said that both China and Brazil are stabilizing this month. China's reading, however, is still slipping and is the weakest among the other four industrialized economies in the top of the table.

The OECD readings are up-to-date only through December. In real time, it is nearly mid-February. Markets are continuing to melt down. Europe's Sentix index, released today, fell sharply to its lowest point since mid-2015. Germany's Ifo has been weak. A slew of Markit PMIs have been weak for both services (where available) and manufacturing. The loss of wealth due to market declines is palpable China's stock market loses are dizzying and its second consecutive near $100 billion one month drop in official reserves as of December is chilling news.

Ironically, indicators like the OECD that have names like `leading index' unfortunately are by their nature constructed of data that lag in real time and are not fully up-to-date. Still, it is always interesting to assess the data we have in hand to see what they tell us. And one message from the OECD is that things are still stable. Another is that while things are construed as stable, there is still minor erosion afoot. Whichever way of looking at these indices that your prefer, the data over the next several months appear to have worsened so the LEI signals look like they are preparing to deteriorate too. In that vein, Europe will do so from a relatively firmer base while the U.S. will do so from a relatively weaker base. In real time, China and Brazil may not really be stabilizing at all.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief