Global| Nov 12 2013

Global| Nov 12 2013OECD Leading Indicators Confirm Strength in Euro-periphery

Summary

The OECD leading economic indicators are a good short hand way to assess trends across various economies. The chart on the left shows that the US expansion seems to have steadied. Europe's momentum is strong as its indicator is moving [...]

The OECD leading economic indicators are a good short hand way to assess trends across various economies. The chart on the left shows that the US expansion seems to have steadied. Europe's momentum is strong as its indicator is moving up with vigor. China's indicator is weakening; its economy is still losing momentum.

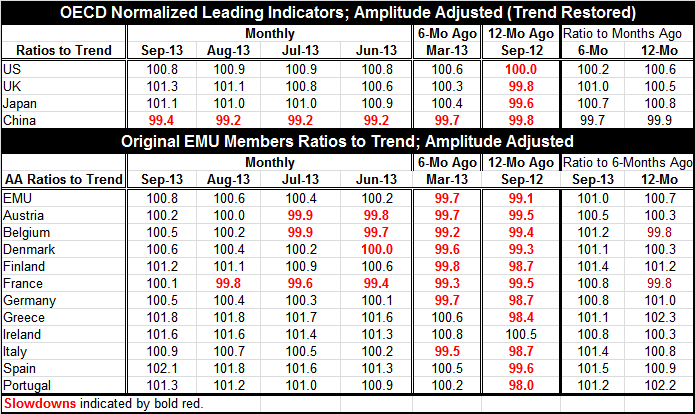

The OECD leading economic indicators are a good short hand way to assess trends across various economies. The chart on the left shows that the US expansion seems to have steadied. Europe's momentum is strong as its indicator is moving up with vigor. China's indicator is weakening; its economy is still losing momentum.

In Europe where the upswing has the most vigor, it is the peripheral economies that had been doing so badly that have turned higher with the most strength. The strongest indicator rankings in September are from Spain, Greece, Ireland and Portugal.

Germany ranks ninth among the eleven EMU members in the table. France ranks last. Italy ranks only in the middle of that pack at sixth. The large EMU economies are not leading the upswing. Nor are their indicators all that strong.

The OECD LEIs show that 12 months ago only Ireland had positive momentum. Six months ago four countries had positive momentum; Greece, Ireland, Spain and Portugal. By June of this year, only four nations had negative momentum: Austria, Belgium, Denmark and France. As of September all the eleven EMU nations in the table are showing positive momentum.

While the vigor in the periphery of the eurozone is good news, it will not be able to last without continued growth in the eurozone core. In our report of yesterday, we showed that Greece's improvement has stimulated its imports but that its exports had begun to lag. A widening trade gap in the peripheral economies of EMU could spell a hasty end to suddenly improved economic growth.

One of the things that has helped to make downward adjustments in the peripheral current account deficits was the sharp slowdown in domestic demand that severely slowed imports. But stronger growth will suck those imports back in. And growth in the periphery that is stronger than in the core of EMU will expand current account deficits in the periphery nations. That does not seem to be a prescription for continued growth. Yet many are very happy with the recent surge in peripheral growth. One thing should be clear is that the eurozone needs to be about balance, and that the scope for strong growth in the periphery unaccompanied by strong growth in the core will be quite limited.

It is important for the largest eurozone economies to grow and to give fellow EMU members a chance to exploit the domestic demand in the large core nations. While that may seem like a good idea, Germany, the largest economy in the EMU, simply does not work that way. That's why I see this pattern of growth in EMU as not such a good thing. Europe continues to have problems with policy coordination even as it shows signs of improved growth.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief