Global| Feb 09 2021

Global| Feb 09 2021OECD Leading Indicators Advance

Summary

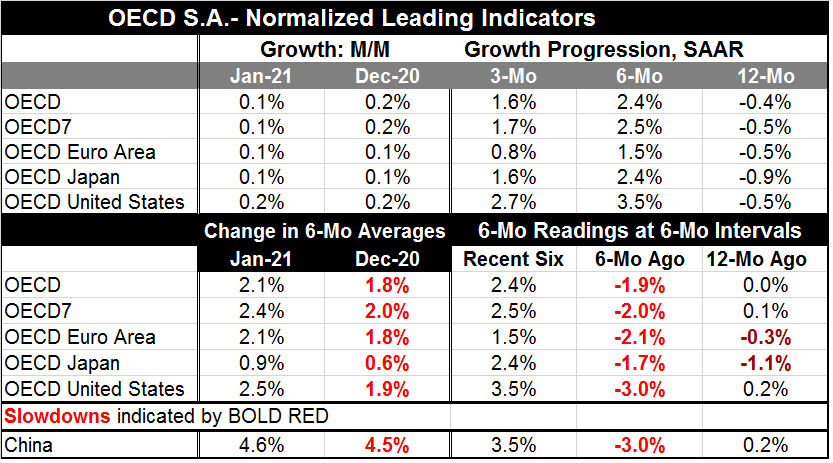

The OECD leading indicators rose by a 'tick' to 99.7 in January from 99.6 in December. November was 99.4; October was 99.3. Clearly the strengthening trend continues, but it is a very mild and possibly fragile trend. The pace of [...]

The OECD leading indicators rose by a 'tick' to 99.7 in January from 99.6 in December. November was 99.4; October was 99.3. Clearly the strengthening trend continues, but it is a very mild and possibly fragile trend.

The OECD leading indicators rose by a 'tick' to 99.7 in January from 99.6 in December. November was 99.4; October was 99.3. Clearly the strengthening trend continues, but it is a very mild and possibly fragile trend.

The pace of expansion

The sequential growth rates (three-month to six-month to 12-month) show no clear ongoing trend. For all countries and regions (OECD, OECD7 and euro area), there is a decline over 12 months and increase over six months, then another increase over three months but an increase that decelerates compared to six-months. So the expansion process continues, but it does not continue apace.

The vaccine

The pace is deteriorating and that is happening as globally the virus is still spreading and as several new more difficult – and perhaps vaccine resistant- strains of the virus have emerged. The U.K. strain spreads faster and is about 30% more lethal while the South African strains was just deemed to have made the AstraZeneca vaccine ineffective against it; that vaccine rollout in South Africa has stopped as a result.

Vaccine backtracking?

There are huge implications for growth and for LEI readings if vaccine rollouts are going to slow, become impaired, or if the virus is able to outwit vaccines sending the labs repeatedly back to rework their formulae.

The LEIs: growth and momentum

Viewed in terms of change in averages the six-month change in the six-month average for the LEI in January does accelerate broadly in all countries and regions. This is a horizon preferred by the OECD. However, the margin of acceleration on this smoothed basis is very thin – except in the U.S. where the acceleration is better than one half of one percentage point. Comparing change in six-month levels (rather than changes of six-month averages) also produces an acceleration over six months that is across the board. But the six-month ago readings are themselves negative. And the six-month changes of 12-months ago are mixed and small. Clearly the signal from these LEIs is that progress is continuing, but the progressions are nascent and are not yet gathering much momentum.

A more detailed assessment

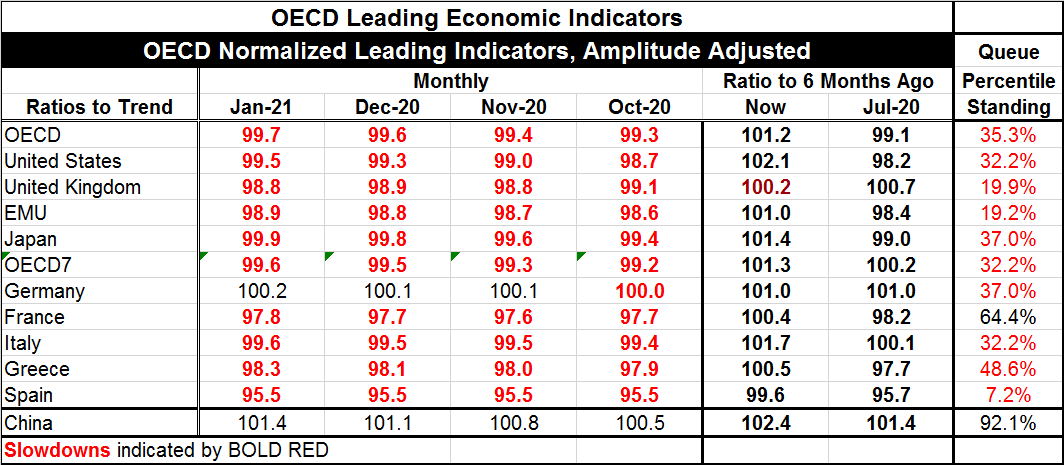

Applied to a broader sample of countries and looking at the index levels, we see most LEI indexes are below 100 indicating subpar growth. Germany and China are the only exceptions. The ratios of LEI values to six months ago finds broad improvement for this set of countries/regions with only one reporter weaker over six months compared to the previous six months (U.K.).

Percentile standings of the LEIs

However, the percentile standings of the LEI values are weak across the board with China as the only exception on a 92nd percentile standing and with France at a moderate 64th percentile standing. All other readings are below rankings of 50% which puts them all below their historic medians. The OECD ranking is in its 35th percentile, a near bottom one-third standing for the areas as a whole.

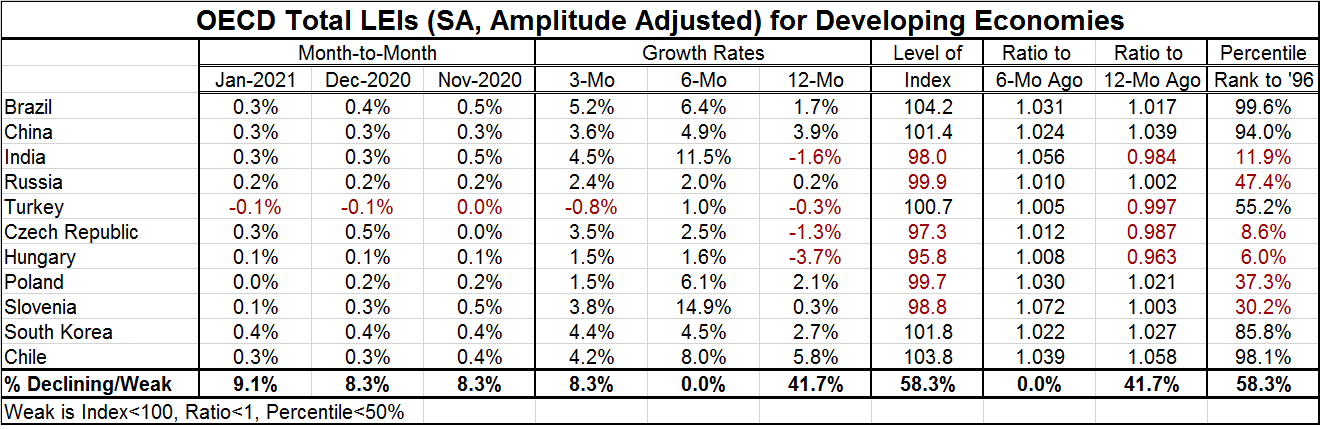

We can repeat these comparisons for a set of developing economies as well; we include China in both groups for comparison.

Note: the month-to-month LEI changes as well as three-month growth and six-month growth are positive on a widespread basis; fewer than 10% of their reporters show declines on any of those horizons. Over 12 months, 47% of reporters register a decline. That is a reminder that the ongoing recovery in the developing world also is relatively nascent. Current index levels are below 100, a sign of weaker than normal growth, in 58% of the reporters. The ratio to six-months ago finds improvements in all members in this table. Turkey and Russia show the smallest margins of improvement; Slovenia and India show the largest margins of improvement. However, the current LEI as a ratio to 12-months ago still is weaker in four counties: India, Turkey Czech Republic, and Hungary.

The percentile standings show more above median standings than for the developed country group. Brazil, Chile, China and South Korea all log strong standings when ranked on data back to 1996. Turkey has an above median standing at its 55th percentile. Russia is short of its median (below 50%) as are Poland, Slovenia, India, the Czech Republic, and Hungary.

On balance, the OECD indexes communicate several states of being rather clearly.

• That globally performance is weak

• That momentum is still positive

• That while positive, momentum is weak

• That the recovery is still nascent and is not picking up momentum and may be fragile.

When we take these statements about the condition of the global economy and marry them to what we know is reality we can see a problem since the virus is still there and still spreading but being fought using the various vaccines. The vaccine process is also still in its infancy, but it is progressing and the U.S. vaccinations are outdistancing new infections. That's progress. But there are also questions? To make real progress, the extent of vaccination will have to broaden and combine with the number of past Covid-19 cases to create a herd immunity effect that will slow the pace of the spread while vaccinations can continue and really begin to tip the process in favor of stopping the spread altogether. For now the OECD LEIs tells us that globally growth is still taking it on the chin, making progress, but progress that is slow and looks oh-so fragile.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief