Global| Dec 02 2014

Global| Dec 02 2014No Relief for ECB from PPI; No Relief for PPI from ECB

Summary

Euro-Warfare: The EMU PPI is down by 1.4% year-over-year. Yet all the stories out of Europe are about the European Central Bank and whether it can launch a quantitative easing program or whether that will be blocked. And while the [...]

Euro-Warfare: The EMU PPI is down by 1.4% year-over-year. Yet all the stories out of Europe are about the European Central Bank and whether it can launch a quantitative easing program or whether that will be blocked. And while the issue of which remedy the ECB may be able to launch is important, there is nothing more important than what is happening: the condition that policy will have to treat. With oil prices plunging and the OPEC in disarray, inflation has taken on the greater prospect of downside risk, adding it to an already palpable legacy of target misses. This risk comes at a time when the ECB's HICP has run below its target cap for 71 straight months, and has been below 1.5% for the last 20 consecutive months. The year-over-year HICP has been continuously below 2% with the exception of four months for the last 140 months (11.7years)!

Euro-Warfare: The EMU PPI is down by 1.4% year-over-year. Yet all the stories out of Europe are about the European Central Bank and whether it can launch a quantitative easing program or whether that will be blocked. And while the issue of which remedy the ECB may be able to launch is important, there is nothing more important than what is happening: the condition that policy will have to treat. With oil prices plunging and the OPEC in disarray, inflation has taken on the greater prospect of downside risk, adding it to an already palpable legacy of target misses. This risk comes at a time when the ECB's HICP has run below its target cap for 71 straight months, and has been below 1.5% for the last 20 consecutive months. The year-over-year HICP has been continuously below 2% with the exception of four months for the last 140 months (11.7years)!

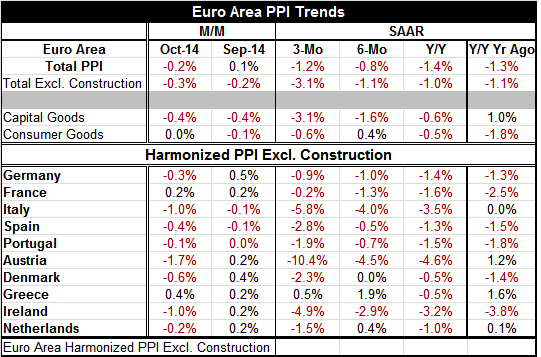

Docile PPI: The PPI has long been tranquil and its core (excluding food, energy, alcohol and tobacco) has been below 1% for eight straight months. The year-over-year headline PPI has been falling for 15 months in a row and has been below 1% for 20 months in a row.

There can be no doubt that EMU inflation is tamed, but is it too docile?

The Policy Conundrum: Should the ECB, especially with the new threat of even weaker inflation from falling oil prices, take further steps to boost inflation back toward its target or will the stimulus from weak oil prices be enough, even with its `perverse' effect which will cause an even bigger short-term inflation miss (undershoot) to occur?

The Link to the HICP and Signal: The EMU-wide PPI is plotted in the chart above along with the HICP. While the statistical correlation between these two series is only 0.046, a very small correlation, the chart makes it clear that the PPI is in fact an important harbinger of changes in the speed of the HICP. The PPI is more volatile than the HICP, a fact that reduces its correlation with the HICP, but does not prevent it from sending out reliable signals on changes in trend. Its signal right now is that this trend of declining prices is going to continue.

The Dilemma: So if YOU were seated on the board at the ECB and if YOU had this incredible legacy of inflation target misses, how would YOU respond? Of course, the relevant question is, "How will THEY respond?", but a bit of game playing may also be useful. The Germans, Austrians and the Dutch are single-minded about monetary policy and do not seem to have been moved by the repeated misses of the inflation target on the downside. Southern European economics that have been put through the wringer on austerity and have elevated rates of unemployment want the ECB to play the agreed rules: boost inflation back to target. But since the ECB is faced with the same `zero bound' problem as the Fed (and the BOJ) what can it do? It might do QE but that is not in its charter. So what does greater damage to the ECB's credibility, missing its target for so long or amending its operating rules for a very special circumstance?

The ECB's 800-Pound Invisible Gorilla: This question is the 800-pound gorilla in the room that no one is really asking. The German Axis is holding the ECB's feet to the fire on its limited mandate-PERIOD! Southern Europe wants relief and thinks it can legitimately pursue additional policy measures because of the ECB's failure to perform on its inflation mandate. Both sides have a point, but never the twain shall meet.

Europe's Mobius Strip: Europe is stuck in an endless Mobius strip. This strip seems to have only on side and only one edge; it seems to defy the rules of geometry, but it is not only very real but easy to construct. This strip personifies the circumstance of the argument over the ECB. Each side has a point but it is all part of the same argument of what the ECB should do and why. No one is asking the question of which course of action will be best or which worse for the future and the credibility of the ECB! That should be the point and should bring the two sides together.

A Simple Counterfactual: However, the German Axis wants to stick to the language and rules governing the ECB's allowed ACTIONS even though these rules are preventing the ECB from defending its credibility and reaching its agreed goal on inflation. And the inflation miss is now long and severely under target. Perhaps the German side could understand the dilemma better if we instead posited inflation over its target (instead of under) by as much for as long. What if the HICP had been for 11.6 years above 2% and was currently running at 3.7% (the `mirror image' pace on the upside to 0.3%)? Posit that, then ask them how that would make them feel about policy. Of course, they would conclude that policy should tighten and should have tightened long ago and they would add that nothing stands in the way of a tightening. They also (probably) would add that such a situation could never occur in the euro area. On the high-side, there is no zero bound. But is that grounds for ignoring it on the low-side and tolerating such a miss? The German side could understand this better couched in those terms. But the final question is simply this: What is more important? Is it preserving the strictures on the ECB actions or the ECB having the credibility of hitting its target?

Does the answer beg the question? If the answer is that it is best for the ECB to keep the restraints on, then what is the point of having targets that can be trumped? This is a defining moment for Europe and for the ECB. People that hate `fiat money' usually hate it because such systems are too flexible and wind up creating inflation. Europe has invented a fiat currency system that has all the flexibility of the gold standard. And I do not mean that as a compliment. Remember for those of you that love the gold standard, one of the reasons we moved to fiat currencies is because the gold standard eventually is unsuitable, rigid, and breaks down. Both the gold standard and the fiat systems have issues. Will the euro-system break down over its inflexibility? Or will falling oil prices, paradoxically, save it?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief