Global| Apr 06 2005

Global| Apr 06 2005Mortgage Applications Near Lowest of the Year

by:Tom Moeller

|in:Economy in Brief

Summary

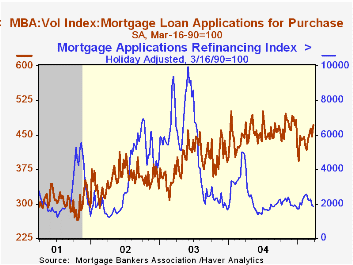

The Mortgage Bankers Association reported that mortgage applications dropped 4.4% last week to the second lowest level of 2005. The decline lowered the opening level for April 6.8% below March which fell 4.8% from February. Purchase [...]

The Mortgage Bankers Association reported that mortgage applications dropped 4.4% last week to the second lowest level of 2005. The decline lowered the opening level for April 6.8% below March which fell 4.8% from February.

Purchase applications dropped 5.3% and reversed all of the prior week's rise to open the month 2.6% below March. During the last ten years there has been a 50% correlation between the y/y change in purchase applications and the change in new plus existing single family home sales.

Applications to refinance fell for the fifth week in the last six. The 3.1% decline lowered the latest level 12.2% below the March average which fell 16.1% versus February.

The effective interest rate on a conventional 30-year mortgage slipped to 6.16% following the prior week's jump to 6.34%. The effective rate on a 15-year mortgage reversed all of the prior week's rise and fell back to 5.81%.

The Mortgage Bankers Association surveys between 20 to 35 of the top lenders in the U.S. housing industry to derive its refinance, purchase and market indexes. The weekly survey accounts for more than 40% of all applications processed each week by mortgage lenders. Visit the Mortgage Bankers Association site here.

What Financing Data Reveal about Dealer Leverage from the Federal Reserve Bank of New York can be found here.

| MBA Mortgage Applications (3/16/90=100) | 04/01/05 | 03/25/05 | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Total Market Index | 644.5 | 674.3 | -36.4% | 735.1 | 1,067.9 | 799.7 |

| Purchase | 446.0 | 470.9 | -6.6% | 454.5 | 395.1 | 354.7 |

| Refinancing | 1,798.8 | 1,857.2 | -56.4% | 2,366.8 | 4,981.8 | 3,388.0 |

by Carol Stone April 6, 2005

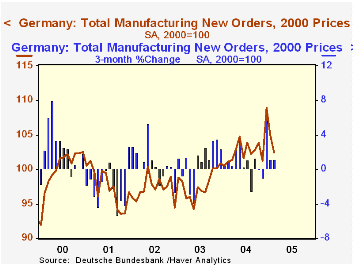

German factory orders declined in February, with domestic and foreign customers both pulling back. This was the second successive monthly decrease, although these followed a widespread jump in December. The Ministry of Economy and Labor reports that total orders were off 2.6% in February, following a 3.5% drop in January and a 7.6% surge in December.

Press reports of these data emphasize the two latest monthly declines, attributing them to higher energy costs and Germany's high level of unemployment. These factors may eventually drag down the German manufacturing sector. But for the time being, reductions in these last two months are probably better seen simply as reactions to the big gain in December. Foreign orders especially are still 4.1% above November's amount.

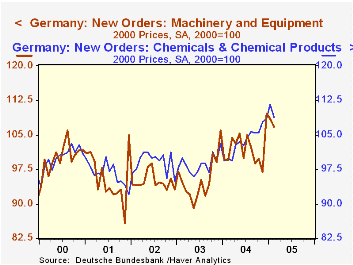

Further, among industries, the key machinery sector is holding that late 2004 level better than most others. Total orders for that group in February were 10.2% above November, with the domestic portion 1.9% higher and foreign 16.8% (simple point-to-point percent changes, not annualized). Foreign orders for machines were actually stronger in January than December so a modest setback in February was hardly noticeable. Some industries are weakening, to be sure, especially metals, nonmetallic minerals, rubber and leather. Flat trends are evident in wood products, electrical equipment orders from domestic customers and "other" manufacturing. Notably, though, chemicals, a sector that often reacts sharply to petroleum prices, has continued a dogged uptrend until a 2.5% decrease in February.

So a clear pattern is not apparent in German manufacturing. Some analysts argue that the persistent gains in the foreign sector will lift all of industry in coming months, actually helping eventually to lower unemployment; this is the opposite chain of events foreseen by others, who suggest that high unemployment will pull down all of the German economy. Stay tuned.

| Germany (% chg, SA) | Feb 2005 | Jan 2005 | Dec 2004 | Year Ago | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|---|

| New Orders | -2.6 | -3.5 | 7.6 | 1.3 | 6.4 | 0.6 | -0.3 |

| Domestic | -2.8 | -6.3 | 8.0 | -2.9 | 4.3 | -0.1 | -3.4 |

| Foreign | -2.3 | -0.4 | 7.0 | 5.9 | 8.9 | 1.5 | 3.5 |

| Sales (includes Mining) | 0.1 | 2.8 | -2.1 | 1.2 | 4.8 | -0.5 | -1.7 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief