Global| Sep 22 2014

Global| Sep 22 2014July Italian Orders Sag

Summary

Both Italian foreign and domestic orders fell in July. Foreign orders have fallen for three consecutive months. Domestic orders have fallen in two of the last three months. The trends in orders are not reassuring either. Italian [...]

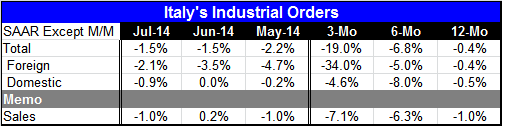

Both Italian foreign and domestic orders fell in July. Foreign orders have fallen for three consecutive months. Domestic orders have fallen in two of the last three months. The trends in orders are not reassuring either.

Both Italian foreign and domestic orders fell in July. Foreign orders have fallen for three consecutive months. Domestic orders have fallen in two of the last three months. The trends in orders are not reassuring either.

Italian headline orders are declining for three straight months; their progressive growth rates show progressively deteriorating orders contraction. Orders are down by 0.4% over 12 months and down at a 6.8% annual rate over six months; they are falling at a 19% annual rate over three months. This is a very disappointing profile.

Foreign orders are down by 0.4% over 12 months and down at a 5% pace over six months. They are falling at a 34% annual rate over three months. This is an even more disturbing pattern of weakness.

While Italy's domestic economy has not been doing well, its order pattern is not as bad as orders from foreign sources. Domestic orders are down 0.5% year-over-year and down at an 8% percent annual rate over six months. Over three months Italian orders are down at just a 4.6% annual rate. That's almost a walk in the park compared to the severe contraction for foreign orders over that same period.

Meanwhile, industrial sales continue to be weak, posting declines at a -7.1% annual rate over three months, a -6.3% annual pace over six months, and a -1% rate over 12 months. Sales are showing the same deteriorating pattern as orders.

Recall that Italy has slipped back into recession for the third time since 2008. Its newest episode of contraction began in the second quarter of 2014. Even so, Italian foreign orders are much weaker than Italian domestic orders.

Compared to the euro area itself, Italian orders are only about same as overall euro area orders which fell by 1.3% in June and fell by 1% in May; their July values are not yet available. While the Italian orders report may be a blow to any that were expecting a sudden rebound, the domestic portion of Italian orders is holding up better than orders in the euro area at large.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief