Global| Mar 23 2018

Global| Mar 23 2018Japan’s CPI Pace Moves Higher As New Risks Emerge

Summary

Japan’s CPI moved higher, rising by 0.1% in February after a 0.4% increase in January. This marks a 12-month string of monthly CPI changes without a month-to-month decline. This is the longest such string for Japan without the CPI [...]

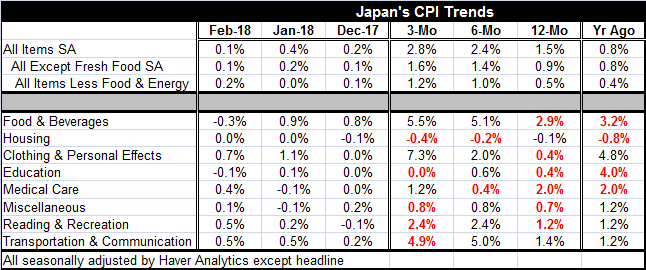

Japan’s CPI moved higher, rising by 0.1% in February after a 0.4% increase in January. This marks a 12-month string of monthly CPI changes without a month-to-month decline. This is the longest such string for Japan without the CPI declining (by a measurable -0.1% or more) month-to-month since at least 2005.

Japan’s CPI moved higher, rising by 0.1% in February after a 0.4% increase in January. This marks a 12-month string of monthly CPI changes without a month-to-month decline. This is the longest such string for Japan without the CPI declining (by a measurable -0.1% or more) month-to-month since at least 2005.

All items except food and energy prices rose 0.2% in February and that series is accelerating from 0.5% to 1.0% to 1.2% from 12-month to six-month to three-month. However, for the BOJ’s closely watched series of all items excluding fresh food and energy, the annual gain in February was just 0.5%, a tick higher than its 0.4% gain in January and represents still-too-weak-to-depend-on momentum.

Large Japanese companies are continuing their policy of implementing wage hikes and that should provide some underpinning for continuing inflation. Moreover, Japan, like the U.S., the U.K. and Germany, has a very low unemployment rate. Japan’s rate is at a 25-year low. But tight labor markets have not automatically punched the ticket to higher wages and inflation.

While Japan’s inflation trend looks favorable and it embodies some of the best news Japan has seen in a while, the recent rise in the yen will be a counteracting force to rising inflation in Japan. Global risks again are shifting.

The new trade wars have put global economic policy into a new stage with new risks. Japan has not or has not yet secured an exception from the Trump tariffs.

Central banks continue to be surprised at the extent of moderation in pricing. Old relationships marking correlations between economic tightness and inflation have been breaking down faster than an old car with high mileage. Will the instigation of a trade war rekindle these dormant relationships by weakening the discipline of global supply chains and by limiting global competition or will it affect inflation directly with import price-hiking tariffs?

Tariffs threaten higher prices in countries that impose them. But tariffs, if retaliated against, militate against the expansion of productivity and against increases in global growth. At a time that growth forecasts have been rising around the world, the tariffs threaten to set back the growth acceleration and they raise new risks for monetary authorities that were poised to shift gears to less accommodative policies. Less accommodation by the world’s major central banks hardly seems like the right path right now.

It is too soon to tell how all this is going to shake out. For starters, markets do not like this and there are no winners, there are only losers and bigger losers. With tariffs imposed on China’s companies producing iron ore, there have seen sharp drops in their share prices. The tariffs are creating knock-on effects, some desired some not so desired.

However the jury is still out on where this is headed.

I think you have to apply the same principals to tariffs that you do to localized warfare. It has been said the U.S. should not launch any military engagement without a clear set of objectives so it can tell when they have been met and when it is time to declare victory and leave. This is one of the lessons of Vietnam. The same may be said to be true of tariffs. The question everyone should be asking is this: what does Trump want? On the face of it, the U.S. has persistently gotten the sort end of the stick on trade. Whatever criticism you can launch at the U.S. for saving too little, or consuming too much, or having the wrong work force skills, and so on, the counterpoint is that the dollar could have fallen to help reduce the U.S. deficit. And that is what was never allowed to happen. Now as part of the fallout from the ‘trade war’ the dollar is falling. That does improve U.S. competiveness. But there are still restrictive and anti-competitive practices that U.S. firms face abroad. What does Mr. Trump need to see to say that the tariffs have been an effective stick to get the behavior modification he has wanted so he can remove them?

I think the wrong way to look at these tariffs is to assume that they are ‘protectionist’ and are meant to stay in place for a long time. I think they are a stick and are meant to bring countries to the negotiating table to offer policy changes and to open doors wider for U.S. firms overseas.

Everyone knows that a tit-for-tat trade war with successive rounds of tariffs imposed does not lead to any place good. I am not necessarily confident that the Trump administration can pull this off without there being damage. It is said to make an omelet you have to break some eggs. But I am confident that they have a plan and that it is not simply to impose tariffs and keep them there.

Japan is one of the countries that has run persistent trade surplus over all. And while Japan has played ball with the U.S. on trade and lived through a series of orderly marketing agreements that restricted auto trade and has invested directly in the U.S. to make autos here thereby limiting exports, it continues to run trade surpluses (much lower however since the tsunami struck and forced Japan to close its nuclear reactors and to import fuels). So Japan remains at risk to these new, more, aggressive Trump tariffs.

For now the BOJ is in the same fix as the ECB, the BOE and the Fed, wondering how much the trade war will spread and how much damage it will do. It is already doing damage to growth and to growth prospects by taking down financial markets. There will be further handicapping of the impact on growth. Needless to say, the Fed’s recent meeting and outlook will have its conclusions substantially altered by these events. Everything is in flux again.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief