Global| Oct 13 2004

Global| Oct 13 2004Japanese Current Account Widens with Service and Income Flows as Well as Trade

Summary

Japan's current account surplus for August, reported today by the Bank of Japan, increased ¥347 million from July in seasonally adjusted terms. This brought it to ¥1.734 billion, the third largest monthly surplus in the almost 20-year [...]

Japan's current account surplus for August, reported today by the Bank of Japan, increased ¥347 million from July in seasonally adjusted terms. This brought it to ¥1.734 billion, the third largest monthly surplus in the almost 20-year history of these data.

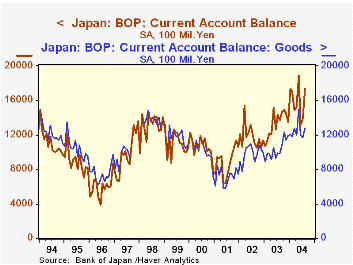

Typically, observers associate the behavior of current account balances directly with trade balances, mostly trade in goods, but sometimes the broader concept of goods and services. In the case of Japan, goods exports run larger than goods imports, creating sizable trade and current account surpluses. As seen in the accompanying graph, for years, the trade surplus was even bigger than the overall current account. During the year 2000, however, this relationship switched around: non-trade international flows have moved from net deficit to net surplus and that surplus is growing.

This new trend highlights the importance of services and incomes as well as trade in a nation's overall balance of payments position. For a nation such as Japan, where investors hold substantial foreign assets, one might attribute the growing non-trade surplus to investment income. While this is generally so, it is also true that Japan's income payments are diminishing, as is evident in the table below; in fact, this trend appears to be on a steadier path than the growth of income receipts. Further, as we think of "services", we most often look to travel and transportation. But in the August data, the biggest increase was in royalties and license fees. That is perhaps less significant because it is unlikely to be repeated consistently. Nonetheless, all of these "intangibles" contribute and can produce sizable swings in the overall current account position from unconventional and therefore probably unexpected sources.

| Billions of Yen | Aug 2004 (Seas Adj.) | Monthly Averages, Not Seasonally Adjusted|||||

|---|---|---|---|---|---|---|

| Last 12 Months | 2003 | 2002 | 2001 | 2000 | ||

| Current Account Balance | 1734 | 1518 | 1314 | 1178 | 888 | 1073 |

| Trade | 1277 | 1208 | 1022 | 978 | 711 | 1047 |

| Memo: Non-Trade Balance | 457 | 310 | 292 | 200 | 177 | 26 |

| Services | -244 | -354 | -325 | -439 | -443 | -428 |

| Credit | 952* | 812 | 749 | 686 | 653 | 622 |

| Debit | 1229* | 1167 | 1075 | 1125 | 1096 | 1050 |

| Income | 775 | 732 | 690 | 689 | 700 | 542 |

| Credit | 1116* | 964 | 922 | 957 | 1043 | 873 |

| Debit | 145* | 232 | 231 | 268 | 343 | 331 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief