Global| Jun 17 2020

Global| Jun 17 2020Japan's Trade Trends Continue to Erode

Summary

Japan was once an international trade juggernaut. It was unstoppable. Its exports flooded worldwide markets and Japan's trade surpluses were large and enduring. But that was then. Japan is still a very important global trader and [...]

Japan was once an international trade juggernaut. It was unstoppable. Its exports flooded worldwide markets and Japan's trade surpluses were large and enduring. But that was then.

Japan was once an international trade juggernaut. It was unstoppable. Its exports flooded worldwide markets and Japan's trade surpluses were large and enduring. But that was then.

Japan is still a very important global trader and exporter. Japanese firms now have operations all around the globe so that not all Japanese products are made in Japan and that has a huge impact on Japan's trade statistics. Japanese firms have large direct investment positions in China, many Japanese name-plate electronic products are made in the Philippines, Toyota produces cars in Thailand as well as other places. Japanese automakers have production facilities in the U.S. as well. The U.S. production platform was designed to reduce the bilateral U.S. deficit with Japan back when that was a hot-button issue.

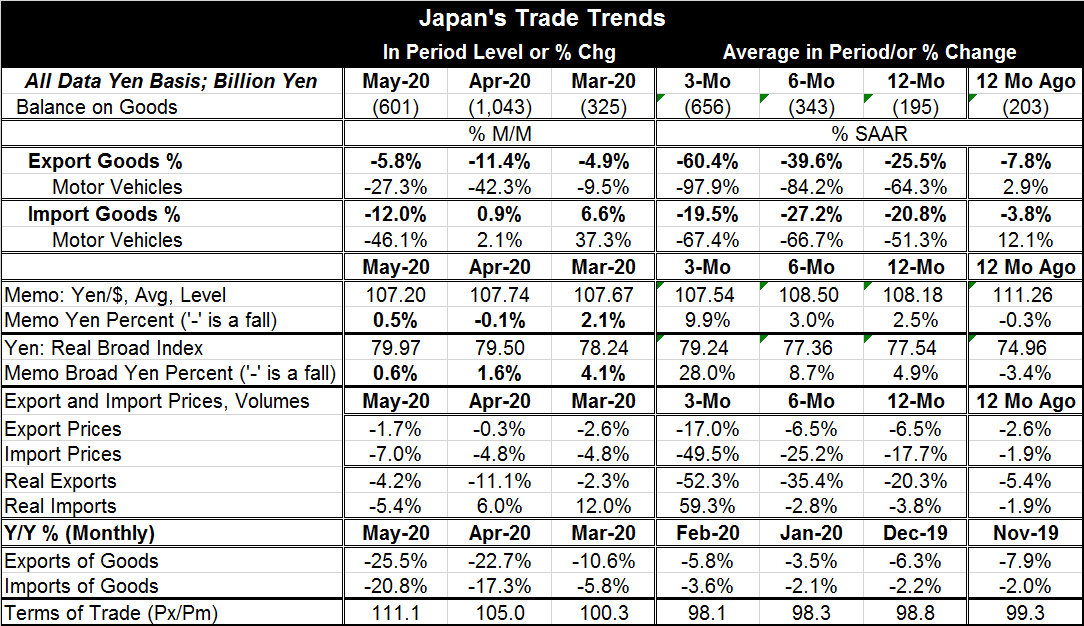

In May, Japan's trade position posted another deficit. Since July 2018, there have been only 3 monthly surpluses recorded. Over 12 months nominal yen-based exports are falling by 25.5% compared to a 20.8% drop for imports. On this timeline, there has been an ongoing disruption of global trade as the U.S. and China have been trading off imposing new tariffs on one-another. Then there was the outbreak of the coronavirus that further slowed global trade flows. Japan's export flows are slowing sequentially from 12-months to six-months to three-months. Both exports and imports are falling on all those horizons.

A good part of the decline in nominal trade flows has been prices weakness. Oil prices have plunged and are still only languishing at weak levels as OPEC has taken steps to stabilize them and to eventually boost them (they hope). Export prices are falling by 6.5% over 12 months and falling at an annualized rate of 17% over three months. Similarly import prices are falling by 17.7% over 12 months and plunging at a 49.5% annual rate over three months.

Those price trend differences for exports and imports translate into very different patterns for export and import trade volumes. Export volumes are decelerating, dropping by 20.3% over 12 months, falling by 35.4% over six months and plunging by 52.3% over three months. Contrarily import volumes are lower by 3.8% over 12 months and falling at an annualized 2.8% over six months; however, over three months import volumes are rising at a 59.3% annual rate.

Monthly Japanese nominal exports are falling year-over-year for 19 consecutive months. On that same basis, imports fall for eight consecutive months but also fall year-on-year in 16 of those 19 consecutive months.

Trade flows have been vastly affected interrupted, reduced and their future has been made uncertain by trade war and by the reaction to the spread of virus. The U.K. and the EU are still hammering out their new trade relations in the wake of Brexit. The U.S. still has some new trade deals to make especially with the U.K. and the EU. The trade picture remains in flux.

The Baltic Dry goods index continues to move higher. The U.S. is showing some powerful new signals of returning to growth after a very short but extremely intense recession related to virus-management. The early strength in U.S. jobs and surprising rebound in retail sales growth as well as in industrial output expansion and the positive signals from the home builder index show that many U.S. sectors are on the mend. The U.S. economy is a long way from being fixed, but there is a substantial pace of recovery in the making. There still is no indicator of how long lasting the recovery will be or how full it will be or if it will remain this powerful for very long. Europe seems less engaged in recovery than the U.S. China is back up in the air.

The Baltic Dry goods index continues to move higher. The U.S. is showing some powerful new signals of returning to growth after a very short but extremely intense recession related to virus-management. The early strength in U.S. jobs and surprising rebound in retail sales growth as well as in industrial output expansion and the positive signals from the home builder index show that many U.S. sectors are on the mend. The U.S. economy is a long way from being fixed, but there is a substantial pace of recovery in the making. There still is no indicator of how long lasting the recovery will be or how full it will be or if it will remain this powerful for very long. Europe seems less engaged in recovery than the U.S. China is back up in the air.

If recovery takes hold, Japan remains competitive and ready to resume its exporting. The yen has risen by about 2.5% vs. the dollar over the past year while the broad yen has risen only by about 5%. The terms of trade (Px/Pm) have turned in Japan's favor over this period, but that has not been so much at a cost of competitiveness as it has been because of a drop in the price of oil. Japan should be well-positioned to benefit from a pick-up in global growth if that is in the cards. So far, the U.S. emits the strongest signals of recovery while Europe shows more signs of bottoming than of growing. China is still struggling especially with a new outbreak of the virus. The global outlook remains foggy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.