Global| Jul 20 2017

Global| Jul 20 2017Japan's Trade Surplus Stays Small

Summary

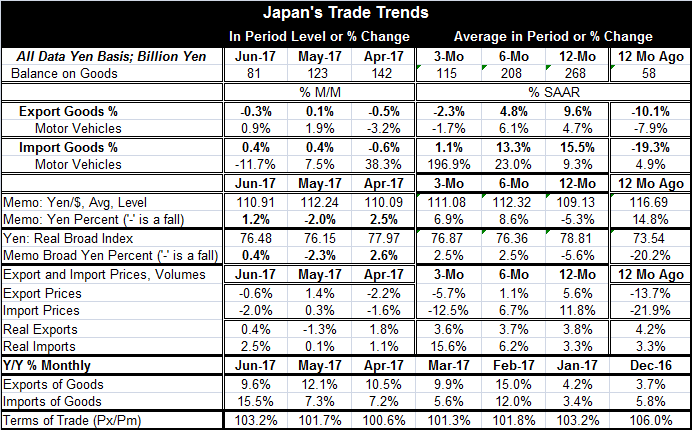

In late 2015, Japan shook off a string of deficits on its trade account and began to post surpluses. The surpluses rose into 2016, but since then they have been unable to build momentum. Aside from one large surplus posted early this [...]

In late 2015, Japan shook off a string of deficits on its trade account and began to post surpluses. The surpluses rose into 2016, but since then they have been unable to build momentum. Aside from one large surplus posted early this year, the surpluses have been contained and are now trending lower.

In late 2015, Japan shook off a string of deficits on its trade account and began to post surpluses. The surpluses rose into 2016, but since then they have been unable to build momentum. Aside from one large surplus posted early this year, the surpluses have been contained and are now trending lower.

Nominal trends

Exports and imports both are showing decelerating trends in yen terms comparing rates of growth from 12-month to six-month to three-month. Exchange rates have not been a major factor. The yen is up by 5.3% over 12 months but recently has been very stable against the dollar. The broad trade-weighted yen has had similar movements.

Real trends

In real terms, the patterns are very differ. Japanese exports in volume terms are growing in a 3.5% to 4% range. In real terms imports are accelerating despite the fact that the imports are decelerating in nominal terms. Real imports are accelerating from about 3% over 12 months to 6% over six months to 15% over three months.

Prices

Obviously the equalizer here is that Japan's export and import prices are both decelerating. That is what 'squares' the real with the nominal data. And price gyration is not principally an exchange rate effect. For imports, oil prices are at work on prices. Despite all this price agitation, Japan's terms of trade are nearly unchanged from January to June. And Japan continues to fight off deflation

Non sequiturs from Japan

Non sequiturs from Japan

Japan's trends tell a somewhat mixed and inconsistent story about growth. Nominal flows are decelerating for both exports and import and that is an ominous note for growth. But in the more important real (inflation adjusted) data, exports have a steady 3.5% sort of growth in gear, and while steady is not really that much help for the overall economy, it is there. Meanwhile, import volumes have been ramping up with the mixed message that (1) domestic demand in Japan is strong and in good shape and (2) that the rise in imports is going to reduce GDP growth which already is at a pace that has not been especially impressive. The behavior of real imports is hard to puzzle out because real imports are so much stronger than they should be given the weakness in Japan's GDP and domestic demand (see the chart for data though Q1). One answer to that observation is simply to not make so much of compounded three-month growth rates. Year-over-year Japan's exports and imports are growing at 3.8% for exports and 3.3% for imports- that's even-handed. Even with the three-month real import speed-up, year-on-year imports are not very impressive at 3.3%.

Asia...ready or not

Asian growth in general has been less than impressive even with China having just hit its Q2 GDP target but doing so on data many find suspicious. China continues to talk of how it has to transform its economy to lean more on the services sector... then it continues not to do it. This Chinese transition has been one of the most widely advertised policy shifts that despite its promotion is not happening. Asia is still stumbling in the wake of the financial crisis. Japan is still trying to shed its deflationary tendencies and its population is shrinking making that job even harder. Japan is not likely to export itself to prosperity either. While the 21st century was supposed to belong to China and Asia, at the 10-year mark it has already run into some major obstacles. And at the 17-year mark, nearly one fifth of the way into its 'century,' it is still stumbling through the obstacle course that was supposed to be its cup of tea.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief