Global| Apr 19 2021

Global| Apr 19 2021Japan's Trade Surplus Reappears

Summary

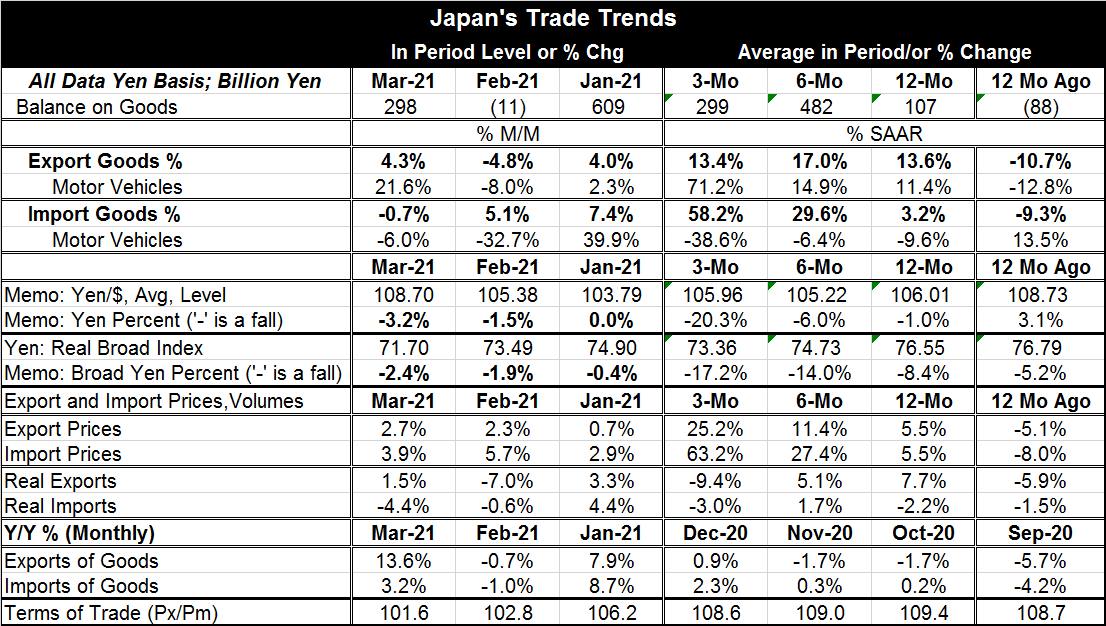

After a dip into deficit in February, Japan's trade balance shifted to surplus in March as exports surged 4.3% and imports receded by 0.7%. Both exports and imports in March reversed their respective changes in February. However, both [...]

After a dip into deficit in February, Japan's trade balance shifted to surplus in March as exports surged 4.3% and imports receded by 0.7%. Both exports and imports in March reversed their respective changes in February. However, both flows had risen strongly in January. The January gains were strong enough to help carry the three-month gains in exports and imports to an annualized rise of 13.4% for exports and a super strong 58.2% annualized gain for imports.

After a dip into deficit in February, Japan's trade balance shifted to surplus in March as exports surged 4.3% and imports receded by 0.7%. Both exports and imports in March reversed their respective changes in February. However, both flows had risen strongly in January. The January gains were strong enough to help carry the three-month gains in exports and imports to an annualized rise of 13.4% for exports and a super strong 58.2% annualized gain for imports.

Looking at sequential growth rates for goods exports, the annualized rates of growth are more or less steady at 13.6% over 12 months, rising to 17% over six months and easing back to a 13.4% pace over three months. Contrarily, import growth builds sequentially accelerating from a gain of 3.2% over 12 months to a six-month pace of 29.6% and a three-month annualized pace of 58.2%.

The sequential values of the dollar yen rate show some exaggerated moves especially over a short period of three months where the growth rate drops at a 20.3% annualized rate. But the smoothed three-month, six-month and 12-month averages of the rate level are quite stable and consistent around the yen 105 to the dollar mark. The broad yen shows a bit more movement with the yen losing ground more steadily for a net drop of 8.4% over 12 months, increasing Japan's competitiveness.

Export and import prices both rise month-to-month in January, February, and March. Over three months, export prices rise at a 25.2% annualized rate while import prices gain at a 63.2% annualized rate as oil prices are moving higher. Export and import prices both gain momentum from 12-months to six-months to three-months as the pace of price increases accelerate from 5.5% for both export and imports to sharply divergent gains over three months for the two flows. Import prices were pushed sharply higher by oil and commodities prices, making sharp gains over three months at a 63.2% pace.

As prices gyrated export and import volumes reacted to the rising price environment. Import prices rise by 5.5% over 12 months and gain sharply over three months as import volumes fall at a modest pace over both three months and 12 months. Import volumes react in a small way to prices changes because the demand for commodities is relatively inelastic (they are unresponsive in the short-term to price changes). Export volumes logged a 7.7% gain over 12 months then fell at a 9.4% annualized rate over three months as the gain in export prices accelerated; export volumes dropped partly because Japan does sell goods that have to be price competitive in world markets (they are price-elastic).

During the last year, the virus was running wild having a less pronounced impact on Japan but still prompting lockdowns especially around the Tokyo area as Japan with very high population density in Tokyo and a reliance on packed mass transit reacted to small increases in infections with an abundance of caution. Japan even cancelled the scheduled Olympics in 2020 because of concern about the virus spreading. Japan is currently busy trying to make the venue safe to conduct the once-delayed Olympics this year.

As 2021 has unfolded, manufacturing sectors are emerging globally even as service sectors remain impaired. Global supply chains are damaged by reactions to the virus and as manufacturing makes gains supply chain issues have lingered and become quite problematic in some sectors. Japan's trade flows are plugged into China and the U.S. Both are economies that are coming to life. This reawakening should help to boost Japan's growth through the trade channel. The global outlook is improving; however, the virus is still present, still a problem, and in most places, still spreading, despite vaccines being deployed. The vaccines give us hope that there is some sort of endgame in sight, but trade continues to be conducted under a cloud of uncertainty.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief