Global| Nov 20 2019

Global| Nov 20 2019Japan's Trade Remains in Deficit

Summary

Japan is suffering the fate of an economy with strong trade ties to two countries embroiled in a trade war. Japan's largest trade partner is China and its second largest trade partner is the United States. In October, Japan's exports [...]

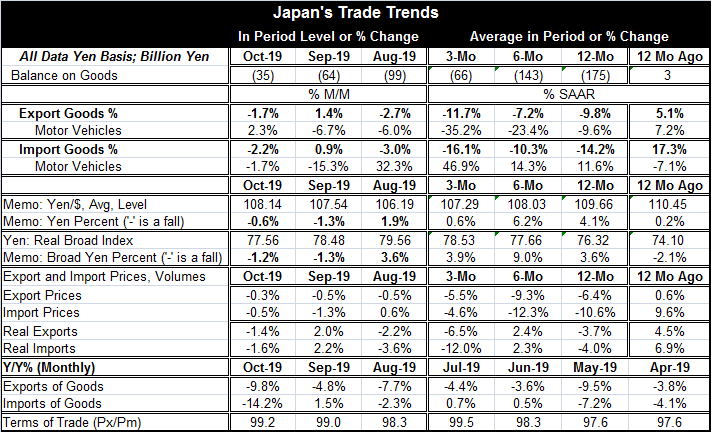

Japan is suffering the fate of an economy with strong trade ties to two countries embroiled in a trade war. Japan's largest trade partner is China and its second largest trade partner is the United States. In October, Japan's exports and imports fell month-to-month following gains for both in September after each of them fell in August. Nominal exports and imports both are falling over 12 months, six months and three months. Neither trade flow shows a clear cut case of persistent deceleration but each has a larger drop over three months than over 12 months on annualized growth rates.

Japan is suffering the fate of an economy with strong trade ties to two countries embroiled in a trade war. Japan's largest trade partner is China and its second largest trade partner is the United States. In October, Japan's exports and imports fell month-to-month following gains for both in September after each of them fell in August. Nominal exports and imports both are falling over 12 months, six months and three months. Neither trade flow shows a clear cut case of persistent deceleration but each has a larger drop over three months than over 12 months on annualized growth rates.

Export and import prices also show decline on all three horizons. However, their declines are larger over 12 months than over three months.

Real exports and real imports show declines over 12 months and three months for both exports and imports. Declines over three months are larger than the declines over 12 months.

While Japan's trade position remains in deficit, the deficits have become much smaller as the charts show. That means that the trade sector is siphoning off less of Japan's domestic demand.

The yen against the dollar and against a broad currency basket in real terms has generally been rising, but its path has been moderate.

However, the overpowering trend is that both exports and imports show decelerating trends year-over-year growth. Japan is feeling the global growth slowdown.

This past week BOJ governor Haruhiko Kuroda denied that he said that Japan has unlimited tools or abilities. It is clear that there are pressures being felt in Japan over what can be done. Of course, neither the BOJ nor the ECB nor the Fed are hitting their inflation targets. The BOJ is not alone in the failure. It may have a longer more severe history of missing but all money center inflation-targeting central banks are missing their targets.

Getting growth started has been hard to accomplish everywhere. Fiscal policy is essentially redlined in the U.S., Japan, and the EMU. China has been using debt to try to keep growth aloft, but that is a process that has been less and less effective. Global growth expectations have all its eggs in one basket, hoping for a U.S.-China trade deal. Will it develop, and if it does, will it be enough?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief