Global| Dec 14 2020

Global| Dec 14 2020Japan's Tankan and Outlook Improve Despite Ongoing Global Pandemic

Summary

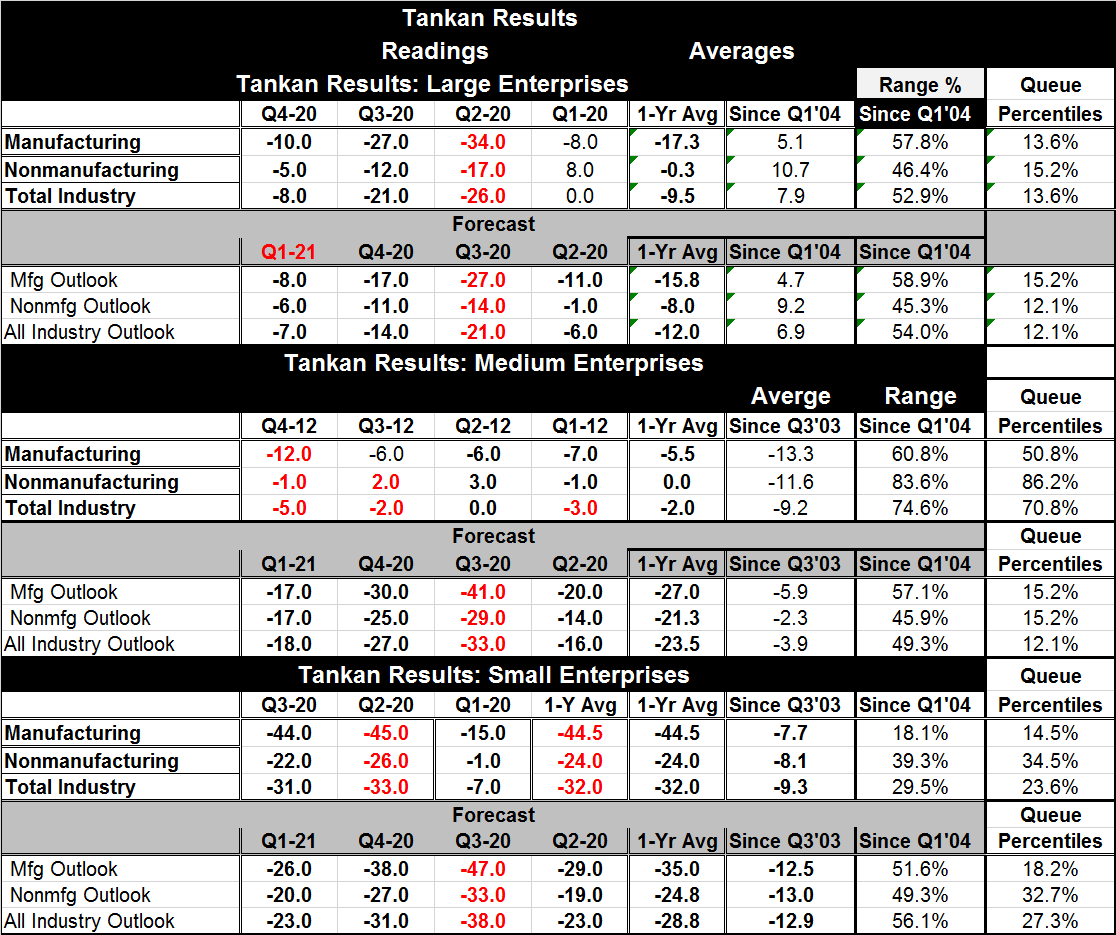

Japan's tankan survey for large firms improved this quarter with the current manufacturing index logging a value of -10 compared with -27 last month. The manufacturing outlook improved to -8 from -17 last quarter. The tankan is a [...]

Japan's tankan survey for large firms improved this quarter with the current manufacturing index logging a value of -10 compared with -27 last month. The manufacturing outlook improved to -8 from -17 last quarter.

Japan's tankan survey for large firms improved this quarter with the current manufacturing index logging a value of -10 compared with -27 last month. The manufacturing outlook improved to -8 from -17 last quarter.

The tankan is a quarterly assessment of Japan's economy that is the most closely watched of all Japanese surveys. The survey contains a wealth of information. The table below shows the survey ‘headlines' divided between firms of three different size categories: large firms, medium firms and small firms. Each size-class is further divided into manufacturing and nonmanufacturing. The manufacturers in the large company survey are taken as the bellwether for the survey.

At the far-right column, I present the tankan results in a percentile queue standing format on data ranked back to Q1 2004. That period includes 16.5 years of data. On that timeline, Japan's economy has been under a great deal of economic pressure. The current tankan large company manufacturing index has a 13.6 percentile standing (which is quite weak; this weak or weaker only 13% of the time…) and that is after its large jump this quarter. Despite the jump (which itself is impressive and is the largest quarter-to-quarter jump on this timeline), the tankan still has the very weak standing reported above. The improvement in the outlook index is the 6th strongest quarter-to-quarter change on the timeline and that leaves the future index with a 15th percentile standing. Large nonmanufacturing companies are assessed as just about as weak in the tankan assessment and are about equally as weak in the outlook.

The improvement in the current index has slightly outperformed the outlook index although both have improved sharply this quarter. The reasons for that must be that the current improvement is real (or perceived as such) while the forward assessment is based wholly on expectations that are being tempered by global conditions which themselves are being degraded by the virus and a new spread that raises fresh red-flags.

As always in these times, there is no economic polling or analysis that can occur without reference to the virus. Currently several vaccines are in trial or outright distribution modes globally. There is a chance that the global economy is in the endgame with this virus although the vaccines have not been fully vetted in a reality-setting yet and the Pfizer vaccine has some strict and difficult distributional demands that must be dealt with.

There should be no sense that we are home free or that everything will improve soon. The virus is still spreading and vaccine distribution will be methodical and since the vaccines are new some glitches in distribution should be expected. The outlook should continue to be somewhat measured although there is now a greater basis for hope.

Still, Japan's tankan seems to report a reasonable approach to and handicap of the future. Its current assessment has picked up sharply and perhaps that improvement will continue as global conditions find their footing and as the current wave of virus dissipates in the face of better practices and when confronted with vaccines. But there are still substantial contractionary forces acting on the global economy. The potential for the virus endgame to produce unpleasant surprises in Japan and elsewhere still exists. Global economies will also at some point have to reassess where they stand and what financial condition their local populations are in once the virus is gone.

In the U.S., an important export market for Japan, a lot of people have leaned hard on temporary programs to make finances stretch – quite apart from extra support payments and extra unemployment benefits. The removal of these programs could create a second wave of financial problems of a very significant magnitude - all by itself - even once the virus is vanquished. Risk will continue to haunt the global economy in many different guises. In the U.S., it will strike an economy weakened by the virus, and ladened with debt, with already deep political divisions.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief