Global| Jun 10 2020

Global| Jun 10 2020Japan's Surveys Show Gathering Weakness

Summary

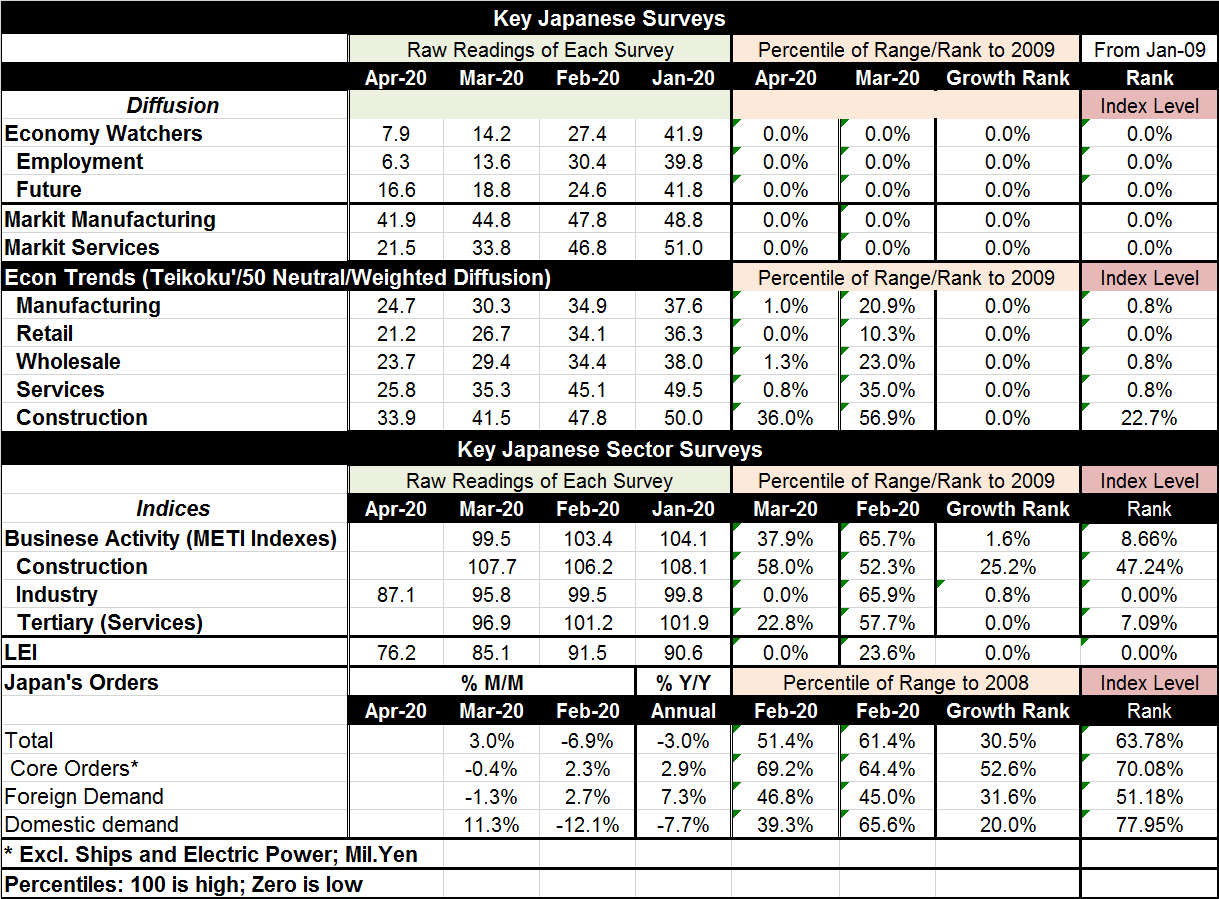

Japan's various economic surveys tell a consistent, depressing… and familiar story on the economy. The final two columns of the table rank the various readings on growth and on index level. The readings are uniformly and extremely [...]

Japan's various economic surveys tell a consistent, depressing… and familiar story on the economy. The final two columns of the table rank the various readings on growth and on index level. The readings are uniformly and extremely weak. The only exceptions to this observation are construction in the METI indexes that has a near-median standing (still slightly below median) and orders. What those series have in common is that they are up-to-date only through March while April is the month when the hammer fell on the economy in Japan, in Europe and in the United States. The one METI reading for April is for industry and that has a zero percentile standing.

Japan's various economic surveys tell a consistent, depressing… and familiar story on the economy. The final two columns of the table rank the various readings on growth and on index level. The readings are uniformly and extremely weak. The only exceptions to this observation are construction in the METI indexes that has a near-median standing (still slightly below median) and orders. What those series have in common is that they are up-to-date only through March while April is the month when the hammer fell on the economy in Japan, in Europe and in the United States. The one METI reading for April is for industry and that has a zero percentile standing.

New orders

The orders figures which despite lagging the chronology of other reports are also fresh data released just today, show that there was an orders rebound in March after extreme weakness in February. Core orders slipped a bit in March after a strong gain in February. Foreign demand weakened in March while domestic demand increased sharply. Yet, we know, with this series, the monthly results are very volatile so they may not say much of the progression of weakness or strength. Turning to more reliable year-on-year results total orders are lower while core orders are up. Foreign demand is up strongly while domestic demand is down about just as strongly. The level assessments (standings) on these series in March range from 51% to nearly 78%. But these are nominal series that are expected to grow over time with both economic growth and inflation. The one-year growth rankings range from a 52nd percentile standing down to a 31st percentile standing with foreign demand being the weakest reading, despite its strength relative to other series.

The orders data remind us of several things lagging as they do…they provide a snapshot of Japan ahead of the main impact of the coronavirus. This reminder shows us that foreign demand has already been weak largely because of an ongoing U.S.-China low-key trade war. Japan's largest trading partner is China and its second largest partner is the U.S. While ‘foreign demand' for Japan was up by 7.1% year-on-year, the growth rank of that result was only in its historic 31st percentile- a weak result. Core orders were growing and holding up slightly above their usual historic pace. Japan's domestic demand already was weak in the lower one fifth of its historic range.

More series

The up-to-date as of April, Teikoku indexes show growth and level rankings across the board as the lowest on this timeline. The Teikoku indexes are actually up-to-date through May (not shown) and they continue to offer weak and weakening signals. The economy watchers index also has May data (also not shown) available and it shows some rebound in progress.

Japan's progress

Japan's results are by now quite familiar from the patterns we have seen in other countries. What is going to distinguish countries was we move ahead is how far they fall into the pit of recession and how fast they recover and rise from the depths of the pit that they fall into. The plunge into recession was common to all virtually all countries. But national responses have been different in different economic systems. Sweden did not adopt a lockdown strategy and the U.K. was going to do the same until it was overwhelmed by the spread of disease. The U.S. has the largest volume of cases, but it has been hit hardest in New York, especially in NYC (where I live) and the impact here has been tremendous; it continues to have substantial impact on daily life. But much of the rest of the U.S. is much less affected with great differences from state to state.

These differences in how the virus was reacted to and how it spread will help to create different circumstances for the reseeding for growth. Everywhere governments have tried to help and to reduce the adverse impact on growth. The U.S. has already been deemed to have fallen into recession. Yesterday U.S. Treasury Secretary declared that the U.S. economy has begun the process of recovery. This is much sooner than had been expected if he is right. But the question remains about what sort of recovery it will be. Will other countries end their recessions earlier as well?

Just today the OECD issued reports saying that this will be the deepest recession since the great depression globally. It has said that the U.K. economy could be hit the hardest of all and could contract by as much as 14%. It has also said that in a single-hit (no second wave of infection), France could decline by 11.4%, Spain by 11.1%, Italy by 11.3%, and Germany by 6.6%. These are impressively large numbers and do not embrace the potential for a second wave of infection.

Japan's data suggest that the blueprint of economic decline is more or less the same and is in progress globally. China is an exception to some extent but how much we do not know since so much of what has happened there is shrouded in mystery - especially the timing. We will continue to track economic progress and look for clues as to what is next and where. For now Japan seems to be on a familiar track.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief