Global| Dec 16 2009

Global| Dec 16 2009Japan's Service Sector Shows Improvement

Summary

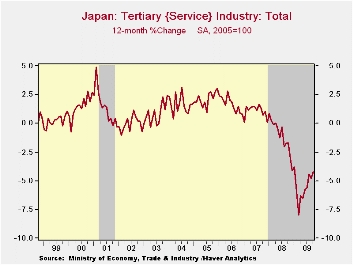

Japan’s service sector as gauged by its tertiary sector index advanced in October after registering a drop in September. The index is down by 4.3 percent over 12-months compared to MFG and mining where the index is down by 14% over [...]

Japan’s service sector as gauged by its tertiary sector index advanced in October after registering a drop in September. The index is down by 4.3 percent over 12-months compared to MFG and mining where the index is down by 14% over 12-months. These drops compare to March and February lows in the two indices, respectively. In March the tertiary index was down by 8.6% Yr/Yr. In February the mining and MFG index scored its largest 12-month drop at -36.9%.

Cleary Japan has been improving sharply from its recession lows. But while the mining and MFG sector has eight straight months of improvement in its mo/mo readings, services has only improved for one month in a row. Services also has improved in five of the past six months. Still, the tertiary sector is only up by 2.5% from its cycle low point whereas MFG and mining is up by 23.8% from its cycle low reading. MFG and mining currently stands by 21.8% below its cycle peak whereas the services sector is off by just 6.4% from its cycle peak. Two sectors are experiencing very different recession and recovery forces.

The service sector stands in the 53rd percentile of its range while Mining and MFG stands in the 40th percentile of its range, well below its mid-way mark.

Still, the failure of services to post consistent gains or strong gains while MFG is improving sharply is a sign that Japan is still struggling. We know it is having some renewed problems with deflation. In this environment because the service sector employs so many, it is easy to see why confidence does not easily come back and why Japan remains vulnerable to deflation even in face of some export recovery and a strong MFG rebound. The rising yen has pre-empted the possibility of compensation for service sector weakness with strong export-led growth. While Japan’s exports are recovering they are also hindered by the continuing strength of the yen. Japan’s recovery continues to face a dilemma

Japan Industry Survey| Recent Months | Moving Averages | Extremes; Range | |||||||

| Oct-2009 | Sep-2009 | Aug-2009 | 3-Mo | 6-Mo | 12-Mo | Max | Min | %-Tile | |

| Mining and MFG | 86.1 | 85.7 | 83.9 | 85.2 | 83.1 | 80.7 | 110.1 | 69.5 | 40.9% |

| Tertiary | 96.8 | 96.3 | 96.9 | 96.7 | 96.4 | 97.0 | 103.5 | 89.1 | 53.5% |

| Ranges, Max, Min since 1993 | |||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief