Global| Jan 23 2020

Global| Jan 23 2020Japan's Sector Indexes Show Weakness and a Loss of Momentum

Summary

Japan's indexes of industry level activity show a gain in the all-industry index in November. The rise in November to 103.9 from 103.0 in October is driven mostly by a rise in the tertiary sector (services) although there is also a [...]

Japan's indexes of industry level activity show a gain in the all-industry index in November. The rise in November to 103.9 from 103.0 in October is driven mostly by a rise in the tertiary sector (services) although there is also a small uptick month-to-month in construction.

Japan's indexes of industry level activity show a gain in the all-industry index in November. The rise in November to 103.9 from 103.0 in October is driven mostly by a rise in the tertiary sector (services) although there is also a small uptick month-to-month in construction.

The three-month, six-month and 12-month averages show a steady diet of weaker readings into the more recent periods. Supporting that finding, the simple point-to-point growth rates over three months, six months and 12 months also show growth rates that indicate contraction and a pace of contraction that is getting progressively larger over shorter periods.

In addition, the ranking of the sector indexes on their levels shows moderate-to-weak standings. The overall all-industry index has a 69.9 percentile standing. That is boosted mostly by the tertiary sector's 83.9 percentile standing. Construction has a 55.9 percentile standing with mining and manufacturing at a weak 12.7 percentile standing. Since these sector indexes grow over time, they should be expected to sit quite high in their respective ranges but they do not. When we rerank the sectors by growth rates over the past 12 months, we find that all sectors when ranked on growth rate data since 2000 have extremely low rankings. Construction has the highest rank standing in its 28.8 percentile- in the lower one-third of its historic collection of growth rates. Mining and manufacturing as well as the tertiary sector rank in the bottom 10th percentile of their respective growth rates. As a result of this collection of weakness, the all-industry growth rate has a 7.1 percentile standing, a standing that has been this weak or weaker only about 7% of the time since 2000. That is a very weak result.

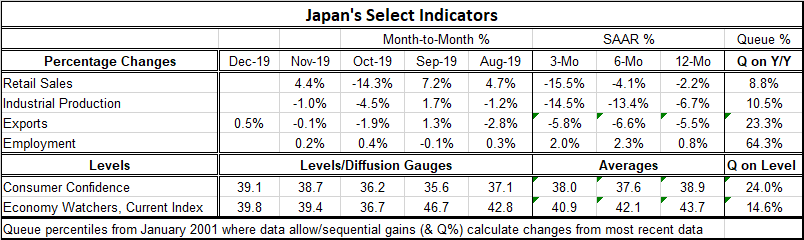

While the sector data may not be as familiar, I compare to the topical information we have on traditional indicators like retail sales, industrial production, exports and employment. I also include several variables that are ranked by level; these are statistics gathered on a diffusion basis where values vary between zero and 100. The familiar indicators echo the weakness in the sector indexes and also the poor and generally deteriorating growth environment.

Japan's data, much like in the U.S., show the best performance for employment data. Employment growth is weaker over three months than over six months, but both six-month and three-month growth rates exceed the 12-month pace by a substantial margin. Yet, retail sales are slowing, contracting, and getting progressively worse. Industrial output echoes this same performance. Exports, too, are dropping and generally worsening but hold about the same negative growth rate over three months as over six months. The economy watchers index gets progressively weaker while consumer confidence weakens from 12-months to three-months with a small pick-up over six months. The queue or rank standings of these variable all are very low with employment being the exception although a 64th percentile standing on 12-month job growth is not strong and only looks ‘exceptional' when compared to the other sector rankings.

Japan is weakening. Its monetary policy has the spigot open about as wide as it can be. Fiscal policy is available for only light duty since Japan's debt-to-GDP ratio is so high. Japan's two major trade partners, the U.S. and China, just concluded a partial trade deal that Japan is hoping will make a difference since it is running out of things to do on its own. Japan is coming off a consumption tax hike it engineered late in the year as part of a long-standing move to raise tax revenues in the face of such a large pile of government debt. But demographics are stacked against Japan as its population is aging and also shrinking. All these conditions pose difficult challenges and explain why Japan is facing largely contracting conditions.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief