Global| Mar 29 2018

Global| Mar 29 2018Japan's Retail Sales Show Some Life Year Over Year

Summary

Retail sales in Japan are off by 0.2% month-to-month in February, falling on that basis for the second month in a row on seasonally adjusted data. Still, retail sales are up by 1.7% from one year ago. With only two exceptions since [...]

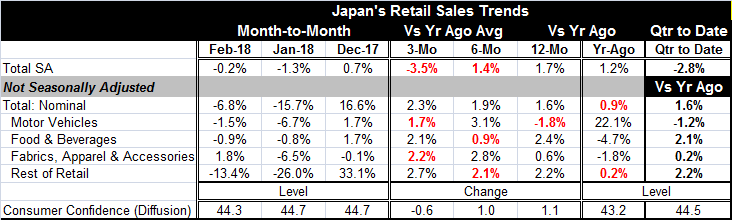

Retail sales in Japan are off by 0.2% month-to-month in February, falling on that basis for the second month in a row on seasonally adjusted data. Still, retail sales are up by 1.7% from one year ago. With only two exceptions since April of last year, the three-month average of the retail sales year-on-year growth rate has been at 1.9% or higher and never higher than 2.4%. Japan’s retail sales seasonally adjusted have been very steady. February’s 1.7% gain over 12 months corresponds to a 2.3% rise of the three-month average of 12-month percentage changes, and presents retail sales trends as on the same path that they have been on for the better part of a year.

Retail sales in Japan are off by 0.2% month-to-month in February, falling on that basis for the second month in a row on seasonally adjusted data. Still, retail sales are up by 1.7% from one year ago. With only two exceptions since April of last year, the three-month average of the retail sales year-on-year growth rate has been at 1.9% or higher and never higher than 2.4%. Japan’s retail sales seasonally adjusted have been very steady. February’s 1.7% gain over 12 months corresponds to a 2.3% rise of the three-month average of 12-month percentage changes, and presents retail sales trends as on the same path that they have been on for the better part of a year.

Understanding the not seasonally adjusted trends

The month-to-month sales patterns for the not seasonally adjusted components are showing sales declines; this is historically normal sale usually fall NSA early in the year. To try to account for the strong seasonality in retail sales and still present some component detail, the table for three-month and six-month changes presents the three-month and six-month (NSA) average for the month expressed as a percentage change of the same average of one year ago. This is just another smoothing process. Looked at in this way, over three months, all retail component growth rates are at or above 2% except for motor vehicles where sales gained only 1.7%. Over six months these smoothed averages show more variability with vehicle sales as strong as 3.1% and food and beverage sales as weak as 0.9%. The 12-month gain is simply the current month February over February of 2017 and it shows more variability across components because its one-month change is not averaged with any adjacent months.

Viewed in this way, overall NSA retail sales are accelerating but none of the components are although most have three-month (smoothed) growth rates stronger than their (smoothed) 12-month pace. The seasonally adjusted retail sales patterns for total retail sales do not share this characteristic and on that basis sales are actually decelerating. However, as noted above, the three-month average of the seasonally adjusted 12-month rates of growth remains stable and firm at a growth rate of 2.3%.

Momentum

There is a difference between the two momentum calculations since one is smoothed while the other is based on more volatile point-to-point changes using compounded rates of growth. While most U.S. economists have an affinity for seasonally adjusted data, unless the underlying series is very stable and predictable calculating short-term growth rates can magnify volatility. Japan’s retail sales volatility has been declining very steadily and now both the seasonally adjusted series and the smoothed year-on-year calculations are very well-behaved. This gives us grounds to believe their trends. Still, the weakness in the seasonally adjust series over three months is hard to understand since the not seasonally adjusted series show signs of being stronger than they usually are at this time of year. This weakness in three-month seasonally adjusted sales seems inconsistent with the NSA data and all the other trends. So we will want to keep an eye on Japanese retail sales especially now.

Special factors

There is a lot in train in Asia that could impede or setback Japan’s confidence levels. Prime Minister Abe is under pressure for his alleged involvement in a real estate deal. Despite his denials, his favorability ratings have deteriorated. Taiwan and China are having some difficulties and China as a result has been running some naval maneuvers in the area that have led to heightened tensions. Of course, there is the unsettled behavior of North Korea and the pending U.S. talks with Kim Jong-un to consider. And not least of all is Japan trying to make a deal with the U.S. over its new tariff policy. All of this puts Japan under some degree of pressure and stress that could lead to a loss of consumer confidence. So far (as you see in the bottom of the table), consumer confidence is fair to stable.

The quarter-to-date

The quarter-to-date calculations mix the seasonally adjusted data that calculate growth over two months relative to the Q4 base of retail sales while annualizing it, to the smoothed data which compare January plus February growth to January plus February of one year ago. These are very different concepts, but the date being NSA force this approach on us. The seasonally adjusted approach shows growth falling quarter-over-quarter exactly what you expect with two consecutive quarters of retail sales declines in January and February. But the smoothed data show a year-on-year rise of 1.6% overall on mixed components with vehicle sales and food & beverages coming in as the weak sectors. Note that the NSA smoothed data show nearly the same year-on-year gain for the quarter-to-date (compared to one year ago) as does the simple 12-month change in retail sales calculated from seasonally adjusted data. All in all, economic data always have some volatility, but Japan’s retail sales still seem to be on reasonably solid footing and trends.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief