Global| Oct 22 2018

Global| Oct 22 2018Japan's METI Sector Indexes Rebound But Still Lag

Summary

Japan's economy continues to fight for revival. In August, the METI all-sector index has revived, rising to 105.7 from 105.2, but it had fallen in June and July and is still below its May level of 106.4. The index is up on its reading [...]

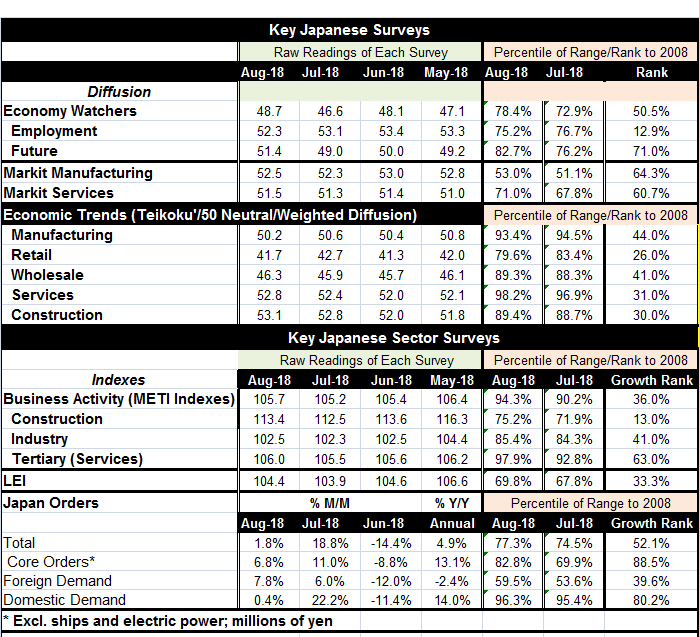

Japan's economy continues to fight for revival. In August, the METI all-sector index has revived, rising to 105.7 from 105.2, but it had fallen in June and July and is still below its May level of 106.4. The index is up on its reading of 105.1 of 12-months ago but that is a small gain for 12 months, less than one tick per month, amounting to net gain of 0.6% over 12 months.

Japan's economy continues to fight for revival. In August, the METI all-sector index has revived, rising to 105.7 from 105.2, but it had fallen in June and July and is still below its May level of 106.4. The index is up on its reading of 105.1 of 12-months ago but that is a small gain for 12 months, less than one tick per month, amounting to net gain of 0.6% over 12 months.

The story of Japan's economic recovery still seems to be a story of two steps forward and one and one-half steps backward as progress is very difficult to come by and then just as hard to sustain. Inflation continues to be below target and the Bank of Japan has gone to extraordinary lengths to try to get it back on track.

Internationally, Japan's largest trade partner, China, is dealing with a trade war with the United States that has coincided with slower growth in China and with market setbacks. Meanwhile, Japan has its own trade issues to hammer out with the U.S.

And Japan's own economy is not performing all that well on its own. I rank the METI indexes' performance on their year-over-year growth over a period back to 2008. Against this benchmark, the overall METI activity index has a 36th percentile rank; historic growth rates rank it higher 64% of the time. The current growth is at the border of the bottom one-third of all historic growth rates since 2008. Construction is even weaker with a 13th percentile standing. Industry has a weak and still below median 41st percentile standing. The services sector has a 63rd percentile standing, above its median (at the 50th percentile on this metric) but still a reading that lies outside the top one-third of results historically. Japan is still struggling to get and to stay mediocre.

In the consolidated table, we offer a look at several different sorts of surveys. The economy watchers index has a muted 50th percentile standing for August when it moved nicely higher to 48.7 from July's 46.6. Still, its employment gauge has a weak 12.9 percentile standing. But the future gauge is more optimistic with a 71st percentile standing.

The Markit manufacturing service gauge that ranks value over the past 4.5 years shows rankings in the 64th and 60th percentiles respectively for manufacturing and services. These are rankings just out of the top third of their respective historic ranges.

The Teikoku sector indexes are much more upbeat if they are ranked as diffusion indexes based on their levels. On that basis, they emerge quite strong almost in line with the high-low percentile statistics in the table. But if we rank them based on their annual changes or growth rates, they are only slightly more upbeat than the METI indexes. Based on their rankings by annual growth rates, the Teikoku indexes show a manufacturing ranking in its 44th percentile and various service sector standings ranging from the 26th to 43rd percentiles. Construction in this framework has a 30th percentile rank standing which is better than in the METI framework but still quite weak.

Japan's LEI rose in August to 104.4 from July's 103.9, but like the METI indexes, the LEI still sits below its May level. The LEI growth rank is at the border of the bottom one-third of its historic rank of values.

Japan's orders series has a relatively upbeat showing for the trimmed ‘core orders' measure that excludes volatile and lumpy items; that has an 88th percentile standing. But the overall order gauge has a much more modest 52nd percentile standing. Accordingly, foreign demand is evaluated as the weakest with foreign orders having a 39th percentile standing and with domestic orders at an elevated 80th percentile standing.

Japan's growth has always been importantly plugged into the global economy. But it is also driven by its domestic economy and on all fronts Japan is struggling. The weak construction sector speaks to weakness at home. Services have a higher historic rank, but that part of the economy is usually a slow growing more dependable backbone rather than a growth leader. When the services sector is the growth leader, the economy has fallen on hard times for sure. Japan's industrial sector is struggling with a good deal of headwind coming from the foreign sector as the orders data remind us. But clearly, the very structure of Japan's trade makes it clear that will be the case in this sort of a global environment.

Inflation remains contained everywhere globally so it is not a good idea to be too hard in any assessment of the BOJ. Japan has demographic issues as its population shrinks in addition to a global environment unfriendly to restarting inflation. Encroaching global weakness and extreme competiveness, at the same time that technology is making life difficult for labor to get paid all stand in the way of an inflation restart. Japan is growing, but it is not prospering and inflation is not making progress to its policy objective. In that sense, Japan can only claim mediocre economic performance at best.

With a debt-to-GDP ratio that already is massive and BOJ policy already at full-stop stimulus, it is unclear what if any levers policymakers have left to pull except those that might slow growth. And that does not seem to be in order. Globally, growth is disappointing as well with the possible and past exception of the U.S. But looking ahead, it is unclear that the U.S. can keep up its progress as it is getting more distant from its fiscal stimulus and Fed rate hiking has gone on for long enough that the Fed may be too distracted by where it wants to go to have kept tabs on where it's been and what that offers for the future since monetary policy works with lags and U.S. has been hiking rates since end-2015. Add in the welter of geopolitical risks that have emerged and the risk to global growth seems to be cumulating at a rapid pace. The view from the U.S. is from a very special, and perhaps biased, vantage point. A survey of prospects from most any other global venue is much more circumspect, Japan included.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief