Global| May 01 2017

Global| May 01 2017Japan's Manufacturing PMI Moves Up; Inflation Gauges in the PMI Get an Unexpected Lift- Can That Last?

Summary

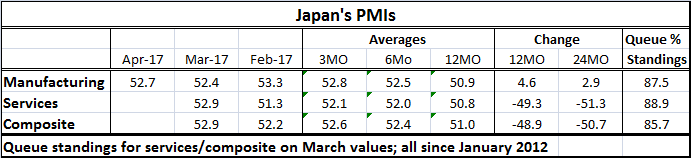

Japan's manufacturing PMI gauge is higher in April at a 52.7, up from 52.4 in March. Ranked over all values since January 2012, it stands in the top 87.5 percentile of all recent surveys. It's a good solid report. Japan's services [...]

Japan's manufacturing PMI gauge is higher in April at a 52.7, up from 52.4 in March. Ranked over all values since January 2012, it stands in the top 87.5 percentile of all recent surveys. It's a good solid report. Japan's services sector has ranked high on this same time horizon, but its final estimate is not yet available.

Japan's manufacturing PMI gauge is higher in April at a 52.7, up from 52.4 in March. Ranked over all values since January 2012, it stands in the top 87.5 percentile of all recent surveys. It's a good solid report. Japan's services sector has ranked high on this same time horizon, but its final estimate is not yet available.

The price components may be the most interesting part of this survey since the Bank of Japan is targeting inflation and trying hard to put Japan's deflationary ways behind it even in the face of a declining population. Input prices rose sharply in this report due to higher raw material costs. But firms also reported raising their prices-charged to defend profit margins. The output prices index in April moved up to 51.2 from 50.1 in March; it was up for the fourth consecutive month and at its highest reading in almost 2.5 years. The presence of knock-on pricing effects is a positive development in the quest for price stability and the eradication of deflation.

We have seen inflation flare and backtrack elsewhere like in the U.S. today where the core PCE has slipped back as the oil price pushed as lost momentum. Japan will have to wait to see if this report is picking up fundamental progress on inflation and on inflation expectations or if it is just a legacy of oil market dynamics.

As Japan battles to raise inflation to the 2% mark, inflation and inflation expectations globally are quite low. In the U.S. last week, the Conference Board produced a series on income expectations that was still quite weak even as the forward-looking assessment was for quite strong (rarely stronger) job growth. Together this seems to speak to the issue of weak wage expectations. Also last week the University of Michigan consumer sentiment report produced inflation expectations that rivaled historic lows for many readings. Inflation is simply not widely expected. In Europe today 'professional forecasters' expect headline euro area consumer prices to rise only a tick or two faster than earlier expected. Core inflation is seen to be picking up only slowly. These results are from a survey by the European Central Bank from Friday. Average headline inflation expectations for 2017, 2018 and 2019 are now raised to 1.6% (from 1.4%), 1.5% (previously 1.5%) and 1.7% (from 1.6%). This is the ECB Survey of Professional Forecasters. The longer-term inflation expectation was left unchanged at 1.8%. Clearly while there is some upshift here, this is not much of a hike even in the face of higher oil prices. Expectations for inflation excluding food and energy (core inflation) were 1.1%, 1.3% and 1.5% in 2017, 2018 and 2019, respectively. That figure is seen rising to 1.7% by 2021. Much like the FOMC in the U.S., the ECB professional forecasters see a very slow return of inflation to its most desirable habitat around 2%.

Maybe inflation is going to build faster in Japan because of all the BOJ special policies, but then again, maybe not. And maybe Japan is also just seeing the impact of OPEC oil price policy which now finds itself under a great deal of pressure. Not only is U.S. fracking coming back on steam, but today's weaker-than-expected Chinese PMI has raised fears of a too low rebound in demand. OPEC may have to make some uncomfortable decisions relatively soon and cut back output not just longer but with more vigor. It can control prices, but it must have the will. And if Russia is not on board for round II, that will would be much more costly. What exactly is OPEC prepared to do and who will be sticking with the cartels program? These could be very important decisions for Japan in its fight to eradicate deflation. It would be very hard to fight deflation if oil prices collapsed again.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief