Global| Feb 17 2016

Global| Feb 17 2016Japan's Machinery Orders Make Rogue Rise in December

Summary

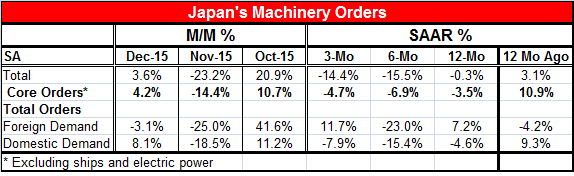

Japanese machinery orders rose in December by 3.6% for total orders and advanced by 4.2% for core orders, the latter gauge a treatment that excludes bulky capital projects. However, these gains follow huge drops in November that [...]

Japanese machinery orders rose in December by 3.6% for total orders and advanced by 4.2% for core orders, the latter gauge a treatment that excludes bulky capital projects. However, these gains follow huge drops in November that exceeded very strong gains in October. As a result, three month trends show that orders are contracting for both overall and core orders. Overall and core orders, in fact, are receding over six months and over 12 months as well. Japan's machinery orders, while up in December, are still under a great deal of negative pressure. The December gain appears to be more rogue than a new trend.

Japanese machinery orders rose in December by 3.6% for total orders and advanced by 4.2% for core orders, the latter gauge a treatment that excludes bulky capital projects. However, these gains follow huge drops in November that exceeded very strong gains in October. As a result, three month trends show that orders are contracting for both overall and core orders. Overall and core orders, in fact, are receding over six months and over 12 months as well. Japan's machinery orders, while up in December, are still under a great deal of negative pressure. The December gain appears to be more rogue than a new trend.

Foreign demand is choppy with increases over three months and 12 months despite a drop over six months. Japan's domestic machinery orders are still falling on all these horizons, but at least they are not steadily decelerating.

There is no sign of stability here. If there is hope, it is from orders in the foreign markets where demand has been so volatile and occasionally positive. But China is Japan's largest trade partner and it is still struggling and shifting away from its manufacturing sector. Europe is also floundering and waiting for news on more ECB stimulus. The U.S. economy has slowed but is growing. Its own orders report has been weak. The global story is, in fact, not encouraging.

All the developments I cite above, fit nicely (well, uncomfortably, from the standpoint of what it means for industrial growth and investment) into the theme of extreme global supply excesses. Globally export and import growth has been weak. The Baltic dry index, an indicator of trade volume growth, has been weak. All of this makes it clear that there will be slack demand for industrial investment for some time. We saw weakness in U.S. housing starts in a report released today and also weakness in euro area construction in another. Weakness is not just for industrial expansion but also housing and other capital projects where demand has been weak. I mention construction since construction projects are major users of various kinds of equipment that would generate industrial orders. You can turn over every single rock and look underneath it and what you will find is that there is little reason for optimism that the industrial sector and orders have anything but continuing pain in store for some time to come.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief