Global| Oct 14 2020

Global| Oct 14 2020Japan's IP Moves Up But With Less Pace

Summary

Japan's industrial sector remains on the mend, but its rise in output in August is starkly weaker than in July when it surged. The recovery from the covid-19 episode continues, but it is a recovery that now appears to be more drawn [...]

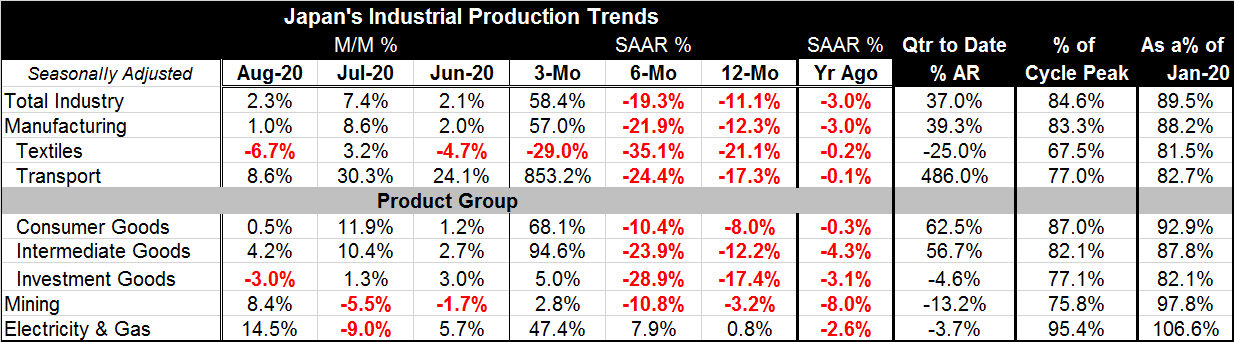

Japan's industrial sector remains on the mend, but its rise in output in August is starkly weaker than in July when it surged. The recovery from the covid-19 episode continues, but it is a recovery that now appears to be more drawn out and less swift. The chart with the sequential growth rates seems to offer the opposite view with the three-month growth rate surging. But that surge is driven by the strong 7.4% (not annualized!) gain in output in July. The monthly data reveal that, after that surge, output grew by just 2.3% in August and by just 1% in manufacturing. Those are still solid and even strong numbers, but they are a substantial stepdown from July's pace

Japan's industrial sector remains on the mend, but its rise in output in August is starkly weaker than in July when it surged. The recovery from the covid-19 episode continues, but it is a recovery that now appears to be more drawn out and less swift. The chart with the sequential growth rates seems to offer the opposite view with the three-month growth rate surging. But that surge is driven by the strong 7.4% (not annualized!) gain in output in July. The monthly data reveal that, after that surge, output grew by just 2.3% in August and by just 1% in manufacturing. Those are still solid and even strong numbers, but they are a substantial stepdown from July's pace

Over six months, counting from February when the virus was spreading the most globally, Japan's output is lower and falling at a 20% annual rate in round terms for both total industry and for manufacturing. Both textiles and transportations detailed in the table show declines at a more rapid pace than for industry overall. Measured over 12 months, the overall and manufacturing declines are nearly halved compared to their six-month trends but still in double digits. And, of course, of three months output is surging.

On a quarter-to-date (QTD) basis, total industry and manufacturing are spurting at annualized rates approaching 40%. But the prior comparisons underscore that even with such a rapid recovery output has not been restored to pre-covid-19 levels. We explicitly measure current output relative to its January level before there were any covid-19 worries in Asia. And we find output is 11% to 12% below those levels for industry overall and for manufacturing. Textiles and transportation are both closer to 18% off those levels of performance on the same timelines.

Looking at sectors, it is clear that utilities has had a steadier demand profile and have gone their own way more than other sectors. Utilities (and food- not shown separately here) are the only sectors that have more than just recovered relative to their yearly starting values. Mining seems to have been less hit by the virus but is now hit harder by the second-round consequences of the virus as mining is falling in its QTD profile while most other sectors are flying high in recovery. Mining is now lower by only 3.2% over 12 months and is only lower by about 2% from its January level. Contrast that to consumer goods (-7.1%), intermediate goods (-12.2%) and investment goods (-17.9%); all of which are down much more sharply from their respective January levels. But consumer goods and intermediate goods are seeing huge gains in the QTD period both with annualized rates of growth of over 50%. Investment goods do not fare as well as they are still contracting at a 4.6% annual rate in the QTD period as well as falling in August (...as well as lower by 17.4% year-on-year).

The message here is that all sectors have been sucked into weakness, but that whether people are at home or at work they continue to consume the output of the utilities industry. Also the message is that even if a sector like mining escapes the first wave of downturn it remains plugged into the broader economy and as the overall economy slows a sector like mining is nonetheless sucked into the malaise of weakness that develops. It is the same globally as the global trading matrix has spread the weakness. Still, some are hit harder than others.

Also there is the question of the second wave… It appears to have revived quite strongly in Europe as a number of countries there are now seeing a revival of infections that rivals or exceeds their first wave. The U.S. is having a much more modest revival of virus in the second round although there are very different experiences state by state. Tip O'Neil might remark that all infection is local. Japan has some revival in infection, but it is still quite a mild ‘outbreak' if we can even call it that. Nonetheless, Japan is a country with high population density and a lot of interpersonal proximity that is all but unavoidable and so it has taken even small outbreaks extremely seriously. For now infections do not seem to be as big a problem in Japan as other places, but even without much of it the economic recovery has slowed.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief